General Discussion

Related: Editorials & Other Articles, Issue Forums, Alliance Forums, Region ForumsBank CD rates...WTF?

I haven't looked in a few years and was surprised because it SEEMS to be saying that rates are like .4 percent or so (worse or better depending on time).

Am I remembering wrong that just a few years ago, you could get 3%, 4% or even 7%?

Thanks for the help.

ON EDIT: With the DOW at 15,000 for the first time in history, what the fuck is this? Don't banks have to try to compete with the stock market for investors?

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

northoftheborder

(7,639 posts).....5 years I think that they have been under 1%.

upaloopa

(11,417 posts)the banks nothing to borrow money so you are in competition with the Fed. Banks don't need depositors so they aren't going to pay a rate to attract them.

That's the way it looks to me. I could be wrong.

RobertEarl

(13,685 posts)When you can borrow from the Fed at near zero, why go anywhere else?

And the checking and savings are pretty much captive, because they are safe. As long as inflation on big ticket stuff stays low, no one notices the trickle up.

Yo_Mama

(8,303 posts)Actually, the Fed is inserting a lot of money into the economy each month. When you do this, banks don't need to pay interest for deposits:

Since lending isn't really growing, banks have nothing to do with the money, really:

It also has adverse effects on the economy - people who need to save have to save a lot more, because the saved money is shrinking in "real" terms, due to inflation being much higher than their investment returns.

And older retirees, pension funds and insurance companies are feeling the pinch.

BlueStreak

(8,377 posts)This is a bankster's dream. The idea behind the bailouts and the vast expansion in money supply was that banks would go out and lend money liberally to businesses and that would fuel a cycle of jobs.

How much longer do we have to follow these bullshit policies? Even Greenspan admits they were all a mistake. This does not work, especially when you add a dose of austerity.

What we know DOES work is programs that have to employ people -- such as infrastructure projects. It creates the demand side of the economy. All this money supply is the Reagan "supply side" stuff that never worked.

I would point out that the prime lending rate is 3.25% right now. And most businesses would have to pay a couple points above prime, so banks can theoretically borrow for practically zero and lend it out to businesses for 5% or more. But that just isn't happening in a big way. The big mistake in the bailout is that there were no provisions that compelled the banks to put money back into the economy by way of making business loans.

As your charts point out, the Fed has sent 3 trillion bucks floating out into the economy. And at best, this has generated maybe 1% of GDP growth, and reduced unemployment by 1/2% BFD. Most of the money has made its way into the pockets of hedge fund managers by way of the stock market, not generating any significant economic activity along the way. And let's compare that to the "stimulus" About half of the "stimulus" was tax cuts -- which aren't stimulative. Obama did that to buddy up to Republicans, but still he got basically no GOP support. So we should have had a real stimulus of $700 Bn, but actually got a stimulus of about $350 Bn, which is ONE-TENTH as much money as the Fed has recklessly pumped into the economy.

If we would instead have authorized just 1.5 trillion in infrastructure projects, we would be way under 6% unemployment now with a thriving economy and with a money supply that didn't threaten to kill us all with future inflation.

The whole thing has been totally reckless and irresponsible -- not defensible on any economic basis.

Bonobo

(29,257 posts)What is, instead of bailing out Fannie Mae and all them, we had made a massive number of govt. loans to homeowners but earmarked the money so that it could only be spent on mortgage payments and home improvements.

The money would have trickled UP to the banks, kept people in their homes and had a big impact on business like construction, building supplies, contractors, etc.

Everyone happy, no?

More trickling down... and millions lost their homes and banks gained so many falling apart homes that hey had to be bulldozed.

Without home repairs, improvements being made, how the hell can a 30 year old house appreciate in value anyway? It makes no logical sense.

mrmpa

(4,033 posts)home repairs needing to be made.

My Mortgage holder offers for $40 a month a protection plan, it covers

AC System, Furnace/heating system, electrical system, plumbing system and stoppages, faucets, toilets, water heater, ceiling fan, garbage disposal, garage door opener, refrigerator/ice maker/water dispenser, built in dishwasher, cook top, range, oven, range exhaust hood, built in trash compactor, built in microwave, clothes washer and dryer and accessible ductwork.

If I need a repair on any of these, the cost is $75 that is even if the system is replaced.

I purchased the plan, because my ac and furnace units are about 15 years old and probably will need replaced within the next 5 years, the cost of the plan that I will have spent is less than what a new system would cost.

I have all ready had two calls for repairs to my furnace. The cost of one repair if I did not have the protection plan would have been $641.86.

I think this is a smart program for the bank to offer, because it protects their investment. It is also good for the home owner, because it may be easier to find an extra $40 a month rather than $600 or more for a one time repair.

JDPriestly

(57,936 posts)on where you live. Land is more scarce than it was 30 years ago. At least it is in most cities. The land values have risen.

Bonobo

(29,257 posts)Land has value, but people buy the houses for the most part when they are shopping.

It costs a lot of money to tear down a house and rebuild.

Try selling a house for $250,000 that is broken down, beaten up and old looking.

abelenkpe

(9,933 posts)Torn down and a nice mcmansion taking up every square foot of the lot built overnight.

Yo_Mama

(8,303 posts)Oh, maybe we could have refinanced the loans for very low interest rates, which would have helped some homeowners, but when you owe $500,000 on a house worth $320,000, a low interest loan doesn't fix the situation.

That's why bubbles are so hugely destructive - it leaves people with stuff that should be assets but isn't because they owe far more debt in relation to the asset than the asset is worth. This is from publication Z.1 - homeowners' equity:

And mortgages outstanding:

And credit market debt outstanding:

Dropping interest rates very low didn't help all those who wound up so deeply underwater that they could never get out. And dropping interest rates low couldn't fuel home or office construction, because we had just been in a building frenzy and way overbuilt, and the home vacancy rate is STILL very high:

The government needed to find other ways of spending the money on something worthwhile so that the money could circulate through the economy, and that's impossible to do at those volumes. Homeowners had been pulling out close to a trillion dollars a year for spending on other things, and trying to replace that spending is effectively impossible. But there was also the loss of income involved with all of those employed in the construction industry, and then all the stuff they bought (like trucks).

And if the government had figured out how to spend a trillion and a half one year to replace that impetus in the economy, it would just have been another bubble, because the government can't keep doing that year after year. In fact we did run huge deficits and it did do something, but that too is not sustainable.

Keynesian theory actually doesn't have a cure for bubbles. There's always a period of consolidation and rebuilding. You can try to soften the blow, but that's all that's achievable.

Low interest rates help to soften the impact of business and personal debt

But they don't take the debt away, and shifting that debt to governments still doesn't take it away:

We have to pay for that through higher taxes.

The only way to get rid of debt is to write it off. However, once you get in a situation in which creditors are writing off trillions worth of debt, it blows up your financial system so that worthy borrowers can't get loans, which makes the situation worse. That is why the end of every bubble involves a financial system bailout, and the government accumulating more debt.

BlueStreak

(8,377 posts)If it were possible to slowly deflate the bubble over, say, a decade, then many people could cope with that.

But bubbles burst. Or maybe it is more accurate to say that we only talk about the bubbles that burst. The free market does self-correct in many cases. But these bubbles often involve extreme profiteering and distortions of the free market system. The mortgage bubble was absolutely such a case. I'm just happy the perpetrators are in jail so that won't happen again.

Oh, wait a minute ... It was Reagan who put 1000 perps in jail after the S&L fiasco. Obama has gone after how many?

It really hurts me to make that comparison, but as Democrats we should be intellectually honest.

Yo_Mama

(8,303 posts)Our government has become more and more a slave to big money.

When Corzine was not prosecuted, I mentally conceded that it was over. Even Ronald Reagan made GE pay taxes.

"Right of Reagan" is not my idea of a Democratic government, but that's where we are. Until the government stops being run from Wall Street, the average individual will keep getting poorer.

BlueStreak

(8,377 posts)I wouldn't say that Obama, by himself, is right of Reagan. But it is very hard to argue that our government today, regardless of where Obama's true heart may lie, is not FAR to the right of Reagan.

The only consolation is that we probably aren't far to the right of where Reagan would have gone if he could.

Yo_Mama

(8,303 posts)Our system is set up so that the government cannot be captured by one man. This is good, and people blaming Obama for everything are completely out of the ball park.

Yet with regard to many issues, the Democratic party has moved right of the Republicans in the 80s, and we need to fix that.

BlueStreak

(8,377 posts)Not just the SCOTUS, which has moved FAR, FAR right. There has been a huge effort by Republicans to load of all levels of the courts with extreme right-wing ideologues. Dems tend to nominate middle ground judges and the GOP almost always goes for the most radical ones they think they can get away with. That has had a huge effect in moving the country to the right.

lumberjack_jeff

(33,224 posts)Yo_Mama

(8,303 posts)what they're doing doesn't do much good for the economy.

It can only help a very few. Now admittedly, those very few are helped hugely, but the money is trapped in a very small circle of people.

Without actual spending IN the economy, the Fed's easy money policies just keep fueling bubbles. We are now in another one.

As for inflation, as soon as the economy improves enough so that net borrowing can build up, we will surely see rapid inflation. How can the Fed withdraw this much money quickly? It's impossible. They are not exactly going to sell a trillion and a half of bonds in a year.

So their alternative is purely to raise rates, and that is going to hurt the middle class very badly.

BlueStreak

(8,377 posts)Yo_Mama

(8,303 posts)Wall Street is happy, therefore we must all remain silent....

But Wall Street will not be happy for long.

BlueStreak

(8,377 posts)Certainly Facebook with a P/E ratio over 1700 looks like bubble mentality. But the market as a whole is not near an historically high P/E level. The issue is that, being a jobless recovery, and a system where corporations can pay virtually no tax, the Fortune 500 are enormously profitable right now. And the market reflects that.

This concentration of wealth is not sustainable. There must come a time whether it collapses under one of these scenarios:

1) the weight of systemic unfunded government (after all business used to pay about 30% of our tax revenue. Now they pay under 10%. If they paid even 20% there would be no deficit at all.)

2) The moneyed interests sending us on one too many military adventures.

3) riots in the streets as millions of long-term unemployed face a miserable existence.

4) the bankster crooks emboldened (after zero prosecutions) to run more major scams as they did leading up to 2008. That is surely underway already. Fish gotta swim. Bird gotta fly.It is what they do.

There will be some ups and downs in the market, but it seems to me one of the above scenarios is what will trigger a major collapse of our financial system.

Yo_Mama

(8,303 posts)You've got fake profits. Any economy that looks like this:

with this:

Is in a bubble. Apparent income is being created out of thin air, whereas real income is nearly stagnant:

This cannot be sustained.

BlueStreak

(8,377 posts)If anything the Net national product is tracking more or less to the market. I believe that last chart does not adjust to real dollars, so inflation is a big part of that slope. That is another part of the puzzle that nobody wants to talk about. There has been a lot of talk recently about chained CPI understating inflation. But forget that. The "regular old CPI index grossly understates the kind of inflation that most people see because it is so heavily biased by market basket goods that are subsidized (basic food product and oil).

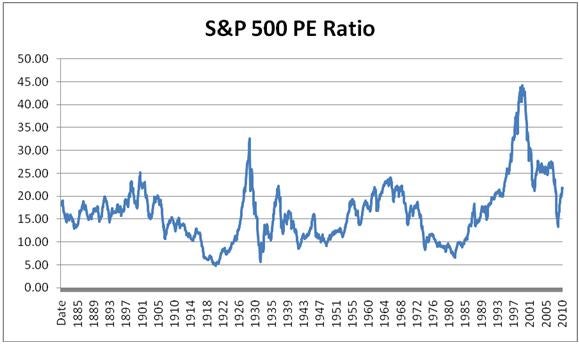

Here is a chart that tracks P/E ratio over the long haul.

The "normal" level seems to be about 18. Today it is 18.45. A year ago it was 2.50 lower.

http://online.wsj.com/mdc/public/page/2_3021-peyield.html

So I'd say we are starting to overheat, but it is still well within the historical range.

Yo_Mama

(8,303 posts)Not immediately, but as soon as the Fed has to correct, and it will have to correct within a few years unless the economy gets much worse in an underlying sense. If the economy were to get worse, then obviously future earnings would be impacted.

If the Fed corrects, then costs of debt are going to go way up. Corporate non-financial debt has continued its rise:

Right now that does not affect earnings, because the cost of servicing the debt is so low.

Once more, back to GD levels.

If this does not scream "BUBBLE" than I do not know what does:

Money is essentially free to a corporation with good reserves. But in the future, this will not continue if we continue in recovery. Corporate profits after tax have continued to rise

Look at the ratios there. If companies wind up paying significantly more on their debts, their after-tax profits will drop very significantly. Further, corporate taxes have to rise!

Corporate profits have risen about 25% from their pre-recession highs.

But after tax profits have risen much more relatively! (over 40%)

Another way to check this is that corporate net cash flow has ceased its stratospheric rise:

The implications of low national factor income versus high profit income are that the situation is unsustainable, or that an ever-increasing amount of profit must come from overseas. When I look around the world, I see that that isn't going to continue either. Europe's slide may halt, but growth in exports from Asia to Europe is not going to be remotely like it has been. Because circulating income in the US for most people is harshly constrained, exports from Asia to the US are not going to provide the type of injections into Asia that have been the case.

You only have to check out the sales of brands like Yum in Asia to see that the real situation over there is much worse then thought. Indonesia and Malaysia and Thailand may stay up, but they are not enough to carry the loss of growth and potential growth in India and China. Nominal drops in revenue like this can mean only one thing:

http://articles.marketwatch.com/2013-04-23/industries/38757853_1_yum-brands-inc-first-quarter-profit-after-hours-trade

Any real rise in interest rates alone would cause earnings to drop significantly. Corporate tax rates have to rise.

Attempts at stimulus have set up a situation in which corporate earnings appear acutely sensitive to interest rates. One can either postulate a Japanese future in which real demand for money never increases, but I cannot believe this due to our trade imbalance and our demographics, both of which are extremely variant from Japan's, or one can count on future inflation and attempts to control it by raising interest rates.

However if you assume that interest rates don't rise, then the pressure on corporate profits will come mainly from rising effective tax rates, and that is manageable.

To summarize: During the recession product sales fell hard, both domestically and globally. As the recession eased, trade and sales rebounded and that provided the first big goose to corporate profits. After that big surge, corporate profit growth was sustained by low effective corporate tax rates plus constantly falling effective interest rates. Effective interest rates have reached their lows. Trade gains are there, but slow. Corporate taxes are going to rise effectively even with no law changes, because many of the companies are still using built-up loss credits.

BlueStreak

(8,377 posts)As I see it, this is the perfect scenario for the biggest corporations (lousy for the small businesses that do most of the real hiring.)

They have the cheapest labor costs in years. That comes from a combination of people willing to take any job at half their prior pay just to have some food on the table. It also comes from being able to work people like dogs with no repercussions. Productivity is at an all time high, but we need to understand that high productivity essentially converges with slave labor. We are part of the way there already. And they have been able to kill unions and labor laws left and right. There has never been a better labor situation for big business. For them an 8% unemployment rate is just about optimal -- at least as far as maximizing profits.

They also benefit from the lowest taxes ever. Again this is a benefit that mostly goes only to the really big companies that can afford to set up offshore havens and use all the other tax tricks they have paid lobbyists to set up for them. Small businesses -- the good guys -- aren't getting much of that benefit. Their taxes aren't historically high, but as the biggest corporations have excluded themselves from paying ANYTHING, all the rest of us are facing higher taxes and fees everywhere we look.

So this is pretty much the dream situation for big businesses: the cheapest labor possible without going offshore, and no taxes. Any movement from here will move them off that optimal profit point. Ironically, further recover is bad for the biggest businesses.

We need legislators who understand how to get rid of perverse incentives that reward people and companies for doing all the worst things for the nation at large.

Yo_Mama

(8,303 posts)Basically, the large companies are sustaining profits while undercutting the base.

However from a purely econ-stat perspective, it is easy to see what is happening. From NIPA table 1.8.6, we can see that the peak for real command basis net domestic product peaked at 11,579 in Q3 2007. In Q-1 2013 (5 and 1/2 years later) it had only slightly exceeded that high at 11,837. Yet corporate profits are going sky-high on essentially the same revenue base.

This won't continue. From Table 7.1 we see that real per capita disposable income (income less taxes) peaked in Q1 2008 at 33,826 and in Q1 2013 (5 years later) stands at 32,640. This is not going to end up well! The quarter before, which still incorporated the FICA payroll tax cut and was boosted by pre-tax increase extra dividends and bonus payments was at 33,138, still well off the peak.

You cannot have a situation in which real aggregate per capita income keeps dropping and corporate profits keep going up. It does not work. It leads to deflation in one way or another.

One clue as to what is happening is that companies are missing revenue estimates even as they are exceeding profit estimates.

It is very obvious that the per-dollar feed-through gain from the Fed's money-throwing is dropping. Will they ratchet it up to 100 billion a month? I agree that CPI is a joke, but even that is now dropping, which points to the difficulty of averting disinflation with dropping real purchasing power among the majority of households.

There is only one sure effect of the Fed's actions - it increases income inequality:

Countries with high Gini ratios have unstable social environments and tend to have poor long term economic stability and unstable currencies.

Well, wtf, wholesale inventories/sales ratio is back to 1.21 in March, which generally sparks a correction. It's kind of obvious that that this would happen, given lower real disposable incomes:

http://www2.census.gov/wholesale/pdf/mwts/currentwhl.pdf

And we are at the danger line there - last year when it came close to 1.20 we had the manufacturing slowdown, as purchases needed to clear. So we are set for another summer of SLOW, which I do not think is going to do much for US incomes. The US consumer frog is in slowly heating water.

napi21

(45,806 posts)accts and the few interest bearing checking accts. that exist. .1 is actually higher than some..

Bonobo

(29,257 posts)WTF?

Don't banks need to compete with those interested in investing in the market!?

If CD rates can't compete with even healthy levels of inflation, aren't we all just fucked and burning our money while banks speculate in the real game, the big money game (with the promise of being bailed out if they fuck up???)

Jesus H. Christ.

In the 80's you could get a CD for 12%. Even in the early 2000's, it was 7%. Fuh-huck!

onenote

(46,226 posts)See the connection?

Interest paid on CDs, etc. almost always is less than the interest payable when one borrows. So as excited as you might have been to get 12 percent on a CD, keep in mind someone else was borrowing that money at 13 percent or more.

Bonobo

(29,257 posts)Savings should be rewarded marginally more than borrowing

Borrowing should be discouraged marginally more than saving.

onenote

(46,226 posts)To pay you more for depositing your money with me than I could charge someone for borrowing that money from me.

Bonobo

(29,257 posts)Thank you for the lesson.

JDPriestly

(57,936 posts)so great. Think about the lending rates on credit cards and other personal loans. They are pretty high compared to the rates banks pay depositors. It's a scandal.

Watch the Elizabeth Warren speech in Congress about student loan rates. The banks are getting by with murder. And no one is investing in industry and job creation in the US. Our policies toward banks and the Fed are hurting Main Street and ordinary working people.

Yo_Mama

(8,303 posts)They can't lend it out. There is no demand for this much money. In fact, the problem is so bad that some banks have charged large depositors a fee for taking their money occasionally during this "recovery".

http://online.wsj.com/article/SB10001424053111903366504576488123965468018.html

It's not just us, either. Last year Swiss banks were charging fees for cash deposits:

http://www.zacks.com/stock/news/87942/swiss-banks-to-charge-for-deposits

US banks are leaving large sums on deposit at 25 basis points at the Fed (1/4 of 1 percent), which is how you get .1% interest. The rest is in servicing costs (it costs banks money to maintain accounts, and it costs banks money to pay FDIC insurance on deposit accounts).

This is the situation the Fed has created, and it has created a strong deflationary impetus. When savings returns are so low, it pays people to pay down their mortgages and other loans, so the average individual is trying to pay down loans. Mortgage refi cash-ins are at astoundingly high rates.

And if you want to buy a house, saving money for a 10% downpayment has a much higher real return than anything you could spend the money on that's stable. If you don't have to go FHA, you save 135 bps (1.35%) on insurance.

Individuals and businesses are acting quite rationally in the situation, but it means that the economy is always hovering around deflation and would be deflating if it were not for the Fed hurling trillions of money into the economy, which drives up basic commodities and stocks.

When your outstanding loans are doing this:

And your money supply at banks is expanding rapidly:

Banks cannot afford to pay much at all for deposits, because they can earn almost nothing OFF those deposits. Nor can they afford to buy long term investment instruments, because when interest rates go up, they would lose their shirts. Velocity plummets:

When short term rates for Treasuries are effectively below inflation, there is nothing banks can do with each extra deposit dollar but leave it on deposit at the Fed for that 25 basis points:

Note that we are back to Great Depression levels!!!

Six month is no better:

One year is still pushing ZIRP:

All of that creates this:

JDPriestly

(57,936 posts)imports it allows to flow in almost without check.

We cannot afford to produce a sufficient quantity of anything that can compete with cheap, foreign imports.

The way to pick up our economy is to place import taxes on goods from low-wage countries.

That offends the free-trade, right-wing folks, but if we continue with our present trade policies, we will be forced to watch our economy go even more deeply into recession, lower our wages, reduce our standard of living and stand by while the dollar drops . . . .

We have to tax imports. I cannot see how we can become a productive country unless we defend our borders, our industry and our jobs from the goods flooding us from low-income, sub-standard-of-living countries.

Employing people in Bangladesh is a great idea. But the way we are doing it is killing them and weakening us. Who is it helping? The few rich investors who own the factories in Bangladeah (and similar third world countries) and those who tag along and invest smaller amounts in those irresponsible corporations controlled by the rich. Face it. We would not permit Americans to work in the conditions that people work in in third-world countries.

The worst of it is that when our economy has succumbed to the on-going devaluation of our labor, our assets, our minds, our creativity, when we have become a country of lazy, fat boors, we will not be able to sustain even a shadow of our democratic institutions and will be subject to whatever dictator comes along.

We must stop this free-trade mania. If you have a lake of pure, mountain water and you allow immense quantities of contaminated water from a factory to flood into it, all of the water in the lake becomes at first less drinkable and finally poisonous.

I do not favor putting the brakes on free trade for any racial reason. It just makes no sense because it is destroying our domestic industry, our domestic markets, our domestic employment outlook and the dollar. Thanks to the cheap goods from other countries, there is no demand for American industrial production -- or at least not nearly enough to pull us out of a recession and make our money useful.

So, stop the free trade. That is my view.

I have yet to see an argument that refutes my point of view. People argue in favor of free trade, but they do not confront or discuss the impact of unfettered imports on our domestic industry, job market or ultimately, in the future, on our dollar.

Right now, we have horrible trade deficits that never end.

Yo_Mama

(8,303 posts)The Fed is hugely driving up the money supply in order to inflate the stock market. Banks have way more money than they could possibly lend out. They get very little return on the money so the savers get very little return.

CoffeeCat

(24,411 posts)...another bubble? Furthermore, as the FED increases the money supply and the stock market surges---is this real and sustainable gains that will hold over time?

I don't see how fake augmentation is ever good, because it's not based on true economic growth. I see another crash. Am I seeing things?

Just trying to learn and ask question. Thanks for any thoughts or insight that anyone may have.

Munificence

(493 posts)BS smoke and mirrors. It's amazing how many folks do not understand that the FED's $85 Billion + month in quantitative easing is putting out the perception that the stock market it doing good. It's all about perception!

The low interest rates by the banks (corodinated with the government and fed) and the beat down in the precious metals market is the governments, The FED, and mainly JP Morgans grand scheme to get everyone in either real estate investments or into the stock market.

If folks do not understand this, then they should become informed and educate themselves. I visit a lot of sites across this world wide web and I would say that this site has the least talk about QE and the ramifications.

$85 Billion a month in "stimulus" from the FED, all to devalue our dollar and keep our interest payments on our debt in check. I will say that this is the only thing going. But is a huge tax on all of us in the form of devaluing the dollar.

There is a big time war going on over the major players in the world, it is called "currency devaluation".

I said it on here a few weeks ago and will say it again:

There is no difference between The Fed, The Gov and JPM - they are doing all of this. The Gov calls JP Morgan "Too big to prosecute" cause there are one in the same, you can not prosecute anyone for wrong doing there as you will have to go after the government also.

Oh and Japan announced their new QE....think ours is bad go check theirs out!

We are beyond the point of return across the world, it is all going to fail. I will say that it all was supposed to crash and burn 4 years ago....the only way to delay it was to fire up the printing presses. We have delayed it, but it is coming.

riderinthestorm

(23,272 posts)Scary times...

BlueStreak

(8,377 posts)In our fractional system, they banks need to have some deposits, then they are free to load many times as much money as they actually have in deposits (that's the fraction). So ultimately they need some deposits. They make their money by getting most of the loan amount from the Fed at a discounted rate (and that rate now is virtually zero).

Historically the formula might have gone something like this. Jerry, the 3rd shift line supervisor buys a $5000 CD at his local bank. He earns 4%. The bank takes that $5000 and combines it with $45,000 of Fed play money that the bank gets for 2%. So the bank is paying about 2.2% for that $50,000 stash. Then bank loans the full $50,000 to a business and charges them 7.5%. So they are effectively making a 5 point spread on that interest rate. They take the risk that the loan will not be repaid, but of course they charge a much higher rate to their riskier customers, so basically they never lose at this game unless they do crazy stuff like what they did with those mortgage derivatives.

The reason CD rates are so low now is that banks just don't need the deposits because businesses aren't borrowing. And businesses aren't borrowing much because the high unemployment rate has created a situation where they have driven their labor costs way down, and many of these businesses are making record profits (see the Dow 15,000). And these profits generate enough loose cash flow that they just don't need to borrow. And businesses that want to fund a major expansion will either float more stock or sell some bonds, either of which is cheaper than getting a bank loan in most cases.

Historic NY

(40,123 posts)

snappyturtle

(14,656 posts)BlueStreak

(8,377 posts)Tbills are only slightly higher, and none of them (not even the "inflation protected" bonds) even keep up with what I believe is the ACTUAL inflation rate, just based on my own observations.

GNMA funds pay a little better.

Corporate bond funds pay 4-8% and are thought to have low risk, but wait ... It turns out they are all highly leveraged, which doubles or triples the tradition risk -- plus you have the big gorilla: interest rate risk. See below.

Public utilities are pretty low risk, and many of them pay a 4% dividend, plus there can be some capital appreciation. Traditionally the big utilities have very steady prices, but that can be changing as we move more into the world of alternate energy sources. They may not be as as safe as they once were. But I still think these are pretty good bets. Look at SO, WGL, and ED for starters.

INTEREST RATE RISK -- BEWARE !!!!!

A lot of us think there is a very high probability that all this money flooding the economy will ultimately end up in a big inflation cycle. The only thing forestalling that now, IMHO, is the stranglehold businesses have on wages, but that will break if we get down to 6% unemployment. And then, watch out. All hell could break loose. Before investing in any interest-bearing (or dividend-driven) instrument, please understand what inflation does to those investments. If you are holding a 20-year corporate bond, for example, that pays 4%, when inflation goes up, the value of your bond will drop like a rock. Same thing for funds, dividend stocks and anything else that focuses on yield. So don't get greedy. There are funds with average maturities of 3-4 years. For me, that's a reasonably safe bet .

abelenkpe

(9,933 posts)CDs even better. Then the market crashed. Haven't seen anything over one percent for CDs or savings. That's what is especially cruel about discussions on cuts to ss or raising the age of eligibility for medicare. How can anyone even save to prepare for a future of further cuts (if they are lucky enough to have work) in a world that makes saving so difficult.

Bonobo

(29,257 posts)When? How the fuck did we allow this? This crime?

Lemme get this straight...

1. Dumb losers like me act conservatively in saving money in bank. Banks pay .4% or less even for a CD...

2. Banks invest in a stock market where they will try to get 10% or more return annually (sorta making up rough numbers here) in a historically high stock market.

3. If banks fail at #2 above spectacularly, they will be bailed out by dummy in #1

4. Dummy than says, "Oh, honey I guess we need to invest in stock market just to keep up with inflation".

5. Dummy loses money in stock market and is fucked.

RagAss

(13,832 posts)And nobody uttered a fucking peep while it was all going down.

Yo_Mama

(8,303 posts)They may lend to entities that do, but they can't buy stocks directly. Net Interest Margin is a measure of what banks are making on their investments after credit expenses:

The Fed is deliberately doing this.

Bonobo

(29,257 posts)

CountAllVotes

(22,240 posts)You have it nailed.

Are you going to do it is the question?

I'm in the same boat more or less, and no I am not going to do "it".

You might check out American Express online savings acct. -- pays .85 - better than .4 locked in!

Luckily I bought some I-bonds 12 years ago and they are paying 4.79% right now; will reset to 4.20% in October, 2013. They are saving my "portfolio" (or I should say "my arse" so to speak.

so to speak.

>>5. Dummy loses money in stock market and is fucked.

The plan exactly, grab up what is left and lose it all.

It is a total joke and I know it! It is not difficult to figure out. Too many without and too many with nothing. NOTHING at all ...

JDPriestly

(57,936 posts)Wall Street calls it market-making. I call it fraud.

abelenkpe

(9,933 posts)Unless they were lucky enough to have a wealthy family or know the ins and outs of the market...

Fla_Democrat

(2,623 posts)Rates are falling for all types of mortgages, and the average 15-year fixed loan has hit an all-time low of 2.56%, according to Freddie Mac.

Meanwhile, 30-year fixed-rate loans, at 3.35%, are within 0.04 percentage points of their all-time low last fall.

Banks will not borrow money from depositors (CD's, MMDA's) for more than they are making from people borrowing from them. Who would pay 7% for money to loan at 3.35%? Throws the spread way out of wack.

Bonobo

(29,257 posts)So in order to help the housing market recover, things were manipulated to lower mortgage interest rates and that put the slam on bank saving rates?

Something like that?

Fla_Democrat

(2,623 posts)and see the when, and could draw from that the why.

I just know the is. As long as the cost of borrowing money from a bank is low, the cost of the bank borrowing from the customer is lower. And, I think we can all agree that interest is the cost of borrowing money, regardless of who is paying it.

Warren Stupidity

(48,181 posts)rates have been kept artificially low for most of the last ten years, and massively so for the last five.

CoffeeCat

(24,411 posts)It costs a good chunk to refinance your mortgage and so many people have done it within the last several years. I think most people I know, who own a home, have refinanced since interest rates have fallen.

These same banks made a killing during the housing boom, and after it went bust in 2008, banks weren't lending. People were scared to make big purchases and banks weren't lending as they had in the past.

These low interest rates have been quite a boom for these banks.

defacto7

(14,162 posts)of negative interest rates. Figure that one out. Sorry, no link.

CoffeeCat

(24,411 posts)There was a lot of chatter about CDs and what a bad investment they are, because of these drastically low interest rates. This kind of talk went on, in various forms.

Maria B was discussing retirement and how to save enough, how to invest, etc. The issue of CDs came up and every talking head dismissed outright this option.

Every talking head and guest on CNBC steers people toward the stock market...PERIOD. They practically scoffed at other options, including CDs. Of course, they are right--rates are horrendously low.

And right now, the stock market seems healthy because of record DOW numbers, with the DOW hitting 15,000+.

There is a great deal of push right now, to get into the market--or to continue to invest in it. I really have no idea what is driving these highs. Is it the FED? Is the economy improving? Many in the middle class and lower middle classes are sinking farther, which would seem to stave off a healthy recovery. The Baltic Dry Index is anemic--and is always a solid indicator of economic growth, stagnation or retraction.

I find the economy and the stock market these days to be one big mystery. However, there is no shortage of pundits who are strongly encouraging everyone to invest those 401k dollars and other monies into the markets.

Puzzling.

JDPriestly

(57,936 posts)It's boom and bust over and over and over. And there is not real investment in industry in this country. In my view investing overseas can be unpredictably risky. Foreign government can simply nationalize property if they wish.

The investment climate today is a nasty squeeze on the middle class. We need to rein in the predator Wall Street barons.

Blue_Tires

(57,596 posts)dkf

(37,305 posts)Warren Buffet says he doesn't like bonds because interest rates are artificial. That is purely the Fed at work.

JDPriestly

(57,936 posts)19th century well before the Fed was instituted.

Big business loves the boom and bust cycle. Very wealthy people buy assets during the busts and sell at the peak of the booms. That's how they enrich themselves.

And the rest of us suffer.

Commodore Vanderbilt, Jay Gould, the lot of them were profiteers (and losers) in the cycles of their time.

The Fed is just the modern tool of these kinds of "market-makers."

It is the game of unscrupulous charlatans.

dkf

(37,305 posts)The housing bubble, even the tech bubble, and now the bond bubble.

In the past those were regular market cycles. Today they are aided and abetted by the Fed.

Silver Swan

(1,118 posts)I would be a millionaire now. As it is, by frugal living I'm breaking even. I thought my retirement would be better than this.

still_one

(98,883 posts)CountAllVotes

(22,240 posts)I know, I have some of those too ...

They'll reset again on Nov. 1st, 2013.

Will likely hang on to them for awhile -- better than the .85 online savings acct. w/American Express!

Luckily I hung on to the old I-bonds with the 3% bottom line on them. *whew*

And to think, the Treasury tried to convince me to trade them in for EE bonds which I've never much cared for.

*sigh*

Whatta mess.

still_one

(98,883 posts)CountAllVotes

(22,240 posts)That was after a bout of DEFLATION (and YES this did happen!). They reset at 2.+% and then to 1.75%; soon to be 1.18%. You must hold them for 1 year before you can cash these however (with a 3 mo. penalty btw; after 5 years -- no penalty). Right now they are better than anything else but you must buy them electronically now, no more as no more physical bonds are being issued. Gee, I wonder why that is?

The 3% ones I'm holding they shall not "get" them any time soon as you can hold them for up to 30-years, tax-deferred AND State tax EXEMPT, and YES, these will be the last things to go that I still have managed to hang-on to.

still_one

(98,883 posts)

TexasPaganDem

(42 posts)When I first started in banking 17 years ago, we still had clients with CDs at 12-14% Annual Percentage Yield for a 10 year term. That rate is now 1% APY. Most savings accounts are at 0.01% APY, and a tier money market will run from 0.10% to 0.25% APY depending on which bank and what deposit level (typically balances of $50,000 or greater are required for the highest tier).

I remember the slow march to zero, and crossover in 2009 when CD rates were no longer keeping up with inflation. At that point, the drive became conservative funds (mostly bonds, because people didn't trust the stock market, even though there was a 40% growth that year), because in a savings account, your money was losing purchasing power. CDs lost purchasing power, just slower than savings accounts.

dkf

(37,305 posts)Can you imagine the interest expense on $16 trillion if short term rates were close to 3-4%?

Low rates do so many things beyond rebuilding bank balance sheets.

Yupster

(14,308 posts)If I owed $ 16 trillion, I'd want 0 % interest rates too.

Also, interest on cd's is taxable.

How much tax money is the government losing by having cd's at .2 %.

But the government is trapped. They can't raise rates because they owe $ 16 trillion.

What's 3 % interest cost of $ 16 trillion? Oh, just $ 480 billion per year.

President Obama, do you have an extra $ 480 billion? No? How about you Speaker Boehner? No?

Then we better keep the interest rates at 0 %.

They're trapped.

reformist2

(9,841 posts)lumberjack_jeff

(33,224 posts)Interest rates will never be better.

JDPriestly

(57,936 posts)The banks get there money for almost nothing. They charge pretty high interest and then pay depositors even less than they pay for their money.

Art_from_Ark

(27,247 posts)Of course, here in Japan the rate has been close to zero for more than a decade. I recently saw a bank advertisement in Tokyo Station offering CD rates of 0.4% for long-term CDs-- meaning it would take 250 years to double one's money at those rates (assuming no compounding of interest).

I also recently talked to a couple of guys from the UK who told me that bank rates for savers in their country were also near zero.

Bonobo

(29,257 posts)of 1 or 2%, where the hell does that leave us?

Unless wages go up..jeez. Screwed.

Art_from_Ark

(27,247 posts)And there's really no place to park savings for the average saver that will provide any kind of return. My last interest payment that the bank credited to my account (6 months interest) wasn't even enough to buy a can of soda from a drink machine.

byeya

(2,842 posts)afraid of deflation because there's no tested cure for it and it - deflation - feeds on itself. Central bankers know how to treat inflation that gets to high for comfort.

Japan has not seen the growth they want since their stock market burst 20+ years ago and the governments have been trying to bring back prosperity ever since. 1--2% is considered a positive from an historical standpoint.

Art_from_Ark

(27,247 posts)Japan actually is, overall, a prosperous country, although admittedly there are some places like Muroran that have seen better days.

The economic problems in Japan stem from a variety of factors, not the least of which has been having to cope with a currency that had fluctuated wildly in value vis-a-vis the US dollar and which is currently valued 2.6X higher against the dollar than it was when the Plaza Accord was put into effect back in 1985. It would be tough for any exporting country to deal with that.

Also, Japan has a very saturated economy. It is hard to grow domestically when everyone already seems to have enough stuff to fill their living quarters with. The last major purchase* I have made, for example, was a car that I bought, used, 7 years ago.

*"Major purchase" to me means anything costing over 25,000 yen, or about $250.

Le Taz Hot

(22,271 posts)My 91-year-old Great Aunt and I were discussing this a few days ago and she said her life savings grew significantly in, I think it was the 1990's (or possibly 80's?) in which she was able to lock in a 13% interest rate on, I believe it was a CD. Anyway, she she said doubled her money in about 7 years. Imagine being able to do that today.

CountAllVotes

(22,240 posts)I remember when rates to buy a car were at 20% in the late 1970s.

No new car for me, that much I could guarantee!

Yavin4

(37,182 posts)The Fed cannot keep interest rates at 0% unless there's high unemployment. Otherwise, we'd be up to our necks in hyper-inflation.

rusty fender

(3,428 posts)Will it be this summer, or will it burst in October, a month it has often burst in

truebrit71

(20,805 posts)...it's coming...I'm just not sure what the catalyst is yet...the housing bubble was fairly easy to see coming, this next "correction" though could be caused by any manner of things...I don't' think we'll see a 2008-type bloodbath this year, but maybe this time next year would be more ripe for it..I think there's enough pent-up demand for higher returns to drive the markets substantially higher, especially if the trillions in bonds starts to rotate out, but that will eventually collapse under it's own weight...

So, nothing this year (maybe) but next year, if things continue on the same path this year, will be ripe for a major correction...

Of course this could be complete and utter bullshit and the markets could shit the bed tomorrow if (insert random global fiasco here) occurs, but keep on putting your money into the markets with your 401(k) until it does, yes?

cbdo2007

(9,213 posts)We'll probably see a pretty big correction late this summer, but otherwise the Stock Market is definitely where you want your money over the next 2 years or so.

Response to Bonobo (Original post)

Name removed Message auto-removed

CountAllVotes

(22,240 posts)I remember this time you mention quite well.

The old passbook savings acct. always paid 5%!

Then came the IRA idea in the early 1980s telling people to invest in an IRA and you'd get 10% interest on it and you'd be a millionaire when you retire.

Well, as you know, that did not quite happen.

The reality of it all is that the trickle down never tricked down, at least to the working class and the poor.

Welcome to the Democratic Underground btw!!

brooklynite

(96,882 posts)The purpose of banks is to have funds on hand to back up loans, mortgages, etc. If you're being restrictive in your lending practices, and if the Federal Reserve will loan money at near-zero rates, you don't need to be competitive in the private market.

That being said, you're recollection is faulty. Rates haven't been higher than 3% since 2008, and higher than 1% since 2010.

pansypoo53219

(23,159 posts)we have an uneven economy. the interest rates need to go up. fear of inflation is a canard

dawg

(10,777 posts)At .4%, someone with a million dollars in the bank could hope to earn $4000 a year. Back when CD rates were 7%, that would have been $70,000. There is a big difference between $70K and $4K.

Of course, someone with that much money could just spend down some of their principal. But most people with nest eggs that size are retirees, and when it's gone, it's gone. I know they are fortunate to have been able to save that much money, but it's still very scary to retirees, especially if they are still relatively young.

Response to dawg (Reply #83)

Name removed Message auto-removed

llmart

(17,725 posts)I have a decent amount saved in an IRA and could draw on it if I needed money, but I'm almost 64 and what if I live to be 94? That's 30 more years and there's a good possibility there'll be health problems that cost money. So I don't want to even think about touching my IRA yet even though it would make daily life a bit easier. To a younger person the amount in my IRA probably sounds like a lot of money, but when the possibility of ever making any money again is next to none, well, that IRA money has got to last.

Warren DeMontague

(80,708 posts)Because that's the only non-Keynesian response to an economic slowdown that they've got in the toolbox.

hugo_from_TN

(1,069 posts)That's where I keep as much cash as possible.