alwaysinasnit

alwaysinasnit's Journal'We will coup whoever we want': Elon Musk and the overthrow of democracy in Bolivia'

https://www.alternet.org/2020/07/we-will-coup-whoever-we-want-elon-musk-and-the-overthrow-of-democracy-in-bolivia/On July 24, 2020, Tesla’s Elon Musk wrote on Twitter that a second U.S. “government stimulus package is not in the best interests of the people.” Someone responded to Musk soon after, “You know what wasn’t in the best interest of people? The U.S. government organizing a coup against Evo Morales in Bolivia so you could obtain the lithium there.” Musk then wrote: “We will coup whoever we want! Deal with it.”

Musk refers here to the coup against President Evo Morales Ayma, who was removed illegally from his office in November 2019. Morales had just won an election for a term that was to have begun in January 2020. Even if there was a challenge against that election, Morales’ term should rightfully have continued through November and December of 2019. Instead, the Bolivian military, at the behest of Bolivia’s far right and the United States government, threatened Morales; Morales went into exile in Mexico and is now in Argentina.

At that time, the “evidence” of fraud was offered by the far right and by a “preliminary report” by the Organization of American States; only after Morales was removed from office was there grudging acknowledgment by the liberal media that there was in fact no evidence of fraud. It was too late for Bolivia, which has been condemned to a dangerous government that has suspended democracy in the country.

snip...

Musk’s admission, however intemperate, is at least honest. His company Tesla has long wanted access at a low price to the large lithium deposits in Bolivia; lithium is a key ingredient for batteries. Earlier this year, Musk and his company revealed that they wanted to build a Tesla factory in Brazil, which would be supplied by lithium from Bolivia; when we wrote about that we called our report “Elon Musk Is Acting Like a Neo-Conquistador for South America’s Lithium.” Everything we wrote there is condensed in his new tweet: the arrogance toward the political life of other countries, and the greed toward resources that people like Musk think are their entitlement.

Sometimes people refuse to learn a lesson even after being hit upside the head.

https://www.rawstory.com/2020/07/i-truly-thought-last-friday-was-gonna-be-my-last-says-texas-hardline-conservative-lawmaker-who-was-hospitalized-for/‘I truly thought last Friday was gonna be my last,’ says Texas hardline conservative lawmaker who was hospitalized for coronavirus.'

State Rep. Tony Tinderholt was hospitalized last week after testing positive for the novel coronavirus, the lawmaker confirmed Friday to The Texas Tribune, marking the first known case involving a member of the Texas Legislature.

“I truly thought last Friday was gonna be my last,” Tinderholt, an Arlington Republican, said in a text message to the Tribune. Tinderholt said his wife and two of his children also tested positive for the virus, though their symptoms were less severe.

snip...

While Tinderholt acknowledged the virus is a “serious illness,” he reiterated Friday his position that Abbott shutting down parts of the economy is wrong.

“Closing the entire economy and halting business as well as illegally taking people’s freedoms are absolutely the wrong things to do to Texas, Texans and our nation,” Tinderholt said.

..........

You can't fix stupid.

The Eviction Ban Worked, but It's Almost Over. Some Landlords Are Getting Ready.

https://www.propublica.org/article/the-eviction-ban-worked-but-its-almost-over-some-landlords-are-getting-readysnip...

Starting July 25, a key component of the federal eviction moratorium is set to expire, allowing landlords that operate federally backed rental properties to give their tenants 30 days’ notice to vacate. After that period, landlords can file for eviction. Axiom has made it clear that it intends to take swift legal action once the protections run out.

snip...

The ban on evictions at federally backed properties that Congress passed in March as part of the CARES Act has played a significant role in shielding the nation’s renters from the risk of losing their homes during the pandemic, a ProPublica analysis of eviction cases filed before and during the pandemic shows.

snip...

But both expanded unemployment payments and the federal eviction ban are set to wind down at the end of the month, and eviction filings have started to tick up in recent weeks as courts in many jurisdictions are either scheduled to or have already reopened.

That sets the stage for a potential crisis for renters and landlords alike if lawmakers don’t extend measures to support renters as Congress returned to session this week, housing advocates say.

snip...

Bill Barr could face probe after 4 ex-presidents of DC Bar Ass'n sign complaint detailing abuses

https://www.alternet.org/2020/07/bill-barr-could-face-bar-association-probe-after-4-ex-presidents-sign-complaint-detaiing-his-abuse-of-office/U.S. Attorney General Bill Barr has been widely criticized in the legal profession for putting the interests of President Donald Trump above the rule of law, and some of those critics include four former presidents of the District of Columbia Bar Association. According to Politico reporter Betsy Woodruff Swan, all four of them are among the 27 attorneys who have signed a July 22 letter asking the Association to conduct an investigation to determine whether or not Barr has violated its rules.

The D.C. Barr Association authorizes attorneys to practice law in Washington, D.C., including many who work in the federal government. According to Swan, the attorneys’ “complaint argues that Barr has broken Washington’s ethics rules by being dishonest and violating his oath to uphold the Constitution, along with other charges. And it highlights four episodes in Barr’s time as attorney general to make the case: his characterization of Special Counsel Robert Mueller’s report on Russia’s 2016 election interference, his criticism of an inspector general report on the Russia probe, his criticism of FBI officials in a TV interview, and his role in the disbursement of peaceful protesters from Lafayette Square outside the White House.”

The letter states, “Mr. Barr’s client is the United States, and not the president. Yet Mr. Barr has consistently made decisions and taken action to serve the personal and political self-interests of President Donald Trump rather than the interest of the United States.”

The four ex-presidents of the D.C. Barr Association who signed the letter are Andrea C. Ferster, Melvin White, Philip Allen Lacovara and Marna S. Tucker. Others who signed it range from Abbe Smith (a law professor at Georgetown University in Washington, D.C.) to Roy L. Austin, Jr. (a former deputy assistant attorney general in the U.S. Department of Justice’s civil rights division).

snip...

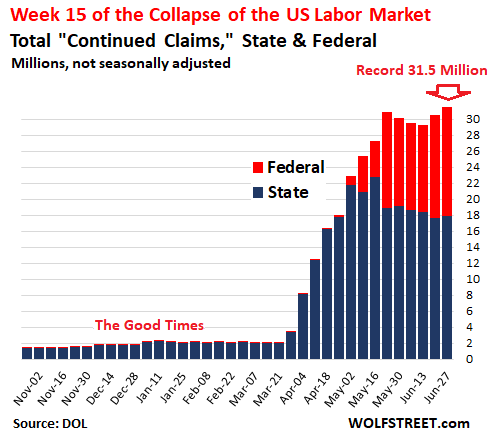

Never Before Have I Seen So Much Fake Unemployment & Jobs Data by the Bureau of Labor Statistics.

https://wolfstreet.com/2020/07/02/never-before-have-i-seen-so-much-fake-unemployment-jobs-data-by-the-bureau-of-labor-statistics-while-labor-department-nails-it/Never Before Have I Seen So Much Fake Unemployment & Jobs Data by the Bureau of Labor Statistics. Labor Department Nails It

Labor Department today: People on state & federal unemployment insurance jumped to 31.5 million, worst ever.

Bureau of Labor Statistics today: 4.8 million jobs created, unemployment dropped by 3.2 million.

BLS under-reported unemployment by 13.7 million, based on data from the Labor Department. What’s happening is infuriating. Read and cringe.

Normally, the jobs report by the Bureau of Labor Statistics is released on the first Friday of the month. And the unemployment claims report is released Thursday every week. But this month, the monthly jobs report was also released today because of the 4th of July weekend. And now we have this delicious situation of both reports on the same day, with the Labor Department’s unemployment insurance data – people who are actually receiving unemployment benefits under state and federal programs – calling the Bureau of Labor Statistics’ survey-based report a liar. And we’ll go through them.

What the Labor Department reported today:

The total number of people who continued to receive unemployment compensation in the week ended June 27 under all state and federal unemployment insurance programs, including gig workers, surged by 937,810 people in the week, to 31.49 million (not seasonally adjusted), the highest and worst and most gut-wrenching ever:

snip...

'Big banks couldn't be happier': Stocks surge as Trump regulators gut restrictions on risky Wall St.

‘Big banks couldn’t be happier’: Stocks surge as Trump regulators gut restrictions on risky Wall Street gambling

https://www.rawstory.com/2020/06/big-banks-couldnt-be-happier-stocks-surge-as-trump-regulators-gut-restrictions-on-risky-wall-street-gambling/

Bank stocks jumped and lobbyists rejoiced Thursday after U.S. regulators voted to gut the so-called Volcker Rule, a set of regulations imposed in the wake of the 2008 Wall Street collapse limiting the ability of financial institutions to engage in high-risk behavior that threatens the systemic health of the economy.

“This is no longer the Volcker Rule. In the hands of revolving door regulators, it turns banks into Trump casinos. Will the inevitable Trump casino bankruptcy be far away?”

—Bartlett Naylor, Public Citizen

“Instead of protecting our financial system in the middle of an unprecedented economic crisis, Trump-appointed regulators are plowing ahead with their dangerous deregulatory agenda,” tweeted Sen. Elizabeth Warren (D-Mass.). “The big banks couldn’t be happier about it.”

CNBC reported that the shares of JPMorgan Chase, Goldman Sachs, Wells Fargo, and Morgan Stanley “were all trading more than 2% higher” after the changes to the Volcker Rule were announced by five regulatory agencies, including the Federal Reserve, the Securities and Exchange Commission, and the Federal Deposit Insurance Corporation.

The changes, set to take effect on Oct. 1, will make it easier for big banks to devote more of their resources to investments in venture capital funds and other vehicles—the kind risky of speculation that sent the entire U.S. financial system into a tailspin in 2008.

snip...

Here's How John Bolton's Lawyer Just Threw Him Under the Bus

https://www.thedailybeast.com/john-boltons-trump-white-house-book-is-due-out-soon-but-his-lawyer-just-threw-him-under-the-bus-2snip...

Then his lawyer, Chuck Cooper, wrote a Wall Street Journal op-ed this week intended to put public pressure on the White House. In it, Cooper volunteered that Bolton had violated both his NDA and perhaps a few criminal laws, including the Espionage Act. Now, even if Bolton’s book is never released, he is facing stiff penalties. As unforced legal errors go, that’s a doozy.

Here are the two sentences that could cost Bolton a big stack of money, or worse: “He instructed me, as his lawyer, to submit the manuscript to Ellen Knight, the NSC’s senior director for prepublication review of materials written by NSC personnel. I sent Ms. Knight the manuscript on Dec. 30, days after the House had impeached the president and amid speculation that the Senate would subpoena Mr. Bolton to testify.”

See, here’s the thing about prepublication review: “Publication” means giving potentially classified information to anyone the government has not approved to receive it. Bolton and his lawyer committed one of the classic blunders that a national-security lawyer would have seen coming a mile away. Simply put, someone who has signed an NDA and received a clearance has to put anything they want to write through prepublication review before they can give it to anyone. Even their lawyer.

Lawyers who represent intelligence personnel drill this into clients at the very beginning. I regularly have my clients—especially the whistleblowers—write everything they want to tell me and send it to the prepublication review office before they tell me a single word of it. It’s a major hassle, and sometimes it alerts the agency that a lawyer is involved, but it keeps them from losing their clearances or their freedom. Some agencies—like the Central Intelligence Agency—will outright refuse to even discuss a prepublication review matter with anyone but the author, let alone allow the lawyer to submit the document.

snip...

America Convulses in Pain, Fed Bails Out the Wealthy

https://wolfstreet.com/2020/06/11/america-convulses-in-pain-fed-bails-out-the-wealthy/snip...

So there are some huge multi-faceted problems that need to be grappled with, and that need to be resolved, and people are hurting, and they’re frustrated, and they’re angry, and many are unemployed, and others have jobs that don’t pay enough to meet the rising living expenses, and small businesses are on the ropes, and there’s going to be a lot of pain.

And what does the Federal Reserve do?

It printed $2.9 trillion since early March to bail out investors in highly leveraged hedge funds that were imploding, and to bail out investors in highly leveraged mortgage REITs that were imploding, and to bail out asset holders whose stocks were plunging, and speculators in the riskiest concoctions, and investors of all kinds, and to bail out asset holders of any kind – and the wealthier they were, the more they got – to make sure they don’t feel any of the pain.

That’s what the Fed is doing.

So the Fed printed $2.9 trillion since early March. That’s about $22,000 per household. For the bottom half of households, $22,000 would have helped a lot to get through the crisis.

But this money wasn’t spread to them. It was helicopter money for Wall Street. And it went on to multiply. And most of it ended up with a relatively small number of households. And their wealth increased by the trillions of dollars.

snip...

The Looming Bank Collapse

The Looming Bank Collapse

The U.S. financial system could be on the cusp of calamity. This time, we might not be able to save it.

https://www.theatlantic.com/magazine/archive/2020/07/coronavirus-banks-collapse/612247/?utm_source=pocket-newtab

After months of living with the coronavirus pandemic, American citizens are well aware of the toll it has taken on the economy: broken supply chains, record unemployment, failing small businesses. All of these factors are serious and could mire the United States in a deep, prolonged recession. But there’s another threat to the economy, too. It lurks on the balance sheets of the big banks, and it could be cataclysmic. Imagine if, in addition to all the uncertainty surrounding the pandemic, you woke up one morning to find that the financial sector had collapsed. You may think that such a crisis is unlikely, with memories of the 2008 crash still so fresh. But banks learned few lessons from that calamity, and new laws intended to keep them from taking on too much risk have failed to do so. As a result, we could be on the precipice of another crash, one different from 2008 less in kind than in degree. This one could be worse.

snip...

After the housing crisis, subprime CDOs naturally fell out of favor. Demand shifted to a similar—and similarly risky—instrument, one that even has a similar name: the CLO, or collateralized loan obligation. A CLO walks and talks like a CDO, but in place of loans made to home buyers are loans made to businesses—specifically, troubled businesses. CLOs bundle together so-called leveraged loans, the subprime mortgages of the corporate world. These are loans made to companies that have maxed out their borrowing and can no longer sell bonds directly to investors or qualify for a traditional bank loan. There are more than $1 trillion worth of leveraged loans currently outstanding. The majority are held in CLOs.

I was part of the group that structured and sold CDOs and CLOs at Morgan Stanley in the 1990s. The two securities are remarkably alike. Like a CDO, a CLO has multiple layers, which are sold separately. The bottom layer is the riskiest, the top the safest. If just a few of the loans in a CLO default, the bottom layer will suffer a loss and the other layers will remain safe. If the defaults increase, the bottom layer will lose even more, and the pain will start to work its way up the layers. The top layer, however, remains protected: It loses money only after the lower layers have been wiped out.

Unless you work in finance, you probably haven’t heard of CLOs, but according to many estimates, the CLO market is bigger than the subprime-mortgage CDO market was in its heyday. The Bank for International Settlements, which helps central banks pursue financial stability, has estimated the overall size of the CDO market in 2007 at $640 billion; it estimated the overall size of the CLO market in 2018 at $750 billion. More than $130 billion worth of CLOs have been created since then, some even in recent months. Just as easy mortgages fueled economic growth in the 2000s, cheap corporate debt has done so in the past decade, and many companies have binged on it.

Despite their obvious resemblance to the villain of the last crash, CLOs have been praised by Federal Reserve Chair Jerome Powell and Treasury Secretary Steven Mnuchin for moving the risk of leveraged loans outside the banking system. Like former Fed Chair Alan Greenspan, who downplayed the risks posed by subprime mortgages, Powell and Mnuchin have downplayed any trouble CLOs could pose for banks, arguing that the risk is contained within the CLOs themselves.

snip...

Fears grow of an eviction apocalypse

https://www.axios.com/eviction-crisis-coronavirus-351bb693-a04f-4ea1-a27d-dceb5163af14.htmlMost states paused evictions when the coronavirus hit — but those holds are expiring at about the same time that more generous unemployment benefits are set to dry up.

Why it matters: The one-two punch could easily exacerbate the housing crisis for Americans already bearing the worst of COVID-19's effects.

One fifth of adults polled in May said they had slight or no confidence they would be able to pay their rent or mortgage due in June, according to a weekly Census survey measuring COVID-19’s impact on Americans.

An Urban Institute analysis of Census data found nearly 25% of black renters deferred or did not pay their rent last month, compared with 14% of white renters.

In Michigan, courts are bracing for "a coming deluge" of as many as 75,000 landlord/tenant filings. (The state's moratorium expired this week.)

The big picture: The pandemic — which forced an economic collapse — is adding new burdens on top of the country's longstanding housing problems.

"There was a supply and affordability problem before, and the opportunity for it to get a lot worse presents itself, unless there's really good support coming from the federal, state and local level," Paula Cino of the National Multifamily Housing Council, a trade group for the apartment industry, tells Axios.

snip...

Profile Information

Name: DoloresGender: Female

Hometown: California

Home country: USA

Current location: California

Member since: Thu Nov 30, 2017, 02:58 PM

Number of posts: 5,063