General Discussion

Related: Editorials & Other Articles, Issue Forums, Alliance Forums, Region Forumstrying to figure out where I'm going to get the money for my obamacare

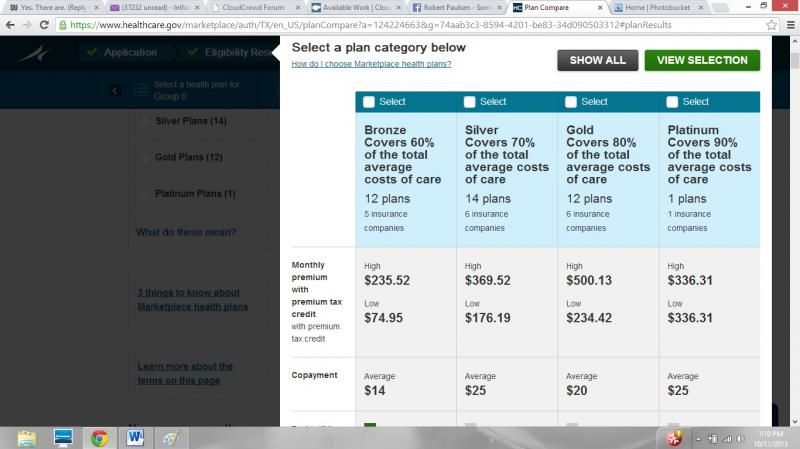

bronze = approx 214 per month, 6000 deductible

platinum = 500 or so per month, 1000 deductible

0 tax credit, no subsidy.

starting to feel like an ATM here, all my funds are pretty much spoken for.

plus, with a 6000 deductible, this would be insurance I couldn't actually use.

am i missing something here?

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

B Calm

(28,762 posts)datasuspect

(26,591 posts)uninsured/self pay.

i was lucky enough to find a clinic that charges 40 per visit, the Dr.'s cousin runs the in house pharmacy so i get my meds for about 20 bucks a month. affordable.

a lot less than 200 - 500 per month.

plus, i only see this doctor once every 3 months.

sure, i can't go get the tests she recommends, but it looks like unless i need more than 6000 in treatment, i'm shit out of luck on obamacare too.

frustrating. but i really do think (hope) i am missing something here.

Motown_Johnny

(22,308 posts)datasuspect

(26,591 posts)require a 6000 deductible for a bronze plan.

1000 for a platinum plan that costs upwards of 500 per month.

jeff47

(26,549 posts)is not subject to the deductible and immediately covered.

FarCenter

(19,429 posts)jeff47

(26,549 posts)4 out-of-pocket doctor visits would equal your $50/mo.

Most of the tests on the list would run over $600 out-of-pocket.

FarCenter

(19,429 posts)If a person occasionally sees a doctor for some complaint, the doctor usually does an examination as part of the sick visit.

The tests are valuable only if you have some reason for getting them done. And many of the most common ones like blood pressure or cholesterol are available cheaply at non doctor offices.

jeff47

(26,549 posts)You'll find that you will "get the chance" to receive most of these tests as you get older.

(Assuming you bother to see a doctor regularly at that point.)

VanillaRhapsody

(21,115 posts)FarCenter

(19,429 posts)Eat less junk, eat more good foods, exercise, stop smoking, stop drinking, stop doing drugs, stop reckless behaviors, etc.

None of which are at all likely to result from consulting with a doctor.

VanillaRhapsody

(21,115 posts)now covered under Obamacares....

You notice that countries with better healthcare have fewer overweight people? Why do you think that is....preventative care. In the future there will be incentives to encourage you to break habits...AND doctors will be rewarded for improving the health of the patients in their care..

all in due time...young person....all in due time.

FarCenter

(19,429 posts)Food expenditures as a percentage of household income are very low in the US -- ~7%.

In France they spend about 13% on food.

http://www.economist.com/blogs/graphicdetail/2013/03/daily-chart-5

http://wsm.wsu.edu/researcher/WSMaug11_billions.pdf

VanillaRhapsody

(21,115 posts)junk food is cheaper yeah....the process junk WE call food is cheaper...But real whole foods are not.

FarCenter

(19,429 posts)Most of Europe eats preserved fruits and vegetables during the winter. They don't have Florida, Texas and California to supply them.

The company cafeterias I've eaten at in Europe had poorer selections than US ones. And they were generally more expensive.

VanillaRhapsody

(21,115 posts)freshness is questionable...you know we import more than we export now right?

FarCenter

(19,429 posts)But they can't afford nearly as much as the US.

VanillaRhapsody

(21,115 posts)They also aren't burdened by healthcare costs...so...there's that. AND they use it...imagine that. They are not thinner because food is scarcer...that is ridiculous!

Motown_Johnny

(22,308 posts)Then take $45.00 a month off that $214.00 since you are getting something worth that much and the OP states that tests are needed. Now we are at 169. Then assume that this person has car insurance and that the rates will drop with health insurance. Where will that put us? Around 150 maybe?

As you said in another post, someone healthy would not be seeing a doctor 4 times a year. I am doing something similar to have blood drawn so that my prescriptions can be adjusted. If we assume this is also the case for the poster who started this, we then have lower cost prescription drugs since they will be covered in all ACA plans. Also, you get one visit to a doctor a year with no copay, that drops us to ~110. It is also very likely that the other three visits will cost less than the $40.00 being paid now. These visits could even be to a doctor with a private practice instead of a low cost clinic (which is intended for low income persons).

What does that $214.00 look like now?

Duckhunter935

(16,974 posts)Motown_Johnny

(22,308 posts)It means you don't pay anything out of pocket for it. It has nothing to do with your deductible.

For example, if you are over 50 you can get a colonoscopy without a copay. You don't pay. Zero dollars. No money out of pocket. Zilch, nada, how else can I say it?

You also get one wellness visit a year with no copay. So you would not need to shell out that 40 bucks like you do now. You could even go to a doctor with a private practice instead of that clinic.

Women get mammograms to help detect breast cancer without a copay.

No copay means no out of pocket costs. As long as you have insurance you pay nothing.

Nine

(1,741 posts)datasuspect

(26,591 posts)it's what i was able to hustle to fit within my budget.

LWolf

(46,179 posts)you are still out that deductible, and then the copays.

You're screwed either way.

Motown_Johnny

(22,308 posts)whatever is "speaking" for all your funds needs to stfu

.

HereSince1628

(36,063 posts)The zero tax credit speaks as much to low income as it does earning too much to get a credit

While some states are trying to negotiate other options, the reality is many states chose not to expand medicaid on either ideological (it's a socialist handout) or on some financial argument (not a fully paid mandate).

Consequently for millions of people, the promise of assistance meeting the mandate is a hollow promise. As great as the ACA may turn out to be, it does bite many of the people it was intended to serve.

Orangepeel

(13,981 posts)Someone in that situation now won't get help, which sucks, but they won't be forced to buy a plan.

HereSince1628

(36,063 posts)In the information chaos that exists, it's the best way.

My understanding is the person must still pay the penalty which rises to many hundreds of dollars per year by year 3.

Orangepeel

(13,981 posts)Those Left Out Of Medicaid Expansion Won’t Have To Buy Insurance

http://www.cms.gov/Newsroom/MediaReleaseDatabase/Fact-Sheets/2013-Fact-Sheets-Items/2013-06-26.html

HereSince1628

(36,063 posts)I'm happy to know I misunderstood.

LukeFL

(594 posts)Future ref

datasuspect

(26,591 posts)they come first.

then rent.

then the student loan people.

then the irs.

so yeah, 39k - 60k actually doesn't make you a millionaire.

ScreamingMeemie

(68,918 posts)I am in Texas.

I make between $40-45k

With a child and the subsidy, I can get the Silver Plan for 176.15/month.

You might want to use that phone number because that's a bit high if you have kids.

datasuspect

(26,591 posts)and the bronze plan monthly amount isn't necessarily burdensome.

it's the deductible that seems way out of whack.

i don't mind paying for something that I can use.

but if i have to pay out of pocket AND pay every month for that privilege, where is the value in that? where is the healthcare in that?

but i will have to put a call in.

ScreamingMeemie

(68,918 posts)For me, it was about getting in the door to actually see a doctor (the ones around here demand payment up front). Deductibles, for higher things like hospitalization are billed--not up front--so I can deal with that later.

I hope you get the right answers.

datasuspect

(26,591 posts)but if something is billed, it has to be paid.

so no, it's not a good deal.

ScreamingMeemie

(68,918 posts)it's the first time I've actually believed I'll live to see him grow up.

Good luck data. Let me know if you find anything out.

datasuspect

(26,591 posts)it feels like i live in a house of cards.

the only thing i know is that i have to go to work and sometimes this is the only thing that keeps me going.

thank you for being kind. I actually am trying to wrap my head around this thing, it's just that it's one more thing i have to do now. i'm stretched thin as it is.

i just pray that if i get sick, it's a massive heart attack and i just die on the spot.

moriah

(8,312 posts)It may be $25-50 or so more a month, but in general, that's what most people use. Their doctor, and their pharmacy. It's nice to have ER visits on a copay as well.

If you're able to find a plan with the *main* things you use covered and with a set copay that isn't dependent on meeting your deductible, then you could get some use out of the plan. I was on Advair and had a plan with a $2000 deductible, but prescriptions weren't part of that, nor were my primary care visits. $120 to see my doctor +$300 for just one of my medications, and I'd be better off to pay $300 a month for insurance, $25 copay for doc, and $50 copay for Advair.

But not everyone uses as much health care as I do.

jeff47

(26,549 posts)moriah

(8,312 posts)Sorry for the long link, but it works when I post it into a different browser, so I hope it works here...

https://secure.arkansasbluecross.com/lookingforinsurance/individualandfamilies/2014/detail.aspx?variantId=00&productId=75293AR031-0001&premium=216.90#/detail.aspx?variantId=00&productId=75293AR031-0001&premium=216.90

--------

A lot of people are looking at the lowest priced plans -- like this one, which is designed to be combined with an HSA. It has preventative care covered with no deductible, but everything else only is covered after the deductible is met.

jeff47

(26,549 posts)At least, in the non-HMO world. And these aren't HMOs.

moriah

(8,312 posts)Then says preventative care is covered 100% (referring to an annual physical, gynecological checkups, prostate checks, cancer screenings, etc). Yes, all plans on the Exchange will cover that 100%. Not all of them will allow a copay to be paid for seeing your primary care physician for a problem and getting medication. But some do, and if that's all you end up needing all year, you might not touch your deductible. That's what I was trying to express to the poster, that it might not hurt for them to see if they could find a plan like that.

There is a difference, and that's the difference I was referring to. I thought it was pretty clear in my post. I really don't know why everyone is determined to pick apart everything someone says to try to help someone else on here.

jeff47

(26,549 posts)Post after post on DU is people spewing false crap about the most basic elements of health insurance in order to damage the ACA.

A portion of them are right-wing trolls, and a disturbingly large number are people who think destroying the ACA will make single-payer magically appear.

As you mention, the exact details get complex, which makes a simple yet complete answer impossible. But for the vast majority of people, their doctor's visits will be labeled "preventative care" and thus not engage the deductible.

robinlynne

(15,481 posts)ZRT2209

(1,357 posts)

davekriss

(5,446 posts)but you do realize the $6000 out of pocket is the maximum in aggregate while the bronze plan is paying 60% of the bills?

That sucks (60%), but it's better than zero. And, of course, after you hit that $6000 threshold by paying 40% of your bills, the insurance picks up 100%.

So here's how it would work. Let's say you fall off a ladder and break a leg. Presume your deductible is $1000 (I know you told us, but I'm already at the window where I 'm typing this in and can't see your OP). The bill for the pins and cast and painkillers comes to $3500.

You would pay the $1000 deductible plus 40% of the remaining $2500, or $2000. For your $241 a month you save $1500 so far.

Later you get an ear infection and need to go to the doctor. They charge $100 for the visit and $10 for the antibiotic. You've met your deductible so you only pay $44. You save $66. $1,566 so far.

Six months later you get rear-ended at a stop sign. The other car zooms away and there are no witnesses. You desperately need a spinal fusion in your neck. Surgery costs $80,000. You pay $4,934 total, your insurance pays $75,066. You've saved $76,632 so far.

You decide to spend the rest of the year in bed under the covers in a fetal position so you don't have to spend any more on healthcare. Then you get the flu...

It's INSURANCE - chances are, especially if you're young, you'll pay more in premiums than for care. But if you are one of the unlucky ones (and these number quite a lot), you'll get the care you need because the providers know it is paid for. It is a SOCIAL thing, in aggregate we benefit while there will be individual cases where, ignoring the risks for themselves, claim they're getting a raw deal, they think "why should I have to pay for the healthcare of others?!"

It's funny how the latter anti-social belief disappears in a poof when that individual needs help. Perhaps it's a car accident, or cancer, heart attack, diabetes, gun shot wounds, rhuematoid arthritis, depression, and on and on with the things that plague us. Just sayin', not accusing you of holding that belief (in fact I think you're just reporting out your circumstances), but things happen, and the problem is we don't know at the start whether or not these things will happen to us. By sharing the costs (spreading them across pools of people), you and I are able to receive expensive care if needed.

(Of course, I advocate for single payer, but I don't always get what I want.)

pnwmom

(110,305 posts)Have you ever priced out a colonoscopy, for example?

aroach

(213 posts)I still support the ACA but we won't qualify for any subsidies even with a disabled child and income below 40K. Why? Because my husband's employer pays a large percentage of HIS premium. They don't pay anything toward me and the kids but the ACA only cares about the portion of the premium that is for his insurance. We have high deductible and high co-insurance. We haven't used our insurance at all this year because of it. So we pay hundreds of dollars a month for insurance that we can't use. I was hoping the ACA would change that but it looks like we are shit out of luck until they change the policy of only looking at the employees portion of the premium instead of the entire family premium to determine the 9.5%

PoliticAverse

(26,366 posts)in the near future.

stevenleser

(32,886 posts)Or is that not going to get you the subsidy?

snooper2

(30,151 posts)

DebJ

(7,699 posts)

regnaD kciN

(27,676 posts)A family and an income of $39K - $60K, and no subsidy???

Please -- my family has a higher income than that, and we have only one dependent child (meaning we're the smallest possibility for a "family" under the ACA) and we still qualify for over $400/month in subsidies. Either you haven't done the math correctly, or you've mis-reasearched your situation, or you're simply making this up.

Motown_Johnny

(22,308 posts)I helped mine out for a while too.

Family might not mean wife and kids.

Motown_Johnny

(22,308 posts)and I didn't say your family should stfu. I said WHATever was speaking for your money, playing off your "spoken for" comment. It may have been a bit harsh but I stand by it.

If you are bringing home over $3300 a month ( my estimate of 40K / 12 ) then 214 isn't a big deal.

This isn't even the real cost since there are benefits to it. If you have auto insurance, that will cost less if you also have some health insurance. Your $40.00 quarterly visits would cost less and one a year should be no copay (see my other post). If you are taking prescriptions and you go in every 3 months to have dosages adjusted (just a guess) then your drugs will cost less also.

Then there is the possibility that you do really have a medical condition that you don't know about. I honestly hope you are well and wish you all the best, but face it. Some percentage of people who are uninsured must have conditions that they don't know about.

What happens to your family then?

I sure hope this family does not include uninsured children. If so, then you really need to do the responsible thing and get some insurance.

Skittles

(172,223 posts)hand it over

Mojorabbit

(16,020 posts)perhaps with mortgage, student loans, etc. I am really getting tired of people here judging other's when they have no idea of another person's financial arrangements. The ACA is going to be awesome for some people(like my husband) and it is going to suck for others esp with the family glitch for those getting insurance from their employers.

Yo_Mama

(8,303 posts)It's just that he already has health care needs for which he is paying out of pocket, and now he's going to still be paying out of pocket PLUS paying the premium, and that has him worried, especially if something really bad happens, because then he's going to be out the premium plus the $6,500 deductible.

He needs more medical treatment than he is getting, but this plan isn't going to get him that either, because of the high deductible. For the lower deductible he has to pay more than he can afford a month.

In most rural areas, if you have non-emergency testing needs and a deductible like this, they are going to make you pay most of the cost in cash up front. Okay? So if this guy needs, say, a CT of the coronary arteries or a nuclear stress test, he's not going to get it because he can't afford it. Now if he doesn't get it and then does have a major heart attack, this plan will pay out for him for the very expensive followup care, but it's the intermediate care he's not going to get.

For some people, this is really going to cut their health care costs. For others, it will increase them.

I don't think we should be mocking people who are facing these choices.

datasuspect

(26,591 posts)they wanted to do testing that would have probably caught her uterine cancer in advance, only problem? she didn't have the 2k or so to pay for the test up front.

Yo_Mama

(8,303 posts)And unfortunately it will still happen under ACA.

There are many tragic cases and we are still failing to confront that reality.

Response to Motown_Johnny (Reply #3)

Post removed

jonsiee

(28 posts)Motown_Johnny

(22,308 posts)This is a huge problem with the system (single payer would solve it.. but that is besides the point).

This person can easily afford some basic insurance but chooses not to. Then when something happens (which is inevitable given the number of people who do this) the rest of us get stuck when they decide it is easier to declare bankruptcy than to pay their medical bills.

If this person is making over $40,000 a year in taxable income then the take home is most likely over $3,300 a month (this is just an estimate). $214.00 is not a very big chunk.

This isn't even an accurate accounting of the cost because of the benefits of having health insurance. If the poster has auto insurance, having health insurance will drop the rates. If this person has some reason to go to the doctor every 4 months then having coverage could very easily drop the out of pocket costs even more. If there are prescription drugs involved (and the quarterly checkups are to draw blood and adjust doses.. again just another guess) then the benefits are even greater.

The idea that someone can bring home well over 3 grand a month and still be so irresponsible as to have no health insurance what so ever is disgusting.

Also, please note that I said WHATever is speaking for the money needed to stfu. Not WHOever. I was playing off the phrase "spoken for".

Maybe it was an overstatement, but to me the OP was disgusting.. and still is.

The truth is I make roughly half that amount of money and pay nearly that much out of pocket for my insurance. I can swing it. It isn't reasonable that this person can't make that payment.

hooverville29

(163 posts)It's almost like he's just paying for a catastrophic care policy

Blue Idaho

(5,500 posts)There are many tests and services that do not require you to satisfy your deductible first.

jeff47

(26,549 posts)Response to Motown_Johnny (Reply #3)

Post removed

TorchTheWitch

(11,065 posts)When I made $36K 12 years ago I could barely make ends meet. Single, no kids, one dog, owned my dilapidated old car so had no car payments or anything more than liability car insurance (of course it was also breaking down all the time and nickel and diming me, but still far cheaper than a newer better car), rent was half of what I pay today for a bigger nicer place in a decent neighborhood than the dump I live in now that's smaller and in a shitty neighborhood, food was at least half of what I pay today, and gas was a fraction. No way would have I have a dime extra for insurance I couldn't afford to use much less be able to save anything for the tens of thousands of dollars I needed to fix my teeth (which is why I have full dentures now) nor could I save a dime for the future and that was 12 years ago.

$40K now is peanuts where I live and would get you a nice cardboard box to live in.

Motown_Johnny

(22,308 posts)I noticed that you did not say you couldn't afford health insurance back when you could barely make ends meet.

Besides, if you think insurance is expensive, try not being insured.

IMO, your point is not valid.

TorchTheWitch

(11,065 posts)And sorry, but back then when I got a shitty HMO policy that was worthless there's no possible way I could have spit out $214 a month on premiums for insurance I wouldn't have been able to use. Oh, and back then I had no computer, no cell phone, nor any of the technology so necessary today either but that also takes a big bite out of the expenses.

You think I LIKE living in an area where $40k for a single person doesn't mean shit? Of course you think my experience is invalid though... with 75% or more of Americans living paycheck to paycheck of course you'll believe that $214 a month for insurance that one can't afford to use is chump change. Pffftttt... all so you can try and claim this ACA piece of corporate for profit mandatory shit is fabulous stuff. Lucky you that lives in a world where $214 is chump change. It sure as fuck isn't for us working poor Americans who are the vast majority.

Motown_Johnny

(22,308 posts)But 40K to me is out of reach. I make around half of that and I pay nearly that much every month for health care (If you include Aflac). The world I live in is Detroit's East Side.

$214 is more than I have to live on this paycheck. It isn't chump change to me, it is two weeks worth of food, gasoline and other essentials.

I am a working poor American. I cut my other costs so that I can afford healthcare. It is simply being responsible.

If your taxable income is over 40K a year then you can afford $2568 a year for health care. You may not want to afford it but you can. It is ~6% of that 40K. Sales tax in many places (including where I live) is 6%.

It is affordable and no amount of whining will change that.

mmonk

(52,589 posts)datasuspect

(26,591 posts)6000 deductible means it is practically useless.

if a test or procedure costs 3500, i just can't shit out that amount all at once until the "healthcare" kicks in.

if i am understanding this wrong, someone please disabuse me of my error.

mmonk

(52,589 posts)So you see, it depends on one's position I suppose.

datasuspect

(26,591 posts)you are very fortunate indeed.

if it is causing you hardship, i apologize for being presumptuous.

i wish you the best of luck.

mmonk

(52,589 posts)And yes, it has been causing hardship.

haele

(15,481 posts)And I know what it means to live paycheck to paycheck, even now that the family income is between $50K and $60K, which should be good; I'm the only worker in a family of four, with a disabled spouse (Laz, a long-time DU'er) on SSDI.

Stick with me a bit here, because I have to explain what we have going on before I tell you what we have done that we can fix the costs overage issues.

Without insurance, Laz's annual medical costs are around $90K between doctor's visits, lab-work, and medication. Medicare D does not cover two of his critical medications; which includes a biologic injectable at $35K a year (retail) that keeps his joints from further degeneration and allows him to walk with a cane for 500ft or so at a time. My employer's insurance won't cover me and the kids with the PPO and sell me a supplemental for Laz that would cover his meds, so we can't see the savings he would get using Medicare.

Previously to this year, with insurance, Laz's usual out of pocket medical costs run around $8K - and that's what it was when our insurance had a deductible of $5K up to last year, which meant after that, all we had to pay was the minimum co-pays of $10 per doctor's visit and $5/$15/$35 monthly tier costs for each of his medications...

The kidlet has chronic stress issues landing her in Urgent Care and the ER several times a year, which usually costs us $3K a year.

At the beginning of the year, insurance was a cluster-fuck with a $9K deductible, and the introduction of "co-insurance" because my employer changed the way the plan was structured; they paid less and "we were more responsible for our health"...which is a savings to the average family if there is not a disability or unplanned medical emergency involved. And Laz ended up in the ER and then hospitalized for two days with bronchial pneumonia this summer.

So, this year, we already paid most of a total of $12K after the insurance got through with bills out of pocket. That's even after the $9K deductible; right now, we still have to pay for medications, 10% of specialists visits, and Urgent Care/ER/Hospitalization costs.

Because we know we will end up with a minimum of $9K out of pocket, I decided years ago to try and minimize the risk of bankruptcy and credit problems by enrolling in the company medical FSA plan that maxed out at $7200 a year.

Last year, my employer added an $5300 HSA plan and kicked in $1K to the HSA at the beginning of the year (but dropped the FSA to $2500).

This sort of plan easier for us to pay out of pocket medical bills by spreading the cost out by $160 a paycheck (I'm including the $140 a paycheck tax reduction due to a lower "gross income" ), and it also lowers our taxable income for federal, local, and state by $7800 a year.

(especially the FSA, which is more like a $2500 no-interest federal medical loan on Jan.1 that you pay off in pre-tax installments)

I do pay $300 a paycheck, there are offestting tax savings, and it's something I can budget as an installment plan. As the HSA rolls over to next year if I don't use all of it, and collects about .75% interest annually, if for some reason I don't use it all over the year, I can modify my deduction and have more money in pocket, or I can continue saving it for when I retire and need long-term care.

This has enabled us to not worry too much about that money, except for what we didn't have as the HSA was catching up to the bi-weekly payments. So what has worked for us this year to cover pre-deductible and "co-insurance/co-pay" costs what can't be covered by the HSA and FSA:

1) KEEP ALL YOUR MEDICAL RECEIPTS! Your out of pocket medical bills (including transportation estimates from house to doctor's office for visits) are tax deductible once the amount over the HSA/FSA or any other medical tax-exempt disbursement that exceeds 10% of your adjusted gross income. Some items such as pressure braces or hose for chronic conditions, walkers, medical canes are also tax deductible; anything with an FX or RX notation next to it on the receipt when you get it at a drug store or medical supply store can be used.

2 If you need to plan for expensive medical issues, get an HSA (through the insurance company or through your employer) and an FSA if you expect significant dental or optical. Plan your FSA payments for all expected Dental and Optical. This year, we had a lot of dental, and three of us have glasses, so we are maxed out.

If you know there's a strong possibility or certainty you will exceed your HSA, use the HSA primarily for initial co-pays and medication up front, and pay little costs (lab work, shots, procedures) so long as you don't exceed your per-paycheck payments.

It hurt during the beginning of the year, because our HSA only advances by $220 a paycheck, and Laz's out of pocket pre-deductible that first month was $2,200. We found that we need to keep one paycheck's funds in the HSA, to cover emergency visits or medications.

3) Negotiate with the billing offices to small monthly payments per month, and keep the receipts and payment records. Little lab or procedure bills of under $50 can usually be paid out the HSA before they get past 60 days, but big bills (like that $300 UTI diagnosis procedure) can be negotiated to a $15 to $25 a month payment. Hospitals and labs have to take a payment, no matter how small, and so long as you are paying, it doesn't affect your credit rating. (BTW, we have 11 payments a month of $15 - $25, and will pay off the payment once it gets under $100 if we have the cushion in the HSA)

As of now, we have $2275 outstanding in medical bills that we are slowly paying down by installments, and crossing fingers for no more to be added. There is $420 currently in the HSA (with $1120 left to be put in this year), ~$200 left on the FSA (kidlet has a crown put on next month that this will cover), so if nothing else happens, we should have $700 in the HSA at the end of the year.

Now, If my company is going to be kicking in another $1K next Jan 1 for the HSA, we will pay off four or five of those outstanding medical bills, and be able to roll paying those into next year, giving us more about a hundred more dollars during the month to spend on smaller necessary things - like going to thrift or consignment stores to replace four-year-old office clothes that don't really fit anymore, or getting new underwear.

4) See suggestion 1 - At tax time, I will gather up the 2013 out of pocket/not covered by HSA or FSA billing, and if it is over $5K, I will submit those to the IRS as part of my tax return. It might not get me back all of my out of pocket expenses, but it will get me back some - enough, at least, to pay off the rest of our medical bills.

So long as there is not a single payer system, this is probably the best strategy one can come up with to keep medical costs to a minimum when one has a chronic medical condition in a "high medical deductible" world

Haele

steve2470

(37,481 posts)KG

(28,797 posts)datasuspect

(26,591 posts)and thought i was being diligent by putting in the work, working my way up a little bit and trying to create something from nothing so I could generate revenue for a company.

don't eat at restaurants, not big on material possessions.

but the government gets more than 1/3 of my monthly income before I can even get my check.

gas fluctuates from between 3.50 - to 5.00 in my area, and NOTHING is getting cheaper.

i just expect for me and my family members to live decently, to have the basic necessities and no one goes without.

the point is, i'm not fucking rich.

i'm lower middle class for chrissakes.

so yeah, i could probably shit out an additional 200 a month, but not for insurance with a 6000 deductible. that means the insurance is practically unusable.

SammyWinstonJack

(44,316 posts)Probably more people in that situation than not. And then suddenly being forced to buy something one cannot afford because the money isn't in the budget....what's so hard to understand about that?

And it's getting pretty damn infuriating too. What was that asinine post this morning? Let's see your income and where you're spending your money. Fuck that.

Sedona

(3,872 posts)Are you using your gross or adjusted gross income to figure your subsidy?

enlightenment

(8,830 posts)and I'd like to point out that it is not the adjusted gross income.

It is the MODIFIED adjusted gross income, which is potentially higher than the adjusted gross:

http://www.zanebenefits.com/blog/bid/256075/Health-Care-Reform-Adjusted-Gross-Income-VS-Modified-AGI

Once you have adjusted gross income, you "modify" it to calculate your MAGI.

Specifically, Modified Adjusted Gross Income (MAGI) is calculated by adding back certain items to your Adjusted Gross Income including:

Deductions for IRA contributions.

Deductions for student loan interest or tuition.

Excluded foreign income.

Interest from EE(employee) savings bonds used to pay higher education expenses.

Employer-paid adoption expenses.

For most people, MAGI is the same as AGI.

For the OP - his MAGI will probably be higher than his AGI, because he is paying student loans.

BlueCheese

(2,522 posts)What's next? Revised Modified Adjusted Gross Income?

enlightenment

(8,830 posts)Give them time.

ejpoeta

(8,933 posts)$500/mo for 2 people with $3500 deductible. Then they only paid a certain percentage after that. I understand it sucks, but it is what it is.

datasuspect

(26,591 posts)but when it looks like a scam, smells like a scam, and costs like a scam. it's a scam.

ejpoeta

(8,933 posts)for us until we reached our deductible. which we never reached except the year I was pregnant. I understand the anger. I would rather have at least a public option, but preferably single payer. At least it is something.

displacedtexan

(15,696 posts)Now I understand.

Habibi

(3,605 posts)You've only listed bronze and platinum.

Le Taz Hot

(22,271 posts)I know the party-before-everything crowd doesn't want to hear but MILLIONS of us are asking the same questions. Mine would be about $500.00 a month providing my husband doesn't get his promised raise (now 2 months overdue). I don't HAVE $500.00 a month. My doctor charges $60.00 per visit and I go only when I can't find a home remedy (I often times can find one). I did have to go to the Dr. Monday as I self-diagnosed a sinus infection and needed antibiotics. I joined Walgreen's prescription savings plan about 3 years ago and it has saved me a mint. I'm also part of their loyalty club (or whatever it's called) and my prescription, which would have been $14.99, was $5.00 and because I had spent x-amount of money at Walgreens I had a $5.00 credit which means the whole episode cost me $60.00 for the doctor visit. That I can afford.

Puzzledtraveller

(5,937 posts)SammyWinstonJack

(44,316 posts)He had to wait two yrs to get on Medicare.

Every yr. he falls into the donut hole for his scripts, in April and we can't afford to purchase his two scripts for the remainder of the yr. and yet I am suppose to purchase health care insurance or pay a fine?

Yeah, no thanks.

If I could afford to purchase a plan, we'd buy his meds first.

Myrina

(12,296 posts)

Brigid

(17,621 posts)This state had not expanded Medicaid , and the AG has even filed a lawsuit trying to block subsidies. I may just sell my condo and move.I'm getting hosed, but not by Obama.

PasadenaTrudy

(3,998 posts)by the terminology. If I go with a Platinum plan, it says "Calendar year medical deductible" is $0. Then it says " Calendar year out of pocket maximum' is $4,000. I'm just on my first cup of joe so maybe I'm not seeing things straight, lol

karynnj

(61,035 posts)Deductible is the amount that you have to have spent before the plan pays anything on the items that say "after the deductible is paid". The Maximum out of pocket caps what you have to pay for the sum of anything you paid out of pocket - including the deductible, copays or any thing where you paid a share of the cost. One way of looking at this is that no matter what catastrophic medical needs you encounter, this is the most you would have to pay for the year. (Fortunately, the vast number of us do not come near to this in most or even all years. It should not be interpreted as the likely out of pocket cost -- unless you know you are someone with extreme medical needs.)

TheKentuckian

(26,314 posts)When it is met you are in the coverage phase and pay a percentage up to the out of pocket maximum at which the plan typically covers 100%.

In this situation, you would just pay 10% up to 4k and then you are fully covered (other than the premiums) because there is no deductible. I've heard a person or two claim that premiums apply to the accumulators but I've yet to see any support for that so I assume that is false.

Lex

(34,108 posts)If you haven't met your deductible amount yet?

hooverville29

(163 posts)Lex

(34,108 posts)You pay only a portion, like a co-pay, for doctor visits. So you don't really have to worry about the deductible unless it's a catastrophic event.

jeff47

(26,549 posts)Most plans would require you pay a small co-pay. Something like $25-50.

Other plans cover part of costs, up to the deductible. Let's say it's an 80/20 plan before the deductible (you pay 80%), and a 20/80 plan after (you pay 20%). I'm picking those numbers for convenience, I don't think such a plan can be found.

You'd pay 80% of the cost, until that 80% adds up to the deductible. Then you'd pay 20%. Until all the money you have spent hits the out-of-pocket maximum.

TheKentuckian

(26,314 posts)With some plans you will pay 100% of the negotiated rates up to the deductible.

Some plans the deductible applies to the out of pocket, other plans they accumulate separately.

Generally, care beyond those visits with structured copays on the better plans still require the deductible be reached.

I see plans with drug "coverage" where you would always pay 100% of the negotiated rate and the benefit is getting the negotiated rate.

I've seen horrible plans with 10k deductibles, 50% coverage, and another 15k to the OOP. One time I came across similar coverage with a 25k OOP.

Even higher earners cannot actually afford care, especially ongoing care and end up gobbling up charitable funds to actually get treatments because all folks tend to focus on is premiums.

Sorry, there is no one answer. Plan structures vary wildly not just by carrier but by group as well. Almost all current individual policies are complete garbage (in my opinion) and this is where for many the Wealthcare and Profit Protection Act is something like affordable care. Most folks are not in the individual market so their experiences are very different so the benefits are not broad by definition but for this 15% of the population this is big in a rubber meets the road way while for most of the population the benefits are less clear and for relatively young folks that make something like living wages matters will appear worse unless they have catastrophe because most folks are already paycheck to paycheck and not loving life so any increase isn't exactly "affordable" to them no matter if you can get some screenings included with your premium.

One thing is sure, we'll continue to have the most fucked up and expensive system in the civilized world and people will keep on avoiding care for financial reasons.

JVS

(61,935 posts)

Skidmore

(37,364 posts)with funds to participate in an employer health insurance pool from my income which was a great deal less than $40K/yr. I realized that others were contributing to and was grateful for the coverage for myself and my children when we needed. There were copays and deductibles too, which I met without complaint because I realized that I could not have footed the entire costs of my teenage daughter's hospitalization or my own surgery and radiation treatments. Later when I lost my job at the same time I was diagnosed with cancer, I was fortunate that my husband had just picked me up on a family plan through his employer because, with a diagnosis of cancer, I could not have coverage. Now with ACA, I will be able to be insured again should something happen to him and I need coverage to help with annual visits to the oncologist to get the prescriptions I need to just live.

A lot of the insurance I have payed in over the years, including insurance for automobiles, house, and life, I will hopefully never need to use for a catastrophic event. However, they are there should my home burn down or I'm involved in an accident.

PeaceNikki

(27,985 posts)Rates and plans might be much different in 12 months.

Although, I personally think you should get covered cuz I know you and shit happens, bro.

Also....

PoliticAverse

(26,366 posts)AnotherMcIntosh

(11,064 posts)

Just try it once a week.

If you are not elderly, it could help acquire a taste for it.

Prism

(5,815 posts)I empathize with you and know many others in your shoes. It really, really bothers me to see so many hostile to recognizing the realities like yours.

How can we fix a problem people refuse to admit exists in the first place?

JVS

(61,935 posts)Isn't that the easiest way to fix problems?

The Midway Rebel

(2,191 posts)6K barely pays for about an hour or so in an ER. A week in the hospital would throw many Americans into bankruptcy without the ACA.

datasuspect

(26,591 posts)LWolf

(46,179 posts)It really doesn't matter if it's 6,000, 10,000 or 50,000 if you don't have it.

taught_me_patience

(5,477 posts)The Midway Rebel

(2,191 posts)datasuspect

(26,591 posts)if free means they take it out of the significant taxes i already pay, then yes.

Habibi

(3,605 posts)what is the silver plan for your exchange? You have the bronze and the platinum costs listed, but not the silver, and from what I've been reading, the silver plans seem to provide the best coverage for a reasonable rate.

datasuspect

(26,591 posts)not as bad as bad and not worse than worse.

Pretzel_Warrior

(8,361 posts)datasuspect

(26,591 posts)child.

B2G

(9,766 posts)Very curious based on all of your posts.

hooverville29

(163 posts)

Union Scribe

(7,099 posts)like so many of your other nasty posts?

Pretzel_Warrior

(8,361 posts)

ProSense

(116,464 posts)See if you qualify for a hardship exemption, and then explore the community health centers.

Wow! Healthcare.gov has answers, including exemptions from fee due to hardship.

http://www.democraticunderground.com/10023754838

Medicaid not expanded in your state? Get health/dental income based cared through HRSA.GOV!

http://www.democraticunderground.com/10023790963

Obama administration provides $150 million for health centers to offer enrollment assistance nationwide

Health and Human Services Secretary Kathleen Sebelius today announced new funding to help more uninsured Americans enroll in new health insurance coverage options made available by the Affordable Care Act. Approximately $150 million will help community health centers provide in-person enrollment assistance to uninsured individuals across the nation. About 1,200 health centers operate nearly 9,000 service delivery sites nationwide and serve approximately 21 million patients each year.

“Health centers have extensive experience providing eligibility assistance to patients, are providing care in communities across the Nation, and are well-positioned to support enrollment efforts,” Secretary Sebelius said. “Investing in health centers for outreach and enrollment assistance provides one more way the Obama administration is helping consumers understand their options and enroll in affordable coverage.”

With these new funds, health centers will be able to hire new staff, train existing staff, and conduct community outreach events and other educational activities. Health centers will help consumers understand their coverage options, determine their eligibility and enroll in new affordable health insurance options. Community health center staff will provide unbiased information to consumers about health insurance, the new Health Insurance Marketplace, qualified health plans, and Medicaid and the Children’s Health Insurance Program.

This funding opportunity was issued by the Health Resources and Services Administration (HRSA), and it complements and aligns with other federal efforts, such as the Centers for Medicare & Medicaid Service funded navigator program.

Today’s funding announcement is part of the administration's larger effort to make applying for health insurance as easy as possible. For example, last week, we released a single, streamlined application that was shortened from 21 to 3 pages. We are committed to providing the type of assistance that Americans need to ensure that they have access to affordable health care.

“Health centers work in communities across the country, giving them a unique opportunity to reach the uninsured in their communities and help connect them with the benefits of health insurance coverage under the health care law,” said HRSA Administrator Mary Wakefield, Ph.D, R.N.

Click on the link http://hhs.tv/Media/PublicResources.aspx for video B-roll and sound bites. To view the files, click on the magnifying glass next to the file title. You can then download the files after registering on the same page.

For information on applying for this funding opportunity, visit http://bphc.hrsa.gov/outreachandenrollment/.

For a list of health centers eligible to apply for this funding visit http://www.hrsa.gov/about/news/2013tables/outreachandenrollment/.

To learn more about the Affordable Care Act, visit www.HealthCare.gov. To learn more about HRSA’s Health Center Program, visit http://bphc.hrsa.gov/about/index.html.

http://www.hhs.gov/news/press/2013pres/05/20130509a.html

http://www.democraticunderground.com/10022820842

http://www.democraticunderground.com/10022566100

ecstatic

(35,089 posts)I'm not a great explainer and there's a lot of confusion here (among the never insured) about the way health insurance deductibles work and when they apply. From my experience, it doesn't come into play unless you begin treatment at an outpatient facility or an out of network facility.

datasuspect

(26,591 posts)yes, that would be very helpful.

Lars39

(26,550 posts)You pay monthly premiums.

You need to see the doctor for the flu, for example: you pay a co-pay, the rest of the bill that you pay goes towards the deductible.

(Not sure if routine physicals that the ACA now covers is applied to the deductible...I'm thinking not applied.)

Once you meet the deductible, the insurance will start paying a percentage, say 70%.

You still pay the co-pay plus 30%(per the example).

Once you have paid what amounts to your out-of-pocket maximum, the insurance kicks in and pays %100.

Until the next year rolls around and you get to do it all over again.

You will have EOBs (explanation of benefits) for each visit mailed to you or you will be able to see them online.

Sometimes there will be multiple charges on one EOB, sometimes there will be several different EOBs for the same visit, depending on what you had done.

The insurance company and the provider(doctor, etc) have a contract that decides on "allowable charges", ie how much the insurance company has decided they will pay for things.

The provider cannot make you pay more than what was stipulated in the contract. So you may get a huge bill, but by the time the insurance company identifies the allowable charges

it is often much lower. So don't pay anything until you get a look at the EOB, and even then wait awhile because sometimes the bill is resubmitted for some reason or other.

Phentex

(16,730 posts)(said in my mayor of the munchkin city voice)

Lars39

(26,550 posts)ecstatic

(35,089 posts)PoliticAverse

(26,366 posts)Deductibles

Co-pays

Out of pocket cap

ieoeja

(9,748 posts)I'm not absolutely certain when the deductible comes into play. But I have had outpatient surgery without the deductible applying. I have had out of network medical care, and it did not apply.

I think** it only applies to an inpatient hospital stay.

**Therefore I am. Ha! I kill me. I'll be here all week. Try the organic, free-range soy.

ieoeja

(9,748 posts)ecstatic

(35,089 posts)

eqfan592

(5,963 posts)This is thru my employer.

pnwmom

(110,305 posts)datasuspect

(26,591 posts)out of pocket max is more.

ieoeja

(9,748 posts)The problem, my dear datasuspect, is that you do not -- no offense intended, but to be brutally honest and hopefuly helpful -- you apparently do not know how medical insurance works. In all the ACA discussions, I've never seen mention of the dirty, little secret that once you have insurance, everyone tends to ignore the rules of that insurance.

To your benefit!

When I have had to use car insurance, I had to pay the deductible amount before the insurance would kick in. But not so with medical. Everything goes to insurance first.

I have a $400 deductible. But I have never, ever seen it applied. To anything. Not to surgery. Not to doctor visits. Nada.

Disclaimer: I've never had a hospital stay. I think it might apply to that.

I sometimes pay a copay. More often than not, they waive the copay.

Then I get a bill. Since you are new to the insurance game, let me pass along what I long ago learned is rule #1 when receiving the first bill following a medical procedure:

[font size=2]Always Ignore the First Bill[/font]

The medical industry has pre-negotiated rates insurance companies. Those rates are lower than the rates people without insurance are charged. Your first bill will not reflect that rate. Nor will it reflect the fact that they have already sent the same bill to your insurance company.

I suspect they trick a lot of people into paying a bill this way that patients would not otherwise have to pay.

Next, you will probably receive an itemized statement including the insurance information (I did not last time which caused some confusion). This statement should include:

- initial charge

- insurance agreed rate

- insurance payment

- the portion you are supposed to pay

This will probably come from your insurance company, not from medical. As you do not make medical payments to your insurance company:

[font size=2]Store and Ignore[/font]

Wait til you get a 2nd bill from medical. Chances are, you won't. I usually don't. They're generally satisfied with what they get from insurance, and don't want to bother with it after that.

You know, they actually offer Associates Degrees in "Medical Billing". That is how totally fucked up it is. But if you follow the above rules, you should be in the clear. And end up paying very little for actual medical care.

Unless they put you on a prescription. Then you're royally fucked. But that is a whole other can o' beans.

JSK

(1,128 posts)If we all knew for sure that we would never use our health insurance. Do you know that you'll never be involved in a car accident like a friend of mine who has been dealing with a traumatic brain injury since she was t-boned in a horrible accident 15 years ago? Do you know that you'll never get cancer like my nephew did at the age of 29 and need very expensive complex surgeries?

Rex

(65,616 posts)You list the worst and the best, what about somewhere in the middle? It is interesting how some people have had an easy time getting insurance and some have had a horrible time and cannot afford the insurance. Must be a state by state thing.

datasuspect

(26,591 posts)best worst and the worst worst.

silver is in the middle.

the middle worst.

it would solve my insurance needs with a program i simply don't have the extra to spend for it.

healthcare plays no part in any of this.

Rex

(65,616 posts)Are you in a red state, like me?

datasuspect

(26,591 posts)but i don't qualify for subsidies, tax credits or anything.

the point is that after all the expenditure it still doesn't solve the healthcare question.

it solves the health insurance question. these are two different things.

valerief

(53,235 posts)We all want Medicare for all. They won't give it to us.

What are you recommending?

What's your MAGI? Single or family? What's your state?

LWolf

(46,179 posts)You don't have insurance, so don't get sick or die fast.

You do have insurance, with a deductible that you can't cover. So don't get sick or die fast.

In neither case does one get "affordable" CARE.

Generic Other

(29,082 posts)One would think it was relatively common, probably inexpensive. It cost $250,000 due to complications.

These are the kinds of bills we should all be petrified about. The lose-your-house-all-your-savings-live-in-your-grown-kids-basement scenarios. You now have insurance against this. And only a fool would bet they would never need it.

Also, make sure you haven't misread what benefits are provided, so you don't spread wrong information. Several people upthread have mentioned preventive care being covered.

*And yeah, I think we should all have universal -- cradle-to-grave for free. That is the least we have earned. It is our tax money, our labor, our sweat equity that built this country. Workers are entitled to and should fight tooth and nail to have education, medical care, unemployment, disability and old age benefits. Without these things we are nothing but slaves to an overbloated military and way too many fat cats!

melody

(12,365 posts)LWolf

(46,179 posts)Insurance is not care, and care still costs.

bullimiami

(14,075 posts)I think your max yearly penalty is 285.00.

infiniti30

(2 posts)The key to this was supposed to be affordable. From the sounds of this thread and many other complaints this is not the case and it is only going to get worse.

gopiscrap

(24,765 posts)

Zorra

(27,670 posts)Flying Squirrel

(3,041 posts) enjoy your brief stay.

enjoy your brief stay.ScreamingMeemie

(68,918 posts)Family of Two in (gasp!) Texas:

but that was a very, VERY good try at being concerned, dear.

haele

(15,481 posts)First off, you don't pay them up front when you go to the doctor or get a procedure done. There's usually a co-pay you'll pay first, then the hospital/clinic/lab/medical facility will bill the insurance, the insurance will negotiate costs, and then you will get billed for whatever is left until your deductible.

I have gone through this for the past seven years with employer based health insurance. And we always meet our deductible for the year sometime around April or May, so we always get a nasty set of bills we have to pay off over the year (this year, it's $9K, plus another $4K or so far in "co-insurance", something most of the plans I've seen in the ACA plans don't have)

There are a few things I have done over the year to ease the financial pain (I have student loans, too...)

First thing, the insurance company doesn't care if you pay whatever your bill is going to be after they're through with the negotiations of the provider and the co-payment is made are done or not. That money in the "you owe" line goes straight onto the "deductible" ledger so far as they are concerned.

Second, you don't have to pay medical bills up front or right away. First thing I do is to contact the billing department, and set up payments for the bill - even if it's five dollars a month, the "good faith" keeps you out of collections.

Third, ask if there is additional assistance you can sign up for or discount. As in, Walgreen's gives us a discount on some of the medication through their family plan, and because we keep regular payments, we managed to get recovery therapy payment assistance - an additional 15% off - through the local hospital where my disabled spouse has doctors. There are also charities that sometimes will pitch in for orphan conditions or one a major donor has an interest in. This year, we still owe that hospital about $2K for everything that went on prior to the deductible kicking in, but they are working with us, and several times over the past years, have cut us a significant deal to pay off the bills when they come close to closing - the old "if you can do $100 today, we won't bill you the remaining $60" agreement.

Finally, keep all your receipts. Your deductible will be over 10% of your annual income, correct? If you're making $40K a year, $4K in annual medical expenses - even if you are making payments - that are not already tax deductible can be taken off your income taxes. Include the transportation estimate to and from therapy, doctor's and lab visits, etc. If you are making payments, you can estimate how much more you will be paying on the services fin the year that that billing was initially invoiced, and include that.

If you don't already have a significant tax deduction such as a business or a mortgage deduction, that can really help around tax time.

Most people don't take a medical deduction because there are usually not enough out of pocket medical payments that are not already covered through either an HSA/FSA or through other subsidies that are tax-exempt (as in, the premiums that are taken out pre-tax in employer coverage) Every year, we have been able to use the return from the medical deductions to pay off the out of pocket costs that are still outstanding for the previous year.

It's a sucky position to be in. But we're able to just pay our medical bills - and under our "uniquely American" model of health as an investment business, until we can get single payer, we take the best options we can operate under.

Haele