General Discussion

Related: Editorials & Other Articles, Issue Forums, Alliance Forums, Region ForumsPSA - If you enroll in Medicare Advantage, you could be stuck for life

When you initially sign up for Medicare at 65, you take one of two routes. You can take either of these, with no health questions -

1) Medicare Advantage (PRIVATE insurance)

2) Original Medicare with a Medigap supplement (public insurance - far superior in providing care)

If choose 1)Medicare Advantage and decide later you want to switch to 2)Original Medicare with a Medigap supplement, you are subject to medical underwriting, meaning if you have developed a serious health condition you will likely be denied.

AFIB

Stroke

Cancer

Some types of diabetes

Multiple Sclerosis

Kidney disease

Rheumatoid Arthritis

Heart disease

Numerous others

There are many stories of people on Medicare Advantage developing serious health issues like these and finding their care inadequate. They want to switch back to Original Medicare with a Medigap supplement but are denied. They are quite possibly stuck for the rest of their lives.

Something to consider.

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

DFW

(60,842 posts)Supposedly, on paper, anyway, the only medical insurance I really have is Blue Cross of Texas, which in reality means I have no medical insurance at all. They are John Grisham's "Great Benefit." They deny EVERYTHING.

Grasswire2

(13,849 posts)And a key distinction is this:

Medigap plans are standardized. You know exactly what you are getting, and it is regulated by law.

Advantage plans are all over the place in terms of benefits. It is complicated to compare each policy to another. They'll try to bamboozle you and sell you stuff.

Celerity

(55,412 posts)https://prospect.org/health/medicare-advantage-is-a-massive-scam/

If you’ve ever watched cable news, where the average viewer is in their late sixties, you’ve probably seen an advertisement for a Medicare Advantage plan. They usually star some washed-up celebrity whose career peaked right around when today’s retirees were young adults (think Jimmy Walker or Joe Namath). And they always make a lot of big promises about how great Medicare Advantage coverage is. There’s just one problem: The sales pitch is an abject lie. Medicare Advantage is much worse than traditional Medicare for people on the program and costs a great deal more to boot. But unless the Biden administration changes course, private companies will soon devour the rest of the program.

Medicare Advantage plans are typically a combination of “Medigap” plans, which cover services not included in the government plan like vision and dental, plus a privatized version of traditional Medicare. About 28 million American seniors are now on Advantage plans, or about 40 percent of the whole program. As Barbara Caress explains in the Prospect, it was set up back in the late 1990s as a way for those wonderful private insurance companies we all know and love to work their free-market magic on one corner of the system America carved out as publicly run. Once we got business involved, surely the quality of coverage would improve and costs would go down, right?

The problem with this logic, as people realized even back in the glory days of neoliberalism, is that there are a lot of perverse financial incentives in health insurance, particularly when it comes to seniors. Half the reason the government set up Medicare in the first place was that as people reach the end of life, they tend to become sick and require more treatment than they can personally afford. In the pre-Medicare days, private companies did all they could to keep them off the insurance rolls.

Introducing the profit motive into Medicare has led to considerable hoop-jumping just to prevent such cravenness. For instance, if the government were to calculate the average per-person cost of Medicare and pay private companies that much per enrollee, companies would scramble to snap up all the younger, healthier seniors with relatively few problems, and cream off some easy profits. As Matt Bruenig explains, that’s why the Centers for Medicare & Medicaid Services maintains a gigantic database of every single one of the roughly 64 million Medicare enrollees, and assigns them all a risk score based on their demographic and health characteristics. Advantage companies then get paid, in theory at least, according to how sick their risk pools are.

snip

Just Jerome

(611 posts)To you, Celerity!

ShazzieB

(23,103 posts)This is exactly the kind of thing I need: informational sources complete with links. I will definitely make use of this, thanks.

JCMach1

(29,272 posts)Worked awesome for my father with dementia, but it really shouldn't be so random

Caveat emptor

LiberalFighter

(53,544 posts)Those part of a group that do the negotiating get better results.

True Blue American

(18,579 posts)Celerity

(55,412 posts)True Blue American

(18,579 posts)Joe Namouth ? He gets paid for scare tactics. I have been spending a lot of time helping people understand all the disinformation. Much of it from younger people trying to help their parents. I can not tell you how many have thanked me when they find out what is available .

Celerity

(55,412 posts)techniques used to sell/push Medicare Advantage by some of the firms.

Perhaps I am misreading your reply, and you are not taking issue with the article including them.

If so, I apologise in advance for my error.

True Blue American

(18,579 posts)I am simply asking people to check. Our Union put us on Anthem Blue Cross when private plans were lost. But each area is different. That is why I keep saying back of Medicare book. No one will robot call you from checking that book

allegorical oracle

(6,713 posts)while you, the customer, are stuck with the terms of the contract, the plans reserve the right to change the terms if they want to. Went back to original Medicare.

NowISeetheLight

(4,002 posts)Do you have a supplement plan too? If so did you have to answer a bunch of questions and qualify?

True Blue American

(18,579 posts)To make it simple go to the back of your Medicare book. You choose the plan you want. Stop listening to the paid scare mongers!

Eliot Rosewater

(34,343 posts)once they do, costs for Advantage will skyrocket.

sprinkleeninow

(22,524 posts)getgo. Once enrolled in a plan, if a switch is under considerarion, there's underwriting along with skatey-eight health questions posed. And prices are considerably higher if any health questions answered in the affirmative.

dflprincess

(29,463 posts)their insurance agent told them to keep in mind that you marry your medical policy but only date your drug coverage.

sprinkleeninow

(22,524 posts)True Blue American

(18,579 posts)Check the back of you Medicare book. The plans are all there. There is a deductable.. All the best private plans have that too.

Silent Type

(12,412 posts)a month for MediGap and a drug plan. Many retirees can’t. That’s why 45% of beneficiaries choose Medicare Advantage.

But you are correct about getting caught in MA.

True Blue American

(18,579 posts)Medicare Advantage plan. AARP charges because they are an Insurance Company.

Do you own research but check the back of your Medicare book first.

allegorical oracle

(6,713 posts)insurance went up in Fla. One fourth of my SSec goes just to pay for that.

dpibel

(4,043 posts)You pretty sure about that?

Cuz I'm pretty sure that Medigap is PRIVATE THIEVING INSURANCE DUDE!

In any case, this is one of about 7.84 million DU threads about BEWARE THE ADVANTAGE!!!1!!

And pretty soon, a bunch of people may post here saying, "I have Advantage, and it works great!"

That's what usually happens anyway.

MOMFUDSKI

(7,080 posts)I have Advantage and it is all good. I will ask my Agent about this rule next time we speak.

dflprincess

(29,463 posts)but it's only there to cover what Medicare does not and, I believe, conforms to Medicare rules.

One of the problems with a strictly private plan like Medicare Advantage is that is can limit the network you're in, one of the larger hospital and clinic systems where I live just announced it will no longer accept Humana Advantage plans. They can't do that with traditional Medicare and gap policies. You're also more apt to need preapprovals and have care denied with Advantage.

Lonestarblue

(13,661 posts)I would not change for anything. I have no copays, no waits to get recommended to a specialist, and I pay nothing for my routine annual checkups and my more sporadic tests like colonoscopies. I know others here feel the same about their advantage plans, but those plans are not controlled by the government in terms of coverage and treatment. I’d rather know I have guaranteed treatment than rely on an insurance company person more concerned about the bottom line to decide whether I’m worth treatment.

dflprincess

(29,463 posts)the insurance companies run so many commercials and send so many mailings pushing Advantage plans. It's pretty safe to assume it's not because they love us and want us to be healthy.

DemBlue76

(78 posts)True Blue American

(18,579 posts)elocs

(24,486 posts)I'm under the 100% Federal Poverty Level and have dual coverage--Medicare pay first, then Medicaid. I pay nothing, zero, zilch. No copay for the single med I take. I had an MRI last year as well as an EMG and paid nothing. Every month I receive $200 that I can use for otc products, healthy food, or even to pay on my utility bill. What good is original Medicare if I can't afford it? Having a Medicare Advantage plan was my choice and I don't regret it for a moment. Aren't those of us on the Left supposed to be in favor of choice?

Silent Type

(12,412 posts)traditional Medicare is the best for everyone, but they are wrong. And I have traditional Medicare, but if Kaiser moves coverage area a few counties, I’m probably in.

IbogaProject

(6,192 posts)As you are qualified for medicaid health coverage by agreeing to limit to a specific network you've been ok for now. The issue is your local hospitals and medical practices. Those providers can decide to no longer accept your coverage. My mom is on Medicare Advantage, but not from the start, she has that from her state coverage that was her first gap and she also gets the old military coverage. But now her hospital and their huge practice decided to drop accepting Aetna, so she had to switch. Basically she has to go to a different gap policy from the state and Tricare will be covering more. So the state of NJ is getting out of properly honoring their retiree coverage. This is all insane, we would all be covered nearly as well for less money with having one single payer insurance coverage.

True Blue American

(18,579 posts)Medicare Advantage costs nothing. You pay for Medicare. That comes out of your SS check, accroeding to inco

elocs

(24,486 posts)True Blue American

(18,579 posts)Most of us pay for Medicare based on income.

Trueblue Texan

(4,723 posts)I just got on Medicare, so I know it will go up as I age...they all do. But I know from working in healthcare, it is a big MISTAKE to get an advantage plan. I got the medigap plan G. It covers everything but the Medicare Part B premium and the annual deductible which is less than $250. I would NEVER get a medicare advantage plan.

GoodRaisin

(11,204 posts)Now it’s $179 a month in year 5. I still wouldn’t trade for a “Medicare Part C” plan.

Ms. Toad

(38,915 posts)The Medigap plans are dictated by law. Each lettered plan is required to provide the same stuff as all other plans with the same letter. You are covered everywhere in the country (and, for some plans, out of the country). The bill goes first to Medicare. They make all decisions as to coverage. Once Medicare determines the procedure is covered, the remainder of the bill is sent to Medigap, which covers it - no questions asked - at the rate dictated by law. So while it is private insurance, there is virtually no wiggle room for the insurance company to play games - aside from what they charge you for the premium. So pick the letter plan that covers what you need covered, and choose the insurance company that charges the lowest rate for that plan.

Medicare Advantage, on the other hand, is closer to the insurance people are used to (which is one reason people like it - it's the devil they know). Each provider can limit your care to a small pool of doctors. They can require pre-approval for certain procedures, they can limit your care geographically, etc. As a practical matter, they deny a lot of care that Medicare requires them to cover - and get away with it because people aren't used to challenging insurance decisions.

The other reason people like Medicare Advantage is that they have not yet hit the kind of chronic illness which means they will be paying the maximum out-of-pocket expenses each and every year. That is the point at which they typically want to switch and are unable to without paying significantly more.

at140

(6,287 posts)And so is my wife also. Her cancer treatment bills run between $3500-$4000/month

She pays first $4500 out of pocket (for doctor, hospital, prescription drugs, lab tests etc) for the year, and zero dollars after that.

We both get $120 added to our social security checks every month.

And we both get $750 debit card every year to use at eye doctor, hearing doctor or dentist office.

And we each get $240 worth OTC products sold at pharmacy.

We are NEVER going back to Medicare.

not fooled

(6,823 posts)because enough seniors have been lured into signing up for private insurance. Evil but effective scheming by chimpy's cabal--get people to voluntarily give up Medicare for private insurance.

Once enough have volunteered for private insurance, just watch--real Medicare will be ended, because after all, the 'Murican people have spoken--they clearly prefer private insurance.

Then, watch the coverage go in the crapper. What do you think will happen once private health insurance executives and Wall Street are deciding what to cover? They are making it nice for you now because they want the numbers to increase to the point where real Medicare can be ended, but just wait until they no longer have goverment Medicare as competition. It's going to be the ultimate bait and switch.

Let the death panels begin, in earnest!

Good luck to you with your coverage.

at140

(6,287 posts)required for my wife. Not once! Every expensive PET scan is approved without question.

Then add up the additional dollars Medicare advantage is giving us. Medicare adds zero.

My wife has stage-4 cancer, I am in my 80's. Are we worried about Medicare privatized?

Sure, realistically how many more years we got left? We need the cash benefits now.

My husband has stage four cancer and we have an Advantage plan through my husband’s generous ex employer. The plan has been great and they’ve covered everything so far without question - plus we have no deductible, no copays (except a small amount for medications), and access to any provider who accepts Medicare. I hope this continues forever, but just in case, can I ask who your Advantage provider is?

at140

(6,287 posts)My wife was diagnosed stage-4 5.5 years ago. She has already beaten the 5 year expected maximum survival period. She is doing OK. In my opinion the radiation treatments were most effective. 17 tumos in brain zapped, and she recovered from that.

And congrats to your wife on her remarkable recovery! My husband is going on four years with stage 4.

DemBlue76

(78 posts)In my area Advantage Plans all have a maximum out of pocket around $5,000. So if we have a serious illness like you're describing, we'd pay more than premiums would be on a Medigap policy.

at140

(6,287 posts)My wife was diagnosed stage-4 5.5 years ago. She has already beaten the 5 year expected maximum survival period. She is doing OK. In my opinion the radiation treatments were most effective. 17 tumors in brain zapped, and she recovered from that. Medicare Advantage has been really good insurance so far.

True Blue American

(18,579 posts)at140

(6,287 posts)you just throwing out your opinions?

True Blue American

(18,579 posts)And just left a 7 day stay in the cardiac unit and rehab.

at140

(6,287 posts)My wife is on M-A for 6 years. She was diagnosed stage-4 lung cancer metastasized to brain and ribs.

Medicare Advantage through Humana has served us extremely well. No issues whatsoever.

On top of that we get $1500 gift cards for the year to use for vision/hearing and dentist visits.

This year I got myself high end rye glasses for indoor and sunglasses plus high end brand new hearing aid, and it cost me nothing.

Plus we get $250 added to our social security checks every month. And total pot of pocket is also reasonable, after which M-A covers every expense.

True Blue American

(18,579 posts)Last edited Tue Jul 11, 2023, 08:55 PM - Edit history (1)

Affected me adversely?

I praised them from the beginning..

. And after my experience in a heart incidence, 7 days in the hospital, 7 days in rehab approved immediately and now cardio therapy at my home I am very happy with Anthem Medicare Advantage.

I think you are mixing me up with someone else. All my posts praise Medicare Advantage.

I posted that I was in the hospital a couple of weeks ago with heart failure from low sodium it took them 3 days of cardiologists working to stabilize me.

I have a stack of Anthem Medicare Advantage papers that I owe nothing, including paying for 7 days in rehab to recuperate and get cardio therapy.

I paid one copay where I was admitted to the ER. That was $90.00 two weeks of Medication care at the best Cardiologist Hospital in this are. Now, I am on medications to heal my heart.

I would never criticize Medicare Advantage.

at140

(6,287 posts)I will never go back to Medicare unless forced.

True Blue American

(18,579 posts)I am still getting cardio therapy at home. am better each day.

ariadne0614

(2,210 posts)

MichMan

(17,677 posts)

peppertree

(23,590 posts)Clinton also signed NAFTA (Old Man Bush's baby) and rescinded Glass–Steagall - Phil Gramm's great mission in public life (besides getting filthy rich).

I think even he would admit that, whenever he caved to GOPee pressure, disaster always followed.

Celerity

(55,412 posts)of the MSM and the telecoms/internet, and helped to turbocharge Fox News, amongst other bad outcomes) and the odious Commodity Futures Modernization Act (CFMA), the re-legalised most forms of the weapons of financial mass destruction (derivatives, including OTC, non-exchange based trading of them) that had been banned since FDR days. This played a huge underpinning, foundational role in the global financial crisis of 2007-2009.

peppertree

(23,590 posts)Clinton believed that if Democrats didn't become 'corporate-light', they'd get steamrolled by the increasingly radicalized GOP for decades to come.

But before long, he ended up giving them so much of what they wanted - and they themselves hadn't been able to get.

Plus - oh, irony - what you mentioned (plus NAFTA) ended up becoming the very reasons Hillary couldn't win, years later.

As Neil Young put it: the same thing that makes you live, can kill you in the end.

progressoid

(53,590 posts)

keopeli

(3,582 posts)The "third way" was always a slower route to privatizing everything for money.

peppertree

(23,590 posts)I believe he really did believe that if he didn't go along with at least some of these changes, Democrats would become permanently shut out of the White House.

And to an increasingly radicalized GOP besides.

But - oh, irony - it was precisely those policies (NAFTA, certainly - which wasn't even his baby) that ended up costing Hillary the White House years later.

Murphy's Law.

keopeli

(3,582 posts)GQPers cried, "She's the President's wife! She shouldn't be allowed to chair a government effort!" Of course, having the President's daughter and son-in-law run the US Foreign Policy was never an issue.

I believe the GQP thought they would rule forever after Reagan and the angry people (i.e. Gingrich, Limbaugh) took over the party when HW Bush was denied a second term. We all know it was Ross Perot that killed HW's Presidency and his own culpability in Reagan's crimes (not to mention the Keating 5), not the Democrats.

Yet, it was Hillary (and all of us) that have paid the price for Clinton's "third way", aka capitulation.

Silent Type

(12,412 posts)Celerity

(55,412 posts)peppertree

(23,590 posts)I was thinking of the '96 Telecommunications Act.

But it was Bonzo who gave Murdoch the jewel in his crown: repealing the Fairness Doctrine.

(and his fast-track citizenship, of course - thus allowing him to swallow up U.S. media)

Celerity

(55,412 posts)right before I was born, so no Fox-free world for me ever.

FOX NEWS Channel Fox News Now Launch October 7, 1996

keopeli

(3,582 posts)Thanks for the information!

True Blue American

(18,579 posts)The AMA CHANGED EVERYTHING FOR seniors. That wa Obama and Biden? Remener that Fen big deal! It was and now abiden is working on drug prices. He already lowered Insulin for diabetics. $35 .

Just Jerome

(611 posts)Medicare Advantage is a Trojan Horse. When actual Medicare is toppled, it will be like the end of The Twilight Zone episode, “To Serve Man.” IT’S A COOKBOOK!

Too late.

Traildogbob

(13,337 posts)But Advantage is free, they put money back into your SS, free dental, free vision, free organ transplants, they even pay your mortgage. All free. They even cover your pets for free. They offer Auto coverage under your plan for $2.00 per year. It’s free. They pay you. J.J. Explains it all. Shatner would not lie. How much do they pay for endless commercials and mail? How much does Medicare take from your premiums for commercials and mail?

Advantage lied to scam me in. And the VA was gonna end my coverage because Advantage denied everything. Took a year of letters and proof the agent lied me into it to get out.

Don’t wanna hear your success stories. It’s a scam, when they drain enough to sink Medicare just watch the for profit American health care work it’s magic.

My family were carnies. They knew how to make a few look like winners when crowds gathered at the carnival games. Then milked the rest after the felt could win too. No health insurance is free. Those greedy CEO’s are like all of em. Shine the knobs of a few, suck em all in, then fuck em. The American Corporate plan.

Just wait until GQP crank out the Social Security Advantage plan.

They want to kill the entitlements. And this is their game.

Vdizzle

(391 posts)When it comes to healthcare, a profit motive should never, ever, ever, ever, EVER!, come into play. Ever. Full stop. No excuses, no false reasoning, and no talking point is going to prove me wrong. For profit heath INSURANCE is wrong and always will be.

Silent Type

(12,412 posts)best to get Congress to provide a subsidy so they don’t choose a $200 to $400 a month premium/other savings by going MA. What are chances of Congress doing that?

Traditional Medicare is good for a lot of people, including me right now. But, MA advantage is good for a lot of others.

I don’t think they are as stupid as some seem to believe.

True Blue American

(18,579 posts)Check yourself.

dflprincess

(29,463 posts)but your are correct, you're never going back to Medicare because it would be nearly impossible for you to get gap coverage.

at140

(6,287 posts)I do not see any reason we would want to go back to regular Medicare. I was on regular Medicare for 17 years before Med-Adv. Every time we moved, I had trouble finding a doctor who would accept new Medicare patients.

That was more scary to me personally.

True Blue American

(18,579 posts)Medicaid is a different story. Many Doctors are refusing.

True Blue American

(18,579 posts)With Congestive heart failure. Everyone of my Anthem Medicare Advantage bills had zero deductable except the ER, even my 7 days in rehab.

moose65

(3,466 posts)How much is your premium?

Where does that $120 come from? Who pays for those other things you mentioned?

at140

(6,287 posts)That $120/month is added to our social security checks each month by my Medicare Advantage plan.

We have ZERO monthly premiums!

Our out of pocket is $4500/year and after that there are no bills to pay.

We get $750 gift cards each to use for vision, hearing or dental from M-A.

And we get $240 allowance each for the year to buy any over the counter stuff available from pharmacy of our M-A insurer, I load of on vitamins, skin creams, special socks, ibuprofen, etc what ever is needed. It is shipped free as well.

moose65

(3,466 posts)Don’t you have a part B premium?

This sounds too good to be true. I suspect it probably is.

at140

(6,287 posts)We pay no premiums. Yes, It has been too good to be true for 6 years. But why should I complain?

I am 83 and my wife has cancer. If this great health insurance lasts for another 6 years, I am gonna be very happy.

True Blue American

(18,579 posts)I paid nothing for 7 days in rehab, $90 for the ER. My Son was a benefits Adjuster for the Union. He paid $0 for a stent.He was having a heart attack while they were giving him an EKG FOR CHEST PAINS.. He was shocked how things have changed under the AMA.

My case was different, took Cardiologists 3 days to stabilize my sodium. But cancer patients pay nothing. The AMA changed their everything. So far the ER Copay.

I pay no premium. zero.

Wonder Why

(7,437 posts)https://medicareguide.com/medicare-advantage-to-original-medicare-180767]

Demobrat

(10,313 posts)as long as the care you need is in the network.

I have a close friend who is battling stage 3 colon cancer. His cancer is in a very difficult place. The surgeon he consulted initially could not do it and referred him to someone else. That person is in a different city.

He has traditional Medicare with a Plan G supplement thank goodness. If he had to stay within a network he would be doomed.

Trueblue Texan

(4,723 posts)..denied needed coverage for physical, occupational, and speech therapy in my experience, limiting visits to 2 or 3, regardless of the patient's need. A patient could be unable to feed or toilet himself without a dozen or more therapy visits minimum, and the advantage plan would pay for 3 visits. Forget what the patient needs, it's the profit that matters.

Silent Type

(12,412 posts)Believe it or not, doctors order a lot of stuff that ain’t necessary, especially when they profit from it. Yes, insurance companies profit too.

Trueblue Texan

(4,723 posts)at140

(6,287 posts)With M-A she has paid total out of pocket Less than $20,000 since she was diagnosed with stage-4 lung cancer 5+ years ago.

True Blue American

(18,579 posts)ariadne0614

(2,210 posts)Here’s his most recent explanation of the Medicare Advantage scam. The “free” perks offered are part of a long-term plot to kill real Medicare. Once that happens, watch all of those “advantages” disappear. The private insurers care about one thing—profits, not people.

https://hartmannreport.com/p/stop-the-medicare-advantage-scam?utm_medium=email

Rhiannon12866

(261,498 posts)

Rebl2

(18,011 posts)Rheumatologist warned me several years in advance not to sign up for MA. Have original Medicare and supplement from my husband’s company he retired from.

Attilatheblond

(9,509 posts)I was able to keep the fed plan when widowed and would be a fool to let go of it. Three levels/costs to pick from & I can change the level/policy during open season. Not cheap, but not as expensive as most, and with the number of fed employees in the group, Blue Cross/shield not likely to jerk us around. That and my medicare = really full coverage and no monkey business.

As more people fall for the advantage crap, they will find constant changes in network and coverage year to year. If enough go with the private carriers, Medicare will die and we will ALL be screwed. Private insurance is not reliable without competition.

Rebl2

(18,011 posts)Federal BC&BS too. I was told hold onto it as long as you can by, get this, another insurance company! That company told me you can’t do better than that considering the medication I have to take for RA.

Rhiannon12866

(261,498 posts)

MichMan

(17,677 posts)Medicare Part C. They even show all the plans and let you enroll from there.

Just Jerome

(611 posts)Part C is the result of big money having its way with government.

I urge everyone to check out Thom Hartmann.

Rhiannon12866

(261,498 posts)Thom Hartmann explained the dangers of many of these "part C" local offerings which are not official Medicare and how many who have subscribed have regretted it, depending on where subscribers live.

MichMan

(17,677 posts)To see which ones are available in your area.

Rhiannon12866

(261,498 posts)https://www.democraticunderground.com/100218060889#post14

Medicare Advantage Is a Massive Scam

The program rips off both the taxpayer and its own enrollees.

https://www.democraticunderground.com/100218060889#post47

It is a very, very limited private insurance.

https://www.democraticunderground.com/100218060889#post92

MichMan

(17,677 posts)Rhiannon12866

(261,498 posts)But I'm sure you remember the obstruction that President Obama faced attempting to pass the health care plan that he did - and that obstruction did and still does come from - not surprisingly - Republicans.

MichMan

(17,677 posts)Everyone over the age of 65 is covered by it

Rhiannon12866

(261,498 posts)And I have no idea about hospitalization, but I'm willing to bet it's not 100% - which has to be inordinately pricey.

MichMan

(17,677 posts)Medicare Part D is optional and covers prescription drugs. Available for anyone on Medicare to choose if they like.

FYI, Most MA plans cover both drugs and dental

True Blue American

(18,579 posts)Covers what Medicare does not. Medicare only pays 80%. Medicare Advantage covered all my bills for a heart episode I just went through. It also paid for 7 days in cardio therapy and is now paying for home cardio care.

And you can change every year if you wish during enrollment.

Rhiannon12866

(261,498 posts)https://www.democraticunderground.com/100218060889#post14

Medicare Advantage Is a Massive Scam

The program rips off both the taxpayer and its own enrollees.

https://www.democraticunderground.com/100218060889#post47

It is a very, very limited private insurance.

https://www.democraticunderground.com/100218060889#post92

True Blue American

(18,579 posts)Has been saying that. Surprises me because he is leading people down the wrong path.

I have to ask how is it a scam when it costs you nothing to recieve all these extra benefits but pay nothing? How could it be a scam? Where is the cheat?

Rhiannon12866

(261,498 posts)Sounds like you were lucky, too many were not.

Medicare Advantage's For Profit Assault On Medicare Exposed - Thom Hartmann

For Profit Companies are stealing from Medicare through Medicare Advantage. Thom Hartmann breaks down the latest assault on Medicare by Medicare Advantage.

This “Medicare” is No Advantage…Could Cost You Millions Featuring Alex Lawson - Thom Hartmann

Medicare Advantage ads obscure the often-life-threatening restrictions and bank-account draining demands that are common in Medicare Advantage plans. Alex Lawson from Social Security Works explains.

The New Medicare Advantage Plot Exposed Featuring Alex Lawson - Thom Hartmann

Medicare Advantage is a scam that is tricking you into giving your Medicare to private for profit institutions. Alex Lawson explains the latest scam from the privatizers of Medicare.

drmeow

(6,043 posts)mostly out of principle. Medicare should not be privatized and anything other than traditional Medicare is a slippery slope to privatization of the whole system. I am not willing to support that (and I have the luxury, if it is more expensive for me, not to).

True Blue American

(18,579 posts)It is taken out of yoour SS!

MichMan

(17,677 posts)True Blue American

(18,579 posts)My recent stay in the Cardiology Unit showed me how much Medicare Advantage pays, free rehab.thanks to the AMA. That program costs me nothing and I get more benefits each year to allow me to stay in my house. That costs me 1/4 of what a retirement Center would! I hire outside work done. Life alert, extra money for the things I need. I can even choose groceries. Then another $65 every 3 months for OTC drugs

drmeow

(6,043 posts)which you have to have to enroll in a Medicare Advantage plan, if that's what you mean.

True Blue American

(18,579 posts)Medicare AdVantage not only pays the rest it provides many extras. Free OTC DRUGS., $500 for optical, Dental or HADS,Now they have come out with free groceries. Silver Sneakers, that is a gym plan. Free Life Alert.

I save hundreds of dollars each year. And it costs nothing.

The plans are all right in the back of your Medicare book. Check there first.

drmeow

(6,043 posts)Furthermore - you don't know my life circumstances nor are you my financial or health advisor. Why do you care and why are you pushing Medicare Advantage so hard?

True Blue American

(18,579 posts)Been on Anthem Medicare Advantage since our Union put us on it. Had Anthem my whole working life. When I looked at my statements from my recent Hospitalization I was quite happy.

SickOfTheOnePct

(8,710 posts)“I don’t want Medicare Advantage, so no one else should like or have it either”

SammyWinstonJack

(44,319 posts)True Blue American

(18,579 posts)dflprincess

(29,463 posts)It will eventually bite us all in the butt as the private insurers maximize their profits.

They don't push these plans because they care about our health.

Skittles

(173,695 posts)it's DO YOU WANT MEDICARE TO EVENTUALLY GO PRIVATE? Because THAT is the plan.

SickOfTheOnePct

(8,710 posts)People to be able to use the plan that works best for them and their financial situation without others trying to shame them or tell them how stupid they are.

In every single one of these “MA is the devil” threads, multiple people post about what great care they get, how much cheaper it is for them, etc., and then scolds come along tell them they’re wrong.

Adults who are 65 or older are able to figure out what’s best for them better than strangers on an internet discussion board can, and it’s insulting to believe otherwise.

Skittles

(173,695 posts)OVER AND OUT

Elessar Zappa

(16,385 posts)and don’t give a damn about the greater good. Sad to see it on a liberal site.

SickOfTheOnePct

(8,710 posts)Since you seem to prefer yelling .

yellowdogintexas

(23,781 posts)the first time. if you decide to go back to the Advantage Plan you will have to go through Underwriting.

Or if you move to Part B after being on an advantage Plan

It's the returning to your former plan that causes the problem I think

I started out with Part B and added a supplement later. No issue since I was very healthy.

Of course, stuff changes. I recommend you inquire at Medicare.gov if you plan any changes.

MiniMe

(21,883 posts)I turned 65 last year, and I stayed well away from the advantage. So far, I am happy with Medicare with a Medigap supplement.

orleans

(37,507 posts)i have no idea about any of this and my time is coming up in the fall!

my friend has MA but i've heard thom hartmann downtalk it and it's just all a bit daunting and confusing for me. i hesitate to do MA but i don't know if i could afford the real thing.

to check out different supplemental insurance companies plans. My parents had whatever AARP offered and they had different plans to choose from and of course the amount you paid varied depending on the plan you chose. My parents chose one of the more expensive plans and they rarely had to pay for anything after they met their deductible for Medicare and the supplemental plan.

Zorro

(19,037 posts)You'll also have to add the monthly Medicare Plan D premium for prescription drug coverage, and also budget the cost of the meds.

True Blue American

(18,579 posts)I pay 0 for Medicare Advantage.

Zorro

(19,037 posts)Medigap plans are not Medicare Advantage plans.

True Blue American

(18,579 posts)Medigap plans were sold by the AARP. MY sons MIL WAS on one, PAID $270 a month. When mentioned the cost of MA, nothing, she said she did not want to change Doctors again. She passed 5 years ago.

ShazzieB

(23,103 posts)My husband is still working, so we have insurance through his employer for now. When he retires, we'll have to make some big decisions, and everything I hear about this stuff just confuses me more.

A lot of people here are adamant that MA is the devil, but i the past I have rarely seen a source cited for where their information is coming from. I alpreciate that some in this thread are providing specific information sources with links, rather than just horror stories and conspiracy theories about how all the evil insurance companies are trying to kill medicare. I am going to investigate some of these links, so thanks to one and all!

orleans

(37,507 posts)omg!

my mind reels

someone upthread posted this link to one of hartmann's essays (from 2022) -- i started reading it but was losing focus, so i'm emailing the link to myself for future reference.

https://hartmannreport.com/p/stop-the-medicare-advantage-scam?utm_medium=email

he is on wcpt (820 am in chicago area) weekdays from 11 - 2 (after stephanie miller and before joan esposito)

anyway...

liberal N proud

(61,207 posts)orleans

(37,507 posts)don't know what to do

moonscape

(5,822 posts)Original Medicare with a Medigap policy, I would strongly recommend it. You can always switch to Advantage, just not the other way around. I am bombarded by Advantage insurers every year wanting my business.

I got cancer the month of my 65th birthday, and am very grateful to have Original vs Advantage.

yonder

(10,325 posts)I went with Medicare, a supplemental plan (Medigap) and a low-cost dental/vision plan as did my wife when she became eligible. We are so glad we made that choice and have not regretted it.

Consider all the MA adverts pushed at you and ask yourself how can they afford that. They claim 0 this and free that which may be true as they reel us gomers in, but just wait until they can squeeze the life out of traditional Medicare. Remember 40-50 years ago when the insurance industry started pushing "Managed Health Care"? The next best thing since sliced bread right? All we had to do was let them place themselves between us and our doctors, let them negotiate on our behalf and everything will become cheaper, easier, pain-free, etc. How did that work out?

From memory, administrative costs for MA average 30-40% while Medicare are somewhere around 5%. There's a reason for that.

Your state may offer a free of charge, state-run program which can guide you in this unnecessarily complicated but necessary decision. If nothing else, take the excellent advice in post #59. Begin with traditional Medicare/Medicare. You can easily move to a MA plan. But not the other way around.

Good luck

orleans

(37,507 posts)liberal N proud

(61,207 posts)But, I am not trusting some TV commercial or anyone who calls me to sell their gimmick

orleans

(37,507 posts)unfortunately (lol) i'm either not here ("no, she's not here" ) or i can't talk ("i can't talk right now" )

i missed a perfect opportunity this afternoon; this girl said "hi, i'm looking for _____" (my name) and i SHOULD have said "OMG! we've all been looking for her too! no one knows where the hell she is!"

but i didn't think of it fast enuf

but again, i didn't talk to her.

liberal N proud

(61,207 posts)I always mess with them if I have time

TheBlackAdder

(29,984 posts)

slightlv

(8,220 posts)Your costs are much, much higher than those who chose Medicare/Medigap in the beginning. It's almost as bad as Cobra pricing.

Yes... choose Medicare Advantage, and you ARE stuck for life. This is so unfair, IMNSHO. And it's one of my hot buttons. They should not be able to call this "Medicare Part C" coverage, for example. This infers that it's part of Medicare, which it is not.

Another difference is... if your specialist wants you in for an MRI or CT Scan, Medicare will pay for it with no prior arrangements. Medicare Advantage will give you the runaround, just as you get now on your insurance plan. IOW, I have a horrible back. Rheumatologist wants to give an MRI to see where the problem, exactly, is in the back. However, Medicare Advantage won't allow it until you've done a year of physical therapy. Sound familiar? Basically, Medicare Advantage is your current low-rent ppo or hmo insurance.

And pay special attention to your drugs under Medicare Advantage. Several have "must have approval" before MA will allow you to have them. Also, I've found SingleCare and GoodRX to beat the prices, even with drug coverage under MA.

The at I got tricked into getting the MA isn't my main point, although DO watch out for unscrupulous brokers. I flat out told mine I did NOT want to enroll at this moment. I had several more companies, as well as Medicare paths, to check out first.

When I went the next day to get my meds at CVS, everything had been switched over to Aetna Medicare Advantage, ditto on my primary care. THAT'S how I found out I was now enrolled in Medicare Advantage - Aetna, despite telling the broker I did NOT want to this. That's when I discovered all the "dings" you get in Medicare/Medigap if you go with MA first. Despite not even having been on it a full day, I was still subject to the rule.

If you have nothing wrong with you and are looking for insurance that will include drug costs, MA might be okay. But most seniors I know are being treated for several issues - and at least one issue that causes you to see a specialist. This is when MA will let you down, just like the ppo and hmo insurance in the corporate world when you're in your "prime."

MichMan

(17,677 posts)Who is they? The Federal Government?

The Government not only calls it Medicare Part C on the official Medicare website, they also allow you to apply for it there. Hard to complain that the various insurers call it that when it is referred to as such by the government itself.

slightlv

(8,220 posts)MichMan

(17,677 posts)I doubt he did it in an attempt to kill Medicare

Silent Type

(12,412 posts)moonscape

(5,822 posts)you can get a diagnosis that changes everything. It happens with us Seniors!

PortTack

(35,824 posts)

shanti

(21,809 posts)I had Kaiser while I was working my last 21 years, and it just seemed fine to keep what I had when I turned 65. So I did. I have nothing to compare it to, but it seems like a one-stop shop, cradle to grave and it's working for me. Nothing is perfect.

Riverman100

(283 posts)But My aetna medicare advantage has saved me thousands of dollars. I seldom disagree with you folks, but you may have good points, but your conclusions are bullshit

Celerity

(55,412 posts)

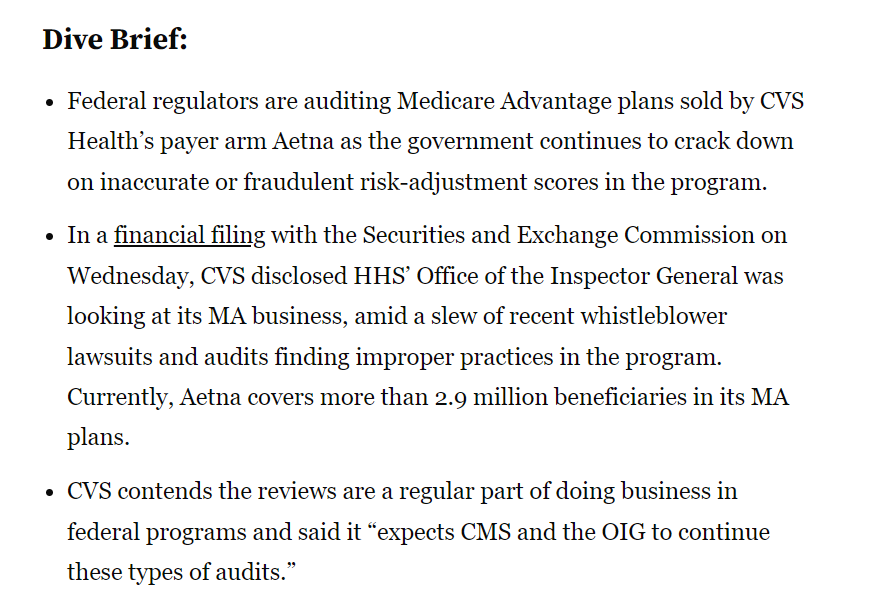

OIG audit targets Aetna’s Medicare Advantage plans as government cracks down on fraud

https://www.healthcaredive.com/news/oig-audit-targets-aetnas-medicare-advantage-plans-as-government-cracks-dow/604515/

Aug. 5, 2021

Dive Insight:

The federal government regularly audits health plans to ensure they comply with CMS regulations and aren’t gaming the system to secure higher payments. CMS pays plans on a per-member basis, then adjusts payments based on the acuity or severity of their member’s health status, as supported by provider data like diagnostic codes.

Typically, the sicker a member is, the higher the plan’s reimbursement. But as MA plans have grown to now cover more than 40% of all Medicare beneficiaries, so too has fraud and abuse. A 2020 OIG report found that MA paid $2.6 billion a year for diagnoses unrelated to any clinical services.

That’s resulted in the government stepping up its efforts to review and audit providers’ medical records to make sure they support the diagnostic codes that determine patients’ health status — and the resulting risk-adjusted premium payments to insurers.

Roughly a year ago, following a whistleblower complaint, the Department of Justice sued Cigna, alleging it falsified its MA members’ health statuses to nab an extra $1.4 billion in overpayments from CMS. Similarly, in April an OIG audit led the government to find Humana had overcharged CMS by almost $200 million using inaccurate documentation.

snip

grantcart

(53,061 posts)I understand that you live in Europe and don't use it but your are consistently wrong about Medicare Advantage.

Usually you are citing sources that have an axe to grind.

My response in 75 below gives you links to government information and my experience.

This comment of yours is again, completely off the point.

There is fraud in Medicare, including regular Medicare and Medicare advantage but it isn't by the insurance companies but by the health providers.

1) Insurance companies in Medicare, Medicare Advantage and the Affordable Care Act all have a fixed gross margin which is called a Medical Loss Ratio and is generally fixed at 15 -20%

This means that insurance company's gross profit is not calculated on a bottom line result but is a fixed percent of sales. If an insurance company sells $ 100 million in premiums they will keep $ 20 million to pay for their advertising, administrative and net profit. Declining care or overcharging for care does not add to the bottom line.

2) Fraud or overcharging medicare (regular or advantage) comes from providers either making errors or deliberately committing fraud. I have seen both.

Before going to Banner I used Dignity health in Phoenix. They have terrible service and I switched and noticed that they got fined by the government for overcharging.

https://oig.hhs.gov/fraud/enforcement/dignity-health-agrees-to-pay-37-million-to-settle-false-claims-act-allegations/#:~:text=Dignity%20Health%20has%20agreed%20to,basis%2C%20the%20Justice%20Department%20announced

Dignity Health Agrees to Pay $37 Million to Settle False Claims Act Allegations

Dignity Health has agreed to pay the United States $37 million to settle allegations that 13 of its hospitals in California, Nevada and Arizona knowingly submitted false claims to Medicare and TRICARE by admitting patients who could have been treated on a less costly, outpatient basis, the Justice Department announced today. Dignity, formerly known as Catholic Healthcare West, is based in San Francisco and is one of the five largest hospital systems in the nation with 39 hospitals in three states.

Here is a more recent example

https://fronterasdesk.org/content/1680753/dignity-health-neurosurgical-associates-pay-10-million-billing-fraud-settlement

I don't know if they intended to overcharge (they are a not for profit).

Eight months ago I had a severe bacterial infection and had to go to the General Hospital in Yuma and had 12 hours of treatment and exams. I had to pay $ 105 and Medicare paid the rest.

The specialist set up a follow up exam at his private office which catered mostly to immigrants. I was informed that I would have to pay $ 200 up front. I explained that my co pay under my Medicare Advantage plan was $ 25 and they said that they needed the deposit and that they would then clear it with the insurance company and refund it back to me after they got approval. I knew that this was a lie that Medicare didn't require prior authorization for a simple office visit.

This was clearly fraud and obviously I didn't go there and I reported it to the fraud line for Medicare.

Again the fraud and/or over billing is being done by the health providers and the billing is going through the insurance companies because they handle the billing

3) It appears to me that you do some googling and find somethingthat sounds bad and assume that it is fraud because insurance companies are you know inherently evil

For example above you cite the OIG report that talks about non clinical reimbursements for $ 2.6 for non clinical HRA payments but you don't have any idea what these are and there is nothing in the citation indicating fraud. What they are is yet another free benefit for beneficiaries of Medicare Advantage aka as Medicare part C, a government paid for insurance.

It radically helped me AND didn't cost me a penny as my Medicare Advantage aka Medicare Part C is completely free

If you have Medicare Advantage you qualify for a doctor outside your health system to come to your house and give you a free consultation on managing your health care. So having a resource to a health care professional that is completely "unrelated to a clinical service" is not only not a bad thing but can significantly improve health outcomes, but is only available, without a copay and without any premium cost to members of Medical Advantage aka Medicare C

from your article

th

In-home HRAs generated 80 percent of these estimated payments. Most in-home

HRAs were conducted by companies that partner with or are hired by MAOs to

conduct these assessments—and therefore are not likely conducted by the

beneficiary’s own primary care provider

The whole point is to give the patient a resource to evaluate his primary care provider.

Costs the patient nothing with Medicare Advantage.

How good are these visits?

They are fucking fantastic. The doctor isn't there to bill anything, to charge anything but simply to help you evaluate your primary care provider.

I have had 3 of these and strongly recommend to anyone that they do it if called. The last one was able to confirm my suspicion that I was not getting the right care for my diabetes and I changed providers and my health improved 100% (which will also save the government money in the long term). The doctor was an exceptionally qualified doctor from Africa that was waiting for his US license to be completed so he could practice medicine but he could consult and he helped me a lot.

There was nothing in the article that indicated fraud but they did suggest changes in oversight.

Are there some insurance companies that do a better job than others than compliance issues? I am sure that is true.

I have to thank you for this link because

1) It does not indicate anything about insurance company fraud

but

2) It does articulate another benefit that Medicare C (aka Medicare Advantage) beneficiaries get for free that those with only A and B do not get: A home visit by a qualified doctor to help you evaluate whether or not you are getting top quality care by your medical provider. I wouldn't say that the home visit doctor saved my life but he helped me find a path to significantly improve my glucose control which is a pretty substantial morbidity factor for diabetics.

Every time I see a doctor I get an email from my health insurance company to ask about the quality of the service and where I can call to get questions answered. In the US it is impossible to call and talk to your doctor but you can get answers from a doctor that works for the insurance company. I am not sure if I didn't have the HRA that is only available for free through Medicare Advantage if my health would have not improved but since I have outlived my father by 12 years I have to consider that they HRA you have cited as a suspicious abuse by an insurance company could have saved my life.

Celerity

(55,412 posts)snip

One rip-off strategy insurers use is improperly denying claims. A recent investigation from the Department of Health and Human Services inspector general found that among Advantage companies, 13 percent of prior authorization denials were improper, along with 18 percent of payment claim denials—or about 85,000 requests and 1.5 million payments, just in 2019. Paying lots of claims adjusters to fake up reasons to deny necessary treatment is a big reason why Advantage companies spend nearly 14 percent of their money on administration, as compared to traditional Medicare’s 2 percent.

Another strategy is rigging the risk pool. Advantage companies are notorious for pushing doctors to “upcode” as many diagnoses onto their patients as possible, thus increasing their risk score and payment, without having to pay for more treatment. That tactic alone cost the government $9 billion in 2019.

All this (plus a bunch of other complicated scams) means that Advantage enrollees receive something like 10 to 25 percent less in health care spending, but the program costs the government about 3 percent more per person than traditional Medicare. This absurd situation is actually getting worse. One recent study found that Advantage plans cost the government $106 billion in overspending from 2010 to 2019, and nearly a third of that came in just the last two years. The price tag is predicted to balloon to $600 billion over the next nine years. One would think that the Biden administration would be looking to reverse course, but it isn’t. On the contrary, as Caress notes, it has so far proceeded with a Trump-era plan to privatize the remaining shreds of Medicare by letting private companies serve as payment middlemen through something the Trump team called “direct contracting.”

After an outcry from progressives, the administration altered the privatization plan, mainly changing the name (it’s now called ACO REACH), with the supposed goal of achieving “equitable outcomes.” But as Diane Archer explains at Social Security Works, at bottom it’s still the same idea, with a lot of obvious loopholes for quick profits by denying care, pushing more people into Advantage plans, gaming risk scores, and so on. Unless Biden changes his mind, America is going to let a bunch more foxes into the Medicare henhouse, including private equity firms, and half-heartedly try to limit the damage to the taxpayer with a bunch of ultra-complicated regulations of the type that are failing right before our eyes.

snip

I am glad your Medicare Advantage works for you, but on balance, the concept and its actual practices are terrible policy IMHO. Introducing the profit motive (which too often manifests itself in outrageous cases) as a fundamental bedrock for what is a basic human right is just something I do not, at my very core, agree with at all.

Btw, I have used the US healthcare system myself. I lived in LA for several years whilst I read for my MBA) and I had no issues with the care (I was listed on my father's employer's (a global financial firm) US health insurance for CA, Kaiser Permanente, so had no costs that I had to bear myself). I completely realise that my US situation was not that of a normal US adult as I was still on my parent's insurance. I also am far too young for Medicare. I also have US-based family and friends who have had horrid times with their healthcare, especially insurance and providers and the billing interlocks.

czarjak

(13,763 posts)We have a pediatrician in the family who says avoid Advantage. Period.

MichMan

(17,677 posts)czarjak

(13,763 posts)dembotoz

(16,922 posts)he was recruited by another network and this was the pigeon hole they had available

Response to Riverman100 (Reply #71)

czarjak This message was self-deleted by its author.

grantcart

(53,061 posts)(Although not a specialist in medicare I am a licensed insurance agent)

If the OP has any interest at all in providing accurate information as a PSA the OP will delete this OP.

Every statement I make will be backed up with a direct reference to a Medicare, .Gov source

To clear up some of the misunderstanding that is common here are the basics about A and B

Medicare A provides for hospital coverage for those eligible for Medicare @ 65 and there is no premium.

Medicare B provides for partial coverage of doctors and specialists fees. It has a monthly cost of $ 164.90 a month and you are automatically enrolled with A at 65

1) First of all Medicare advantage is Medicare Part C, not private insurance

https://www.medicare.gov/Pubs/pdf/12026-Understanding-Medicare-Advantage-Plans.pdf

Medicare Advantage (also known as“Part C”) is a type of Medicare health plan

offered by a private company that

contracts with Medicare. These plans include

Part A, Part B, and usually Part D. Plans may

offer some extra benefits that Original Medicare doesn’t cover.

Medicare Advantage is NOT privately funded insurance. Let me explain. The VAST VAST majority of Medicare Advantage clients choose a Medicare Advantage that has zero premium.

These plans are ADMINISTERED by private companies but the premium is PAID by Government.

Why was it set up this way? Medicare part C also known as Medicare Advantage has expanded benefits that involve more client management involvement than the simple reimbursement of A and B so it was decided to offer more Medicare benefit

but have it paid by the government.

Example: Medicare Advantage has a significant priority in incentivizing preventative health practices. For example they pay for basic gym membership (aka Silver Sneakers). My Medicare Advantage includes paid incentives if I do certain things:

Going to the gym $ 5 a month

Colonoscopy $ 40

Eye Exam $ 40

and so on

My wife gets additional incentive payments for

Breast exam

Bone Density

So not only does Medicare Advantage not cost me (and the vast majority) a dollar we actually get paid by the insurance company. Because of the detailed and individual nature of the benefits in Medicare Part C it was decided that it was better not to have a government agency administer it but to do it through private companies. All Medicare Advantage plans meet basic medicare requirements and are strictly controlled by medicare.

Some people choose to buy an Medicare Advantage Plan that has a monthly premium and offers additional coverage for prescriptions. For some people it is a big savings, for others it is an unnecessary expense.

The OP has it backwards, Medicare Part C are government paid plans (with some people paying for additional coverage).

Medigap helps pay for some office co pays but doesn't offer additional help on prescription drugs

https://www.medicare.gov/health-drug-plans/medigap/basics/how-medigap-works#:~:text=A%20Medigap%20policy%20is%20different,supplement%20to%20Original%20Medicare%20coverage.

A Medigap policy is different from a Medicare Advantage Plan (Part C). A Medicare Advantage Plan is another way to get your Medicare coverage besides Original Medicare. A Medigap policy is a supplement to Original Medicare coverage. When you’re getting started with Medicare, you can either buy Medigap or enroll in a Medicare Advantage Plan, but you can’t have both.

If you have a Medicare Advantage Plan, you can’t buy and don’t need a Medigap policy

To summarize:

Medicare Advantage is government paid insurance that is also known as Medicare C

Most people on Medicare C pay no premiums

You can actually get money back on most Medicare Advantage Plans

Medicare Advantage with no premium offers additional assistance on co pays and prescription drugs.

Medigap is paid by you, you pay the premium. The range for Medigap plans (aka Medicare part L, M and N)is between $ 59 and $ 310 a month. Again the average premium for Medicare Advantage is $ 0 for 70% of the recipients.

Seniors have 4 choices

1) Medicare A and B only

2) Number 1 plus a zero premium Medicare C

3) Number 1 plus a Medicare Advantage plan that has a premium and has additional prescription benefits

4) Number 1 plus a Medigap plan.

Which is best for you?

Even though I have been a licensed insurance agent for 20 years I could not answer that question and OPs like this one that prescribe one option is best for all are highly irresponsible. If I were an agent specializing in Medicare I would need a detailed list of prescriptions to input into the different plans to come to a conclusion.

What I can tell you is that there is no one who benefits most from option 1 (Medicare A and B only) because you can get (and most people do) a Medicare Advantage policy that has no premium but has additional benefits. Even though it is clearly preferable to get more benefits with no cost you will find DUers frequently post OPs discouraging people from getting Medicare Advantage even though it will cost them nothing.

What should you do to learn the actual facts and not be misled by someone who is completely uninformed about Medicare Advantage?

1) Read the links above which includes the official Medicare brochure that explains in detail what Medicare Advantage is.

2) Do not call the companies that advertise but find an independent medicare insurance agent that represents more than one company and ask for their recommendation. If they don't ask about your prescriptions, don't bother using them. If you are worried about finding the right one make an appointment with three different ones and pick the one that gives you the best plan.

3) Don't worry if you are not 100% happy with your Medicare Advantage. I am delighted with Humana but I know that they don't have many approved doctors in Yuma but have a ton in Tucson. If you are ever unhappy with your Medicare Advantage plan you can change in the next open season.

4) Don't get bummed out by all of the Medicare Advantage commercials. They advertise that way because the rules for client acquisition are very strict for Medicare part C. They can only respond to a query they cannot initiate the contact. I was in a Walmart once and stood next to an agent that had an approved table in the front. For three minutes I smiled at him and waited for him to say something. He smiled back but said nothing and I asked him if he could help me and invited me to sit down. He explained that he could not say anything to me until I made the first comment.

My experience with Medicare Advantage

I have Humana

My Medicare Advantage Premium is $ 0

My wife and I get about $ 200 every year back for participating in preventative incentive plans

I am an insulin dependent diabetic with diabetes, HBP and prostate meds and my total prescription cost is about $ 125 for three month refills.

Humana also provides very valuable guidance on health related issues. For example there is a severe doctor shortage in Tucson and after spending hours trying to find a doctor that would take an appointment before 2024 I called them up and had a doctor in 5 minutes. A call to get information about hearing aid options answered my questions in 15 minutes and it was better than the ENT doctors have been giving me for 20 years.

You wouldn't take medical or legal advice from a random poster on the internet so why would you take advice on Medicare insurance from a random poster with no links to government information on medicare. If you want to do it right find a Medicare agent that specializes in Medicare

I have been a licensed insurance agent for 20 years but don't specialize in Medicare and would not try to find the best solution without a licensed agent that specialized in it.

Silent Type

(12,412 posts)you want to go to traditional Medicare, you face underwriting. I think during first year, you can go back. But not sure.

Don’t believe MA is awful, unless one thinks the 45% who choose it are stupid. I don’t.

But people do need to understand networks, copays, etc. Clearly Advantage plans have an incentive to limit care. But it’s questionable whether it’s as capricious as some believe.

Gotta trust people know what’s best for them.

Some folks, like me, don’t care if I can choose any doctor. Fact is, for most of us almost any doc is adequate. Finding anyone better than adequate is really hard.

Bluepinky

(2,586 posts)Medicare Part C (also called Medicare Advantage, or MA) administers the senior subscriber’s medical benefits to which he/she is entitled to through Medicare. The private insurance company assigns a risk factor to the enrolled senior, and the federal government transfers money to that insurance company; the higher the subscriber’s risk factor, or the sicker the patient, the more money the government transfers to the insurance company. Instead of paying Medicare benefits for each individual person, the government pays the Medicare benefits to the private MA plan.

Some of the fraud instituted by the private insurance companies (MA plans) is that they assign a higher risk factor to the senior subscriber, so that on paper, the enrollee looks sicker than he/she actually is. Then, the federal government will issue more money for that subscriber to the MA plan, and that extra money is profit for that private insurance company.

Other ways the MA plan commits fraud is when they deny care to a subscriber, who would be entitled to that care under Medicare. The point is: MA is run by private insurance companies. The federal government does not oversee or manage them, so they can pretty much do what any private health insurance company does: deny care, adjust premiums and deductibles, and limit choices of doctor or hospital to maximize profits.

Hekate

(100,135 posts)Our great good fortune is that my husband is still employed at the age of 76 at work he loves, and is able to do it from home. We use the company’s insurance.

In the nature of things, this will not go on forever, and we will have to deal with Medicare.

The OP is alarming — but I noticed the lack of links and the very low post count. You, on the other hand, I know — and true to DU’s tradition of encouraging and even insisting on sources, you provided them. I will be giving your info the consideration it deserves.

Thank you & have a happy 4th of July.

(Copying your post into mine for ease of retrieval. )

❤️

(Although not a specialist in medicare I am a licensed insurance agent)

If the OP has any interest at all in providing accurate information as a PSA the OP will delete this OP.

Every statement I make will be backed up with a direct reference to a Medicare, .Gov source

To clear up some of the misunderstanding that is common here are the basics about A and B

Medicare A provides for hospital coverage for those eligible for Medicare @ 65 and there is no premium.

Medicare B provides for partial coverage of doctors and specialists fees. It has a monthly cost of $ 164.90 a month and you are automatically enrolled with A at 65

1) First of all Medicare advantage is Medicare Part C, not private insurance

https://www.medicare.gov/Pubs/pdf/12026-Understanding-Medicare-Advantage-Plans.pdf

Medicare Advantage (also known as“Part C”) is a type of Medicare health plan

offered by a private company that

contracts with Medicare. These plans include

Part A, Part B, and usually Part D. Plans may

offer some extra benefits that Original Medicare doesn’t cover.

Medicare Advantage is NOT privately funded insurance. Let me explain. The VAST VAST majority of Medicare Advantage clients choose a Medicare Advantage that has zero premium.

These plans are ADMINISTERED by private companies but the premium is PAID by Government.

Why was it set up this way? Medicare part C also known as Medicare Advantage has expanded benefits that involve more client management involvement than the simple reimbursement of A and B so it was decided to offer more Medicare benefit

but have it paid by the government.

Example: Medicare Advantage has a significant priority in incentivizing preventative health practices. For example they pay for basic gym membership (aka Silver Sneakers). My Medicare Advantage includes paid incentives if I do certain things:

Going to the gym $ 5 a month

Colonoscopy $ 40

Eye Exam $ 40

and so on

My wife gets additional incentive payments for

Breast exam

Bone Density

So not only does Medicare Advantage not cost me (and the vast majority) a dollar we actually get paid by the insurance company. Because of the detailed and individual nature of the benefits in Medicare Part C it was decided that it was better not to have a government agency administer it but to do it through private companies. All Medicare Advantage plans meet basic medicare requirements and are strictly controlled by medicare.

Some people choose to buy an Medicare Advantage Plan that has a monthly premium and offers additional coverage for prescriptions. For some people it is a big savings, for others it is an unnecessary expense.

The OP has it backwards, Medicare Part C are government paid plans (with some people paying for additional coverage).

Medigap helps pay for some office co pays but doesn't offer additional help on prescription drugs

https://www.medicare.gov/health-drug-plans/medigap/basics/how-medigap-works#:~:text=A%20Medigap%20policy%20is%20different,supplement%20to%20Original%20Medicare%20coverage.

A Medigap policy is different from a Medicare Advantage Plan (Part C). A Medicare Advantage Plan is another way to get your Medicare coverage besides Original Medicare. A Medigap policy is a supplement to Original Medicare coverage. When you’re getting started with Medicare, you can either buy Medigap or enroll in a Medicare Advantage Plan, but you can’t have both.

If you have a Medicare Advantage Plan, you can’t buy and don’t need a Medigap policy

To summarize:

Medicare Advantage is government paid insurance that is also known as Medicare C

Most people on Medicare C pay no premiums

You can actually get money back on most Medicare Advantage Plans

Medicare Advantage with no premium offers additional assistance on co pays and prescription drugs.

Medigap is paid by you, you pay the premium. The range for Medigap plans (aka Medicare part L, M and N)is between $ 59 and $ 310 a month. Again the average premium for Medicare Advantage is $ 0 for 70% of the recipients.

Seniors have 4 choices

1) Medicare A and B only

2) Number 1 plus a zero premium Medicare C

3) Number 1 plus a Medicare Advantage plan that has a premium and has additional prescription benefits

4) Number 1 plus a Medigap plan.

Which is best for you?

Even though I have been a licensed insurance agent for 20 years I could not answer that question and OPs like this one that prescribe one option is best for all are highly irresponsible. If I were an agent specializing in Medicare I would need a detailed list of prescriptions to input into the different plans to come to a conclusion.

What I can tell you is that there is no one who benefits most from option 1 (Medicare A and B only) because you can get (and most people do) a Medicare Advantage policy that has no premium but has additional benefits. Even though it is clearly preferable to get more benefits with no cost you will find DUers frequently post OPs discouraging people from getting Medicare Advantage even though it will cost them nothing.

What should you do to learn the actual facts and not be misled by someone who is completely uninformed about Medicare Advantage?

1) Read the links above which includes the official Medicare brochure that explains in detail what Medicare Advantage is.

2) Do not call the companies that advertise but find an independent medicare insurance agent that represents more than one company and ask for their recommendation. If they don't ask about your prescriptions, don't bother using them. If you are worried about finding the right one make an appointment with three different ones and pick the one that gives you the best plan.

3) Don't worry if you are not 100% happy with your Medicare Advantage. I am delighted with Humana but I know that they don't have many approved doctors in Yuma but have a ton in Tucson. If you are ever unhappy with your Medicare Advantage plan you can change in the next open season.

4) Don't get bummed out by all of the Medicare Advantage commercials. They advertise that way because the rules for client acquisition are very strict for Medicare part C. They can only respond to a query they cannot initiate the contact. I was in a Walmart once and stood next to an agent that had an approved table in the front. For three minutes I smiled at him and waited for him to say something. He smiled back but said nothing and I asked him if he could help me and invited me to sit down. He explained that he could not say anything to me until I made the first comment.

My experience with Medicare Advantage

I have Humana

My Medicare Advantage Premium is $ 0

My wife and I get about $ 200 every year back for participating in preventative incentive plans

I am an insulin dependent diabetic with diabetes, HBP and prostate meds and my total prescription cost is about $ 125 for three month refills.

Humana also provides very valuable guidance on health related issues. For example there is a severe doctor shortage in Tucson and after spending hours trying to find a doctor that would take an appointment before 2024 I called them up and had a doctor in 5 minutes. A call to get information about hearing aid options answered my questions in 15 minutes and it was better than the ENT doctors have been giving me for 20 years.

You wouldn't take medical or legal advice from a random poster on the internet so why would you take advice on Medicare insurance from a random poster with no links to government information on medicare. If you want to do it right find a Medicare agent that specializes in Medicare

I have been a licensed insurance agent for 20 years but don't specialize in Medicare and would not try to find the best solution without a licensed agent that specialized in it.

W_HAMILTON

(10,497 posts)Apparently she got roped in a Medicare Advantage plan a loooong time ago. She was paying pretty expensive monthly premiums, too, so I'm guessing the Medicare broker (or whatever they are called) that steered her into this plan did so just because they got a bigger kickback than if they put her on a no-monthly premium plan. The benefits weren't even that good, relatively speaking.

She had a stroke last year and I knew she was going to be needing better insurance, so I looked into switching her back to "traditional Medicare" and I was told that she would be denied (because of her age and preexisting conditions) or it would be so expensive I wouldn't be able to afford it, so, she was essentially stuck with Medicare Advantage. The same Medicare Advantage (Humana) that tried to kick her out of a rehab facility based on their AI projections of how long she should be there and -- surprise, surprise! -- regardless of her doctor's orders or updates, they tried to kick her out on the exact day they had originally projected two or three weeks prior, when she first entered.

I helped my sister navigate signing up for Medicare just last year after learning all of this and I encouraged her to get "traditional Medicare" plus a supplement, since it was her initial sign-up. I told her she could always switch over to Medicare Advantage if it got to be too expensive, but if she started out on Medicare Advantage, odds are she would never be able to switch back since they could deny you after that initial sign-up period where they cannot do so.

GoneOffShore

(18,038 posts)

Emile

(44,184 posts)

Joinfortmill

(21,965 posts)As an aside: I'm 74 and I've always used Medicare Advantage. It has always covered my medical needs and is quite affordable. And, I've had some issues, like brain aneurysm procedures that cost upwards of 200k. My total out of pocket cost was 365 dollars. Choose wisely. I've always chosen a national plan and found that Aetna is the best with Humana a close second. Best of luck everyone with whatever plan you choose.

DemBlue76

(78 posts)I would have thought you would hit your maximum pot-of-pocket, which is around $5,000 for MA plans here.

Joinfortmill

(21,965 posts)Vinca

(54,573 posts)bought into one of those super duper plans with gym memberships and other "frills." Last year I had a second hip replacement and all of my out-of-pocket costs amounted to about $2,000. My brother needs a knee replacement and I know he's delaying it because he's going to be on the hook for a larger deductible and more co-pays. Medicare Advantage is just big insurance with nice commercials.

BlueIdaho

(13,582 posts)May not be the best place to get financial or medical advice.

Emile

(44,184 posts)what Republicans introduced to do away with Medicare.

MichMan

(17,677 posts)I don't believe he did it to do away with Medicare, do you?

Emile

(44,184 posts)Republicans have long supported Medicare Advantage, dating back to the creation of the modern program in 2003 under President George W. Bush.

Signed into law in 1997