General Discussion

Related: Editorials & Other Articles, Issue Forums, Alliance Forums, Region ForumsAs it is the plan is to cut social security benefits by 25% when the trust funds are spent.

That's the trade off when you consider chained CPI.

If you believe our economy will be doing well for the rest of your days I suppose you can bet your future on that assumption and make no allowances for future cuts.

But if it doesn't turn out that way, no one can say they weren't warned.

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

trumad

(41,692 posts)dkf

(37,305 posts)I am more interested in presenting the options to others who may be relying on it.

Chained CPI would benefit me personally though. It would allow for more of a trust fund during more of my retirement. That's how it affects my planning.

Should I be more concerned about the current generation than my own? I don't know.

Warren DeMontague

(80,708 posts)trumad

(41,692 posts)Warren DeMontague

(80,708 posts)"Entertained"?

Because If that's really the case, then the folks on DU who go on about cuts to SS being an irrevocable line in the sand, should qualify it to explain that they only mean for themselves.

trumad

(41,692 posts)There is a line in the sand. You cut--- you're fucked.

BluegrassStateBlues

(881 posts)Best they pull the whole thing and let seniors fend for themselves.

spanone

(142,261 posts)dkf

(37,305 posts)Swede Atlanta

(3,596 posts)by most estimates, that doesn't address the fact that at sometime in the next 15 years it will no longer be possible to pay benefits at the current rates.

So the choice will be to cut benefits, in some cases fairly drastically, find new sources of funding such as lifting the SS income cap or a combination of targeted, specific cuts based around means testing coupled with increases in revenue.

grasswire

(50,130 posts)A better choice is to means test Social Security, starting NOW.

Every program benefitting the 47% is means tested.

Student Loans.

SNAP

Medicaid

Energy assistance

Housing assistance

And so on...........

That's why it's only fair for Medicare and Social Security to be means tested.

Vincardog

(20,234 posts)demwing

(16,916 posts)what about unemployment insurance? Both have means testing.

I hear this explanation quite a lot, and I've always accepted it. Now I'm thinking we ought to look at it again, and question whether means testing really "makes SS a welfare program."

Bluenorthwest

(45,319 posts)You pay in, you draw when you qualify. You don't get it in weeks in which you have earned income because it is about lacking employment. But no one is disqualified for the benefit by having other resources or savings or because of how much you make when employed.

Vincardog

(20,234 posts)Loans because they have too much money.

Question whatever you want but sell your Faux "Facts" to someone else.

demwing

(16,916 posts)Last edited Thu Oct 24, 2013, 08:52 PM - Edit history (1)

and that I be fit for employment. Not a test of financial means, but certainly a test of physical means. I have to have the means to find and keep employment. Being unable to work is a disqualification.

2. There is absolutely a financial means test for Federal Student Loans, subsidized or unsubsidized: http://studentaid.ed.gov/types/loans/subsidized-unsubsidized

Save your mindless cheerleader routine for someone who gives a shit and a half.

Hoyt

(54,770 posts)Personally, I'd rather put everything on the table now -- under Democrats -- and see if there is not some plan that will shore up SS, spur jobs (especially for the young that will be paying our SS), protect those at lowest end of scale, etc.

It's not going to be an easy fix. Raising the cap is certainly part of the solution, but it doesn't solve the whole problem.

The alternative is to kick the can down the road a few more years and let things hit the fan under a Republican regime. Won't be pretty.

brush

(61,033 posts)I know because at time it would be in October that my FICA deduction would reach it's yearly requirement and I would see a larger check for the rest of the year that would feel almost like a raise. After the cap was raised that larger check didn't happen until sometime in December if I recall correctly.

So it's not like this is something that has never been done before.

As prices rise it makes absolute since that the cap should rise.

And why do you think it won't solve the problem when it has before.

Hoyt

(54,770 posts)Also, if we raise the cap, benefits go up for those over the cap. More importantly, raising the cap is a big tax increase for those affected. That is fine with me (screw the rich), but that is also money needed for other things, like unemployment benefits, jobs programs, food stamps, etc. You can't just look at SS in isolation.

brush

(61,033 posts)people in the next income above the present cap will take home maybe $20 a paycheck?

Big huge sacrifice.

C'mon, we're not talking anything draconian here.

Hoyt

(54,770 posts)Again, Their SS benefits will increase, so all of that does not go to shoring up SS. And, I think we need that 6% in other places, so I'm hardly against tax increases.

brush

(61,033 posts)Plenty of other places to cut. We need to put that meme out there instead of furthering the cut SS meme.

Hoyt

(54,770 posts)that cuts a lot of jobs, and thugs won't agree to it easily.

brush

(61,033 posts)I'm betting that hardly anyone on this site is favoring cutting those things you cited.

Let's stop ignoring the elephant in the room and talk about cutting the defense budget that eats up half of the budget by itself.

Do you agree?

Hoyt

(54,770 posts)I realize no one is in favor of cutting those things -- neither am I. That is what I am saying.

If we increase cap on SS (which I am for, but recognizing it is not the panacea some think): 1) it doesn't resolve the SS fully; 2) that is 6% of taxes on higher income people that will not be available for those other things, and whatever else comes along.

DeadEyeDyck

(1,504 posts)It is not. It is an insurance program paid by your employer. Insurance is the transfer of risk for a fee.

You can't cut unemployment benefits to find something else. It is an insurance pool.

Hoyt

(54,770 posts)You want to just let them starve after that because of fund accounting conventions?

Bluenorthwest

(45,319 posts)their income. Boo fucking hoo. But Obama's proposal in the past was a doughnut hole, cap remains where it is, tax resumes at a higher level, say 175K. So by the time anyone is paying extra they have very little room to complain.

I say that boo hoo, by the way as someone who earned over that cap at age 24 the first time. I again say boo hoo.

Hoyt

(54,770 posts)I'm all for increasing taxes on the well to do. I'm not for blowing our wad simply on SS because that won't improve things for the 99% (or even 50%).

leveymg

(36,418 posts)particularly capital gains. It's really quite simple, if we just insist this is the ONLY acceptable solution.

No more deals.

brush

(61,033 posts)Are you in favor of raising the cap or not? Be clear so we know where you stand.

Hoyt

(54,770 posts)Hoyt

(54,770 posts)another 5 to 10% percentage point increase in income above say $60,000 to fund all the other stuff we sorely need?

Bobcat

(246 posts)Totally agree. But let's cut to the chase here. The vast majority of working class and middle class income earners have paid the FULL SS tax rate on EVERY DOLLAR THEY HAVE EVER EARNED IN THEIR LIFETIME. They did not earn enough to reach the cap. I paid the full tax on every dollar earned for MORE THAN 50 YEARS! Every dollar I have EVER EARNED has been subjected to the FULL tax. If middle income earners like me can afford the FULL tax on every dollar earned for their entire lifetime, surely the millionaires and billionaires can afford it too. If it's "fair" for me to pay the full tax, it's fair for the wealthy too. ELIMINATE THE CAP!!

AnotherMcIntosh

(11,064 posts)to fund more wars, like the one that we almost had in Syria.

Hoyt

(54,770 posts)

jeff47

(26,549 posts)The Social Security trust fund is invested in US bonds.

There is no way for politicians to "borrow more from it". Because they've already borrowed 100% of it. That was the point of the trust fund - to invest all of it in something.

It would be insanely stupid to save the trust fund as stacks of money in some vault.

AnotherMcIntosh

(11,064 posts)"When Social Security has a cash-flow surplus (when more is coming in that being paid out) Social Security taxes are 'available' to pay for other programs."

"The Republican report says: "Treasury should have $6.5 trillion in surplus FICA taxes but has only $2.6 trillion." This deficit exists because Republicans borrowed trillions in FICA taxes to offset tax cuts for the rich, and fund Bush's unnecessary wars.

"Your Social Security Fund is owed this money back by its borrowers, the Republicans. We middle class are left holding an IOU, eg U.S. debt, the mega-rich got your money and spent it.

http://www.dailykos.com/story/2013/01/01/1175559/-The-GOP-Borrowed-your-SocialSecurity-Money-for-their-Wars#

Hoyt

(54,770 posts)It won't be paid back even if we confiscate every penny of wealth in this country.

ucrdem

(15,720 posts)Trust fund bonds are real as any other UST-backed currency. Unless the US goes belly up that is.

Hoyt

(54,770 posts)Not reassuring, when the economy that produces jobs is fragile.

jeff47

(26,549 posts)The national debt is bonds that we have sold in order to borrow money.

If buying bonds is throwing money away, then we have no national debt. Are you going to make that claim now?

PoliticAverse

(26,366 posts)The $6.5 trillion they are talking about is how much SS will owe to future recipients in excess of what

its projected revenues are.

jeff47

(26,549 posts)Next, are you gonna quote the Amish on how computers work?

The "money is all gone" is a Republican talking point designed to fool people into cutting the program. It's a lie. The money is invested. Social Security is continuously being paid back as the bonds mature.

Some dumb Democrats are falling for "the money is all gone" story, and stupidly using it to attack Republicans.

If the money was really all gone because it's in bonds, then there's no reason for people to worry about the US owing money to China or any other part of the debt. Those are bonds too.

AnotherMcIntosh

(11,064 posts)http://en.wikipedia.org/wiki/Daily_Kos

jeff47

(26,549 posts)AnotherMcIntosh

(11,064 posts)We're done.

jeff47

(26,549 posts)but would be a fantastic tool to destroy Social Security.

If the trust fund is "gone" because it's been spent to buy bonds, what's our national debt? That's the other side of those bonds.

If the trust fund's money is gone, our national debt is $0. Is that what you want to claim?

muriel_volestrangler

(106,891 posts)If you do "read the entire thing in context", ie read the Republican report from 2011, you see that the $6.5 trillion is (page 5):

PoliticAverse did point this out in reply #107, more concisely than me. But you ignored that.

When the letter to the editor, which the Daily Kos writer quotes, says "Treasury should have $6.5 trillion in surplus FICA taxes but has only $2.6 trillion", that 'Treasury should have' means 'it would be nice if Treasury had...', not 'Treasury is meant to have, but has somehow been cheated of,...'.

"This deficit exists because Republicans borrowed trillions in FICA taxes to offset tax cuts for the rich, and fund Bush's unnecessary wars" is complete nonsense. It's wrong. The amount of FICA taxes 'borrowed' is set by the level of the FICA payroll taxes, and the level of benefits paid out in a year. Any surplus has to be 'borrowed' by the rest of the government, by law. The decisions of Bush, or anyone else, on what wars to fund, or income tax cuts to make, won't affect it at all. What those affect are the amount of federal debt to the public.

And since it is borrowed, there is an obligation to pay it back. It has not 'disappeared' in any sense, nor will it (unless nutty politicians decide to default on the US debt, as the worst of them were proposing recently).

AnotherMcIntosh

(11,064 posts)our entire adult lives, we have seen politicians like Reagan squander the future of this country and then renege on the Social Security obligations. When Reagan took office, the normal retirement age for receiving Social Security was 65. What is it now?

Raising the age for when normal payouts can begin is one way to renege. That was done in Reagan's time and has already been discussed in recent years.

Another way is to renege is reduce payouts is by sending payments which fail to keep pace with inflation. We have seen the chained-CPI proposal to do that. That's why sensible people objected to the Cat Food Commission.

My original post at #32 was

"SS is actuarially sound for the next 10-15 years" only if the politicians don't borrow more from it to fund more wars, like the one that we almost had in Syria."

Do you disagree with that?

Who other than you has said with respect to the funds to be paid out: "It has not 'disappeared' in any sense ..."? Didn't one of our candidates want to put the Social Security funds in a "lock box"? Was he to be criticized for that? Did he fail to understand:

"since it is borrowed, there is an obligation to pay it back. It has not 'disappeared' in any sense, nor will it (unless nutty politicians decide to default on the US debt, ..."

Do you, like the poster that you mentioned, view this as a "blue team vs red team" type of thing?

If the DC politicians are wearing the right color jerseys, can they spend an apparent endless amount of money on war and military-related activities without having any effect whatsoever on their paying Social Security benefits? Will it have no effect on their further reneging on the Social Security payouts?

Is it OK so long as they are wearing the right color?

muriel_volestrangler

(106,891 posts)As I said, the amount that politicians 'borrow' from Social Security is not affected by government decisions on things like wars or other expenditure from the general fund. The Social Security fund has not been affected by the spending Bush did on war in Iraq. It has not been affected by his tax cuts.

"Who other than you has said with respect to the funds to be paid out: "It has not 'disappeared' in any sense ..."?"

Everyone who understands Social Security.

"Didn't one of our candidates want to put the Social Security funds in a "lock box"?"

They are in a 'lock box'.

"Do you, like the poster that you mentioned, view this as a "blue team vs red team" type of thing? "

I cannot see anyone in this thread who has talked about a "blue team vs red team" type of thing. I mentioned PoliticAverse, who pointed out the $6.5 trillion figure was far different from what the Daily Kos writer thought it was. Who are you talking about?

"If the DC politicians are wearing the right color jerseys, can they spend an apparent endless amount of money on war and military-related activities without having any effect whatsoever on their paying Social Security benefits? "

Any politician can spend on war without affecting the Social Security benefits. What they would affect is the deficit, and the future interest payments to Treasury bond-holders. This isn't about a side - it's about understanding how Social Security is funded, and how the general federal fund, from which things like wars are paid for, is funded.

CreekDog

(46,192 posts)that's a budget increase of 3%.

muriel_volestrangler

(106,891 posts)which isn't the same as dividing it by 75 to get the amount for each year. The 2013 figure (the Republican report was from the 2011 Trustees' Report) is $9.6 trillion, here: http://www.ssa.gov/OACT/tr/2013/IV_B_LRest.html#267528

They also express it in terms of the percentage of expected taxable payroll each year (2.6%) or GDP (0.9%). With the current GDP being $16.6 trillion, that's about $150 billion per year, in current money.

(I presume 'taxable payroll' means with the cap currently in force; I think, though I can't remember where now, one of the other documents I linked to said the cap limits the taxable payroll to about 82% of the total payroll - so if the cap were removed, but no-one's benefits were increased at the same time, you'd expect to get 18/82 = about 22% more money coming in - which would be roughly another 2.7% of total payroll, or about what would be needed to fund SS for 75 years. But I may have got that bit wrong).

CreekDog

(46,192 posts)are we literally going to bank it for 75 years? no.

muriel_volestrangler

(106,891 posts)You ask 'how much would I need now to solve this and not have to add still more later?'

"are we literally going to bank it for 75 years?"

Well, the idea of the Social Security trust fund was to 'bank' (ie effectively lend, at the prevailing rates, to the general fund) excess FICA taxes for several decades. No, it won't be literally done this way - the only way to get hold of that amount now would be to borrow it; so you'd end up borrowing money from the markets, and then lending it to the rest of the government, which doesn't actually need that amount now. But the "how much would we need now" is a useful metric.

Hoyt

(54,770 posts)And clearly a whole lot less than what today's beneficiaries put in.

jeff47

(26,549 posts)

Why are you so desperate to destroy Social Security?

All you need is "Saddam shipped the WMDs to Syria" and you'll have bought all the recent Republican talking points.

Hoyt

(54,770 posts)Ignoring the facts, don't change them. The sooner we shore it up properly, the better. Or, we can wait until a large cut is inevitable in a few years, and see how the Republicans will handle it. I know what the results will be.

jeff47

(26,549 posts)The "facts" you are citing include that projection - that's how they got the 25% shortfall in 20 years. About 2% GDP growth means the trust fund never runs out of money.

You don't quite seem to be able to explain how for every single year of the next 20 years, the economy will grow at half the rate of the last 8 years - which even featured this lovely recession we're just getting out of.

And you are proposing a large cut. You are claiming it's impossible to raise taxes enough, so we have to do Chained CPI. Which is a massive cut for anyone who lives more than a few years on Social Security.

So I'm left trying to decide if you just don't know what you're talking about, or if you're out to destroy Social Security.

Hoyt

(54,770 posts)growth rate down. Finally, it seems to me that GDP growth nowadays is quite different from previous years in that wages don't make up as much of that (admittedly, I'm not as sure how this shakes out, so it's just wild speculation).

jeff47

(26,549 posts)

Which would mean it isn't 2%.

Historical average is 3%. Including both booms and busts. The last 8 years, which have been pretty darn awful, are about 2%. We need something like 2.3% over the entire 20 years for the trust fund to never run out of money.

And that's if we do absolutely nothing. If it starts looking a little low in 10 or 15 years, we can still raise the payroll tax cap. If 10 years from now we make it capture the same number of people it did in the 1960s, the program will also have ample money. Or are you going to now claim that raising taxes that much would kill the economy....despite the actual economic performance of the 1960s.

How 'bout instead of shredding the program today because it might be in trouble 20 years from now, we see what happens over the next 10 years?

Hoyt

(54,770 posts)Last edited Wed Oct 23, 2013, 11:53 PM - Edit history (1)

See Section V(B) 6.

The most optimistic assumption assumes growth over 3.5%.

Bobcat

(246 posts)I have yet to see a projection based on the AVERAGE GDP (income) growth for the past 100+ years. Those projections would be calculated on a 3% annual average growth rate . The current projections of a shortfall are based on the same faulty projection as the basis for balanced budget under Reaganomics - a faulty measure of economic growth. The projections of a SS shortfall are based on a low ball long term estimate of less than 2% and the wildly inaccurate projections of the Reagan years were based on a 12% growth rate. Ask David Stockman.

No "journalist" that I know of has yet to even ask what the long term growth rate the doomsayers are basing their estimate on is. Don't hold your breath.

muriel_volestrangler

(106,891 posts)That was while most of the rest of the world was stuck in poverty or war. More recently, other countries have been able to take more of the economic opportunities for themselves, and more of the world growth.

Plus there will be future problems of climate change, which may mean economic growth has to be limited.

jeff47

(26,549 posts)Growth in other countries does not have to reduce growth in the US. Their growth can actually cause higher US growth as the two countries trade.

Someone has to make the stuff to replace all the fossil fuel systems we currently use. So while climate change will devastate the growth of Acme Coal Furnace, it will help the growth of Consolidated Wind Power.

leveymg

(36,418 posts)Bunnahabhain

(857 posts)I know we are not. I do not think it's the financially prudent thing to do.

closeupready

(29,503 posts)on the SS trust fund and fee it to death, you won't even notice, and they'll laugh all the way to the bank, since that was your money that you simply threw away.

Bunnahabhain

(857 posts)but I'm sure you feel better telling someone that is saving for his retirement on his own that Wall St. is laughing at him.

Grasshoppers always laugh at ants.

closeupready

(29,503 posts)If you've discounted the value of the money you've paid in to the social security trust fund to the point where it's not even part of your plan, then you have effectively embarked on a road leading to default on the bonds held by the SS trust fund and also reduction if not elimination of payment of benefits.

Wall Street has been effective at spreading the lie that "everyone knows entitlement benefits need to be cut"; that you have subscribed to that lie is something you do at your own peril.

Bunnahabhain

(857 posts)Your small little mind can't hold enough variables to know why I would expect to get nothing from SS. I expect to see SS get means tested, and if one expects their retirement income to be above the threshold, it would be fiscally unsound to count on SS payments as part of their income. Not everyone views retirement from the perspective of poverty.

closeupready

(29,503 posts) Done.

Done.Bunnahabhain

(857 posts)Now there's a Yoda-like observation.

closeupready

(29,503 posts)Did I enter a timewarp, too?

muriel_volestrangler

(106,891 posts)We can shorten that to "I got mine".

Bunnahabhain

(857 posts)but you would be wrong. My personal planning has nothing to do with my views on public policy. That's just stupid on your part to think so. It's stupid not to plan your finances from a financially prudent stand point. Not doing that is how people with good jobs end up poor.

muriel_volestrangler

(106,891 posts)"Is anyone under 45 actually including SS as a material part of their retirement plans?

I know we are not. I do not think it's the financially prudent thing to do."

You think that everyone should ignore SS as part of their retirement plan. Your stated reasoning for this is that you expect yourself to be above a means test limit. So you think everyone should assume they will be well off, like you. Your personal planning should have nothing to do with my views on public policy, but you have failed at that.

Bunnahabhain

(857 posts)My planning =! your planning (or that of anyone else)

Additionally planning worse case scenarios is always the wisest choice. Planning for a full SS benefit in its current form 20+ years from now is not prudent. That's my opinion of if it's not yours that's fine. Getting upset with me for how I do my planning is just juvenile.

muriel_volestrangler

(106,891 posts)But you are advising everyone else to think that too. That's what you said in #5, and what you've said again in #178.

closeupready

(29,503 posts)Report on every single one of his right-leaning posts.

Bunnahabhain

(857 posts)I've heard it all now. Please make sure you report all those "right wing" posts of mine where I argue for social democracy, universal healthcare, minimum guaranteed income and oh so many "right wing" positions like those.

Are you really of the belief that a person who plans his retirement in a prudent manner is automatically right wing? Do I have to run all my credit cards up and go bankrupt to be "left wing?" FYI, I know real right wingers that don't have a pot to piss in let alone a window to throw it out of and highly progressive people that start to lose sleep if they have less than 200k in their contingency fund. Running one's personal finances in a prudent manner has nothing to do with ideology.

Bunnahabhain

(857 posts)It may not be possible but it's prudent. How can planning for the worse not be a good thing? Work towards the best, plan for the worst.

muriel_volestrangler

(106,891 posts)It's not logical.

We return to closeupready's point - that if everyone, or even a lot of people, said "we won't need Social Security", it'll encourage politicians to get rid of it. Politically, it just encourages the Republicans to say "Social Security is only for the imprudent", and then they'll persuade some people it should be cut.

Bunnahabhain

(857 posts)But huge leaps are what makes the Internet run I guess. The Repubs are going to do what the Repubs are going to do. I mean it's not like they're not trying to cut it right now. If we encourage people to be dependent on SS in retirement folks will be even worse off. FDR, the guy that got us SS, firmly believed SS was merely a supplemental income in retirement and it was never designed to be the main or sole income. Is that the case for many people? It sure is. Should we try and create a reality where this is not the case? I firmly believe so and I think prudent personal financial planning is part of that.

And if things are never attempted they'll always be "impossible."

AnotherMcIntosh

(11,064 posts)dkf

(37,305 posts)Bunnahabhain

(857 posts)

closeupready

(29,503 posts)Don't think so. And I'm alerting on your ass.

ProSense

(116,464 posts)"I know we are not. I do not think it's the financially prudent thing to do."

My, aren't you lucky. Some people think it's "financially prudent" to eat in order to live to retirement.

Bunnahabhain

(857 posts)I am not some rich politician's kid so I had to make my own "luck" which I refer to as "busting my ass." Being financially prudent is something we all wish Dubya had been so I fail to see why someone on DU would mock a poster for being financially prudent. Growing up very poor leaves its mark on you. I guess it's easy when you did not grow up in bone crushing poverty but rather as some rich guy's spoiled brat.

ProSense

(116,464 posts)...because whether people can afford to eat or not should be based on "luck"? Are you suggesting that the working poor aren't "busting" their asses? The RW likes to argue that people who rely on Social Security are lazy "takers."

They like to claim people are struggling because they don't work or work hard enough.

"Being financially prudent is something we all wish Dubya had been so I fail to see why someone on DU would mock a poster for being financially prudent. Growing up very poor leaves its mark on you. I guess it's easy when you did not grow up in bone crushing poverty but rather as some rich guy's spoiled brat."

I fail to see "why someone on DU" would be suggesting that people ignore or cut Social Security, and imply that it's irrelevant.

Bunnahabhain

(857 posts)Because I do not include it in my personal financial calculus for retirement I am therefore saying I want cuts? With thinking like that it's a good thing your daddy is a rich politician.

jeff47

(26,549 posts)For example, you didn't become disabled and unable to work at 20. Or a host of other ways that our best laid financial plans can be utterly annihilated through no fault of our own.

To answer your original question, why is it "financially prudent" to make plans based on a prediction that has gone so wrong? They've been predicting Social Security will be broke in 20 years for the last 30 years. The current doomsday prediction is based on 1% GDP growth, while the average over the last 100 years has been 3%.

Financial prudence would mean looking at the numbers underlying the prediction and discovering they are bullshit. If you disagree about financial prudence, I've got a wonderful investment opportunity to discuss in the over-water traffic route industry.

ProSense

(116,464 posts)financial crises, from Enron through today.

dkf

(37,305 posts)Then it turns into pay as you go where payroll taxes are used to pay benefits.

That's when the projected inflows are estimated to be 75% of benefits. Thus the expected 25% cut.

jeff47

(26,549 posts)Which is a massively low estimate.

Around 2% GDP growth means Social Security never runs out of money - the trust fund would not be exhausted in any reasonable time-frame.

It's really not a good idea to try and fix a problem that will occur 20 years from now that is unlikely to exist. It's an especially bad idea to harm people today in order to do so.

muriel_volestrangler

(106,891 posts)P.20, CBO 2013 Long-Term Budget Outlook:

benchmark, CBO projects that over the 2023–

2038 period, real earnings per worker will grow at an

average annual rate of 1.2 percent and real GDP will

grow at an average annual rate of 2.0 percent. For the

longer period from 2023 to 2088, the corresponding

figures are 1.4 percent and 2.2 percent, respectively.26

http://www.cbo.gov/sites/default/files/cbofiles/attachments/44521-LTBO2013.pdf

Or the 2013 Social Security Trustee's Report:

Average annual percentage change in Productivity (total U.S. economy), for 2024 and later - 'intermediate' 1.68%, 'low-cost' 1.98%, 'high-cost' 1.38%

http://www.ssa.gov/oact/tr/2013/II_C_assump.html#95492

http://www.ssa.gov/oact/tr/2013/2013_Long-Range_Economic_Assumptions.pdf

jeff47

(26,549 posts)Newer reports have tweaked the GDP up, but they've also tweaked the productivity growth to get them roughly the same doomsday.

Bunnahabhain

(857 posts)Becoming disabled and unable to work at 20 is an extremely small possibility. Now, walking blindly through a mind field and not getting blown up? That's luck.

Now, to your "answer" to my original question: financial prudence is planning for worse case scenarios. Worse case: I collect no SS. If I plan for this I and my family are not damaged. If I do not plan for this and it happens we are damaged. If I plan for it and it does not happen? Well now I have money above my budget. Do you look at your retirement portfolio and base your retirement plans around a 25% yearly return? I sure as hell hope not as that's not financially prudent. Do you plan your retirement cash flow upon a liquidation basis or on a 5% spend rate?

Plan for the worse, hope for the best. Excellent formula for happiness and success.

jeff47

(26,549 posts)There's an enormous number of ways perfectly reasonable and prudent financial plans can be utterly destroyed through no fault of the person making those plans. Becoming disabled was one example.

Then what's your plans when you have a stroke tomorrow and are no longer able to work? Oh wait....that would be "becoming disabled", which will never, ever, ever, ever happen so we can ignore it.

OTOH, Social Security being gone, which requires believing that we'll spend the next 20 years growing much slower than the previous 100 (or even the last 8), and can be easily fixed by raising the FICA tax cap, is so likely to happen that it must be part of anyone's financial plans. And we should spend our time mocking people who weren't clever enough to plan for jobs that pay well.

Bunnahabhain

(857 posts)And if I have a stroke tomorrow and can't work? I have long term care insurance and long term disability insurance. Don't you? I know my benefits in those policies. Do you know yours? This is being what? Oh yeah, financially prudent.

And yes, I also figure I'll be paying more FICA as I have said here repeatedly I figure the cap will be raised. That's what? Oh yeah, financially prudent.

Lastly, I have not mocked anyone that did not mock me first.

Edit: and as to strokes...I keep myself fit, exercise, and monitor my BP. I minimize my risk for stroke as this is being prudent with my health. Do you? I hope so as I want everyone to lead healthy, productive lives.

jeff47

(26,549 posts)In fact, you rejected your luck in not having something awful happen to you as relevant.

It's extremely relevant. That's why you bother buying disability insurance, among other things. Guess what? Your insurance company may disappear when you need them most. "Oh, but I use reputable large companies". AIG was a reputable large company. There's no reason to believe your insurance company will be bailed out by the government.

"My homeowners insurance will protect my house". Good news! Your house was just foreclosed on. Sure, you paid the mortgage on time, but there was a paperwork mistake at the lender and the Sheriff's here to throw you out. But in about 4 years, your lawsuit against the bank will get you 10 cents on the dollar! Assuming you can afford to pay your lawyer that long.

Shit happens. The lack of shit happening to you so far is not evidence that shit does not happen. That's the point of programs like Social Security - to provide a floor for everyone, so when shit happens we don't fall below that floor. The need for that floor does not go away because you are "financially prudent". Thus the program will also not go away, especially when the "fixes" are either not going to be necessary or are going to be easy.

Apparently I'm going to have to link the definition of "example" for you.

Bunnahabhain

(857 posts)You do not want to listen. You have decided you know best. Obviously I am an idiot and a lucky one at that as apparently someone else has gone and bought me insurance policies against calamity.

Only on DU.

jeff47

(26,549 posts)You're still not bothering to consider what I'm saying, because you're busy bragging about your financial planning.

My points are two-fold:

1. The best financial planning in the world does not absolutely guarantee a secure retirement. It is literally not possible to reduce all financial risk to zero. Hence the need for a floor like Social Security, and the reason it will be "saved".

2. All of us who are well off enough to consider financial planning and retirement are the recipients of significant amounts of luck - we didn't have something happen to us that left us mired in poverty.

Those should not be terribly controversial. But they aren't conducive to patting yourself on the back.

Bunnahabhain

(857 posts)Your first point is a straw man. I never made any assertion concerning a "guarantee" of a secure retirement or reducing financial risk to zero. Not only is that a straw man it's funny you feel you need to point this out to a guy who's done nothing but explain his stance for financial planning is one of prudence.

Your second point does not use the word "luck" per the standard definition. Luck: success or failure apparently brought by chance rather than through one's own actions. Now, if I had been born as Warren Buffett's son instead of rural povery I would have been "lucky." If I had "been shooting at some food and up through the ground it came; a bubbling pool" I would have been lucky. Instead my modestly comfortable life was created through active steps on my own. Did I receive "help" in the form of student loans for grad school, etc? Sure thing. Is that "luck" though? Nope.

One of my first jobs in high school involved sales. An old hand told me, "The harder you work, the "luckier" you get." I think there's quite a bit of truth in that.

just us

(105 posts)anyone under 25 will benefit from the end of the boomers and a drastic drop in seniors.

Warren DeMontague

(80,708 posts)I guess that only applies to boomers, huh.

Throd

(7,208 posts)If it is there, so much the better, but I'm not counting on it.

liberal_at_heart

(12,081 posts)are.

Bunnahabhain

(857 posts)I'm not counting on it. Apparently this makes me a bad person on DU. I can sleep well at night even knowing apparently I'm a bad person on DU.

liberal_at_heart

(12,081 posts)Social Security if properly funded.

brush

(61,033 posts)It certainly won't fly as there will be wholesale revolt if they try something like that.

Only the most cold-hearted repug would even have the nerve to say to retirees that we're cutting the money you worked your whole life for by 25%.

Bunnahabhain

(857 posts)in multiple projects. Usually about 2030 = 75% of current benefits under current conditions.

Hoyt

(54,770 posts)brush

(61,033 posts)in Greece ans Spain.

Seems everyone knows that but the teabaggers . . . and a few here.

Hoyt

(54,770 posts)Saying you don't have cancer, won't cure you. It might make you feel better for awhile, but that's about it.

brush

(61,033 posts)for what's right. And I'm far from the only one that feels that way about SS benefits they've earned over a lifetime of working.

Guess you haven't found anything you feel strongly enough about yet

Hoyt

(54,770 posts)Again, I'd rather tweak things now, than under a bunch of Republicans with an automatic 25% cut in their pocket.

The fact that the so-called Trust Fund bonds only cover 3 years of benefits should tell you that each generation has it's benefits paid by the next. We paid for our parents and 3 years toward our benefits. If our younger folks face a tougher economy, you and I as SS beneficiaries will suffer unless something is done.

Chan790

(20,176 posts)vs.

Benefits can't be cut so we need to figure out how to raise revenues without raising payouts other than assumed COLA increases. (Mine.)

Worst case scenario (to me), we float the FICA rate while eliminating the tax cap (but maintain a benefit cap) to insure benefits cannot be cut and income will always equal or exceed payouts as a necessary consequence of the mathematics.

Now can we discuss my plans for a National Community Land Trust, middle-class public housing and achieving nearly-100% recapture on multigenerational wealth through inheritance taxes on estates in excess of $6M?

cui bono

(19,926 posts)Are you saying Chained CPI or nothing and without Chained CPI SS will be terrible?

I don't know if that's your point, but I will say this regardless.

What about raising the caps? What happened to that idea?

dkf

(37,305 posts)Of course if you tell someone to cut this they will say no. But that's not the comparison which is cut these increases or cut the entire amt by 25% later.

Actually chained CPI just postpones the date of the cut. I'm not sure how many more years it gets us.

Blue_In_AK

(46,436 posts)my senator Mark Begich.

http://www.alaskapublic.org/2013/05/02/begich-to-introduce-social-security-legislation/

HereSince1628

(36,063 posts)As inflation impacts the value of money, adjustments to the revenue stream supporting social security must be made.

Robbing people because Congress borrowed and refuses to payback money to the trust fund isn't an adjustment. It's theft by one generation on another.

Why is it that boomers accepted adjustments to support previous generations and their own, and now there is rejection of adjustments?

It probably has a LOT to do with the fact that the only place the adjustments can be made is on the top 5% who don't see themselves as benefiting from the programs.

Such is the politics of letting the rich escape social responsibility of sharing at least 51% of their income.

dkf

(37,305 posts)HereSince1628

(36,063 posts)Failure to do that would be a serious problem.

A general conceptual failure is that most American don't realize the resource type of trust is not a fixed fund, but actually a flowing stream.

The flow's INPUT must be available for adjustment as well as the outflow in order to deal with changes in monetary value, demographic variation, etc.

Thirty years of moving the money of US growth to those above the limits required to pay into the trust have seriously impacted contributions and the appearance of the funds very long term future. That's not an inherent problem with the fund or the philosophical justification for the safety net. It's a consequence of not wanting to change the in coming revenue stream

ucrdem

(15,720 posts)According to the SSA's May 31, 2013 projection, unchanged from the previous year, the trust fund will become "depleted" by 2033, at which point the SSA will continue to pay benefits without it at a rate of 77% of scheduled benefits. This is if Congress does nothing. Link here:

http://www.ssa.gov/pressoffice/pr/trustee13-pr.html

In other words, the entire $2.73 trilion trust fund, which hasn't stopped growing in decades, supposedly vanishes in 20 years, but benefits still go out, relying solely on payroll taxes, which is the pay-as-you-go scheme that was intended to begin with.

My personal preference would be to wait until the trust fund actually shows signs of depletion before doing a damn thing, and I frankly think the chances of it vanishing in two decades are less than zero.

http://www.democraticunderground.com/?com=forum&id=1002

Hoyt

(54,770 posts)ucrdem

(15,720 posts)"Hopelessly" might be more accurate. Can't figure out why Sibelius et al. signed onto it, except possibly out of fear that doing nothing could open the door to pernicious GOP meddling down the road, should we lose the WH, which is possible. I guess you could call it fiduciary hyper-vigilance, but realistic it isn't. Link to a May 31 letter from the SSA trustees to Joe Biden; notice that the retirement fund is fat and happy and it's the disability fund that's having a little trouble:

http://www.socialsecurity.gov/OACT/TR/2013/709letter_TR13_Senate.pdf

p.s. the minute one cent of either fund is privately "invested" we're screwn, that much I'll agree with.

Hoyt

(54,770 posts)

dawg

(10,777 posts)and the cap eliminated. High incomes are not subject to Social Security tax because they do not receive any additional benefit for their contributions. That should not, however, absolve them from continuing to pay their fair share for support of the disabled.

They eliminated the cap for Medicare, they should do the same for disability.

Hoyt

(54,770 posts)that we have other things that 6% needs to go toward. SS is only one of the things that need funding.

jeff47

(26,549 posts)It doesn't require much optimism to realize that their prediction is a tad too pessimistic to require immediate changes.

grantcart

(53,061 posts)Also GDP averages from more than a few years out are meaningless, every 25 years or so the base doubles and it becomes impossible to sustain the early rates.

The average for the last 8 years is about 1.9%.

jeff47

(26,549 posts)They state their assumptions, including GDP growth, mortality rate of Baby Boomers, and so on.

The point of citing a 100-year time span is that it levels out the pits and peaks, leading to a better idea of what "normal" growth is.

As for your stat, the fact that the last 8 years have been almost double their projection, which includes the recession and it's crappy aftermath, is another indication of just how bad their projection is.

grantcart

(53,061 posts)There is no citation. No report.

The SSA Trustees use the actuarial data from the office of the Chief Actuary.

That person uses peer review academically proven numbers and their predictions are right on.

Their projections are based on 1.7% annual growth rate and a 2.0% non farm increase in productivity, exactly matching actual performance.

Rather than imagining what they are talking about you can actually read and cite the exact report

You can find it here page 2 first two paragraphs.

http://www.ssa.gov/oact/tr/2013/2013_Long-Range_Economic_Assumptions.pdf

jeff47

(26,549 posts)but you think I'm the one that's wrong.

grantcart

(53,061 posts)with what I said and you cite a report that 'everyone' is talking about.

The same misinformed talking points were attempted in this thread, but at least that time the person had a graph they cited.

http://www.democraticunderground.com/10023840757

The office of the Chief Actuary, which prepares the report for the trustees, uses the best established economic data that the government has. It is supported by academic peer review. No economist is challenging the data.

These data points are only challenged by those that simply make up statements as they go:

Here are your statements again:

71. The prediction is based on 1% GDP growth. The average for the last 100 years is closer to 3%.

It doesn't require much optimism to realize that their prediction is a tad too pessimistic to require immediate changes.

When asked where you get these nonsensical figures from you state:

110. In the details of the report everyone is citing.

They state their assumptions, including GDP growth, mortality rate of Baby Boomers, and so on.

You have no citation because there isn't any. The report of the Chief Actuary is quite clear, although you have to have some basic understanding of economics to understand it.

I suppose the next source for you made up figures are your girl friends dad's best friend.

Samantha

(9,314 posts)This happened as a result of the agreement struck in 1982 or 1983. It was estimated that when this influx of retirements was completed, the trust fund would have financed that, and the next generations of retirees would happen at a normal level, as opposed to the highly elevated Boomer retirement. Factor in 13 percent of Baby Boomers have already passed away, and that number will only grow over the next few years. So I think it makes more sense, as you have stated, to wait until the trust fund is nearly depleted and to try at that point to guesstimate where we will be in the following few years as to the number of projected retirees accessing the plan.

Sam

ucrdem

(15,720 posts)Somehow the temporary expedient has morphed into the main objective. Funny how that works isn't it? Ronnie also took the opportunity to abolish a healthy survivor's college benefit that I collected for four years, ditto several siblings. Now it's gone, phased out in 1981 and abolished in 1985, although secondary students under age 19 are apparently still eligible. Otherwise benefits end at 18.

winter is coming

(11,785 posts)brush

(61,033 posts)Poster what is your point? You must know a 25% cut will never happen.

randome

(34,845 posts)Raise the FICA cap. Raise corporate taxes. Problem solved.

With the GOP becoming less of an influence in business circles, the time for these kind of reasonable changes is fast approaching.

[hr][font color="blue"][center]You should never stop having childhood dreams.[/center][/font][hr]

closeupready

(29,503 posts)It's an effective, popular program. Make it BETTER.

Hoyt

(54,770 posts)Believe me, I'd love retirement age lowered, coverage expanded, benefits increased, etc. But, it won't work just because we'd love for it to be that way.

We can cut military, that would help. Except there are other things we need to do with that money besides just SS.

jeff47

(26,549 posts)First, you can't make any prediction about "wouldn't cover that" without details like what age retirement would be lowered to. The money required to get it back to 65 is far less than to get it to 50. So no, you can't make claims like the need to tax the top 5% at 100% because you have no idea how much money is required.

Second, cutting military will do absolutely nothing for Social Security. They have completely different sources of revenue.

People have been predicting that Social Security will run out of money in 20 years for about 30 years now. Why, exactly, should we believe this prediction, with it's 1% GDP growth? Growth over the last 100 years has been much higher than that. So what, specifically, cuts growth by 1/3rd? Your pessimism about the current economy?

Hoyt

(54,770 posts)to the days of old.

jeff47

(26,549 posts)So what's your model that says growth will be utterly and completely awful for all of the next 20 years?

Let's take the last 8 years. Terrible economy, right? Recession and a lousy aftermath. 1.9% GDP growth.

The "Social Security is going to run out of money" prediction requires GDP to grow HALF the rate of the last 8 years. And it has to do that for all of the next 20 years.

Oh, and that 3% over 100 years? Includes minor events like the Great Depression. It's not a difficult target to hit.

madrchsod

(58,162 posts)econ 101...every dollar spent on the public good returns 5 dollars. every dollar spent on the military results in either negative or 0 dollars returned for the public good. remember what ike said about the military industrial complex

jeff47

(26,549 posts)Defense comes from the general fund. Social Security comes from dedicated FICA taxes.

Cutting defense reduces spending in the general fund. That doesn't make the savings available to the Social Security fund.

If I cut my home heating spending, that doesn't mean you have more money for gasoline.

ProSense

(116,464 posts)

Marr

(20,317 posts)

I remember when the umm... "centrists" would insist that the White House would never, ever push Chained CPI, and that anyone saying otherwise was a firebagging emotarian paranoid.

Now that it can't be denied any longer, we're hearing about how Sensible© and rational and Pragmatic© it is.

Kolesar

(31,182 posts)Today might be better spent doing something else.

Kolesar

(31,182 posts)Last edited Wed Oct 23, 2013, 08:26 PM - Edit history (1)

For the first few years after age 62, the cuts would be quite small. Then, in succeeding years, the cuts would show up as the compounding effect is starting to occur while one's SS pension "does not grow as fast". One would have to live to 80 or 90 for the cumulative effect to be significant. Most of us will have died by then.

I reckon that when I am in my mid seventies, the cut would be about $1000/year <= 25,000/year * 4%

I read about these cost of living adjustments at the AARP website many months ago.

Here's to a long life for you, dkf!

Warren Stupidity

(48,181 posts)a haircut later.

Everyone advocating cuts in social security and medicare and medicaid and food stamps, everyone of you are reagan democrats.

dawg

(10,777 posts)in the past. I think it would be foolish to accept benefit cuts now because there *might* be a 23% shortfall come 2033.

Furthermore, it makes little sense to make adjustments through COLA's. Once someone is locked into a benefit, forcing them to live on less and less each year is just cruel. If you are going to cut benefits, it would make far more sense to tweak the initial benefit calculation. Then, give honest cost of living increases on the reduced benefit amount. That way, seniors could at least maintain their scaled-back lifestyles. (Not that I am in favor of benefit cuts at all, but it just makes more sense to adjust the initial benefit rather than to lie about the inflation rate.)

Most chained CPI proposals also apply the new rates to income tax brackets, resulting in a stealth tax increase each year - except, of course, for income that was already being taxed at the maximum rate.

Georgia used to have a very progressive income tax. The brackets, however, were never adjusted for inflation, so the maximum rate now applies to tycoons making $20,000 a year.

dkf

(37,305 posts)They've managed to underestimate it if anything.

dawg

(10,777 posts)The trustees have every incentive to be overly pessimistic with their projections. (Here in Georgia, we call it CYA - covering your ass.)

In the early 2030's, the Millennials (a huge population bulge) should be near the peak of their earning power.

Nearly twenty more years of technological change will have transformed our economy in ways that we cannot currently imagine.

I tend to be cautious and incremental about changes to systems that millions of people depend upon. (I won't say 'conservative', because I no longer use that word in any positive or neutral context.) The first step, for me, would be watching and waiting.

If, ten years from now, the trustees are still predicting depletion in 2033, then it would be prudent to consider taking some action. If, however, the projected date of depletion has been pushed forward (as has happened for all of my adult life), then I would continue to call for watching and waiting.

Once we got within a ten year window, and it became apparent that changes really might be necessary, the fist step would be to increase both the wage cap and the countable wages for benefit purposes, so that the same proportion of wages would be covered by the program as was the case in its heyday. This would increase future liabilities as well as raising more revenue, but due to the progressive nature of the bend points within the benefit calculation, it would be a large net positive for the trust fund.

If, after several more years, the life of the trust fund continued to fall below ten years, then adjustments to taxes (and potentially benefits) should be weighed and considered.

It goes without saying that I come down on the "raise taxes rather than cut benefits" side of thing. But there could be some exceptions.

Did you know that once I start collecting Social Security benefits, I could remarry a younger woman, start a new family, and my children would get Social Security checks just like those of a disabled worker? Even if I'm rich as Midas. So there are some things on the benefits side that could probably be changed without placing an undue hardship on the people who really depend on the program.

Regardless, it makes little sense to respond to a potential shortfall by making an insane pact to collectively lie to ourselves about the true rate of inflation.

Vincardog

(20,234 posts)we have been making to the Trust Fund were supposed to be a one time deal right?

Since we Baby boomers were such a LARGE generation there was fear that we would not be followed by a generation large enough to fund our retirements. The fix was that for the first time we were asked to fund our parents and our own retirements.

That is the origin of the Trust Fund. The answer for any shortfall after the Trust Fund is depleted is to INCREASE the numbers of jobs and wages of those jobs paying into SS.

Any answer to this post that does not address these truths will be IMO a simple attempt to troll.

pa28

(6,145 posts)Any further engagement is like arguing with the flat earth society.

Vincardog

(20,234 posts)dkf

(37,305 posts)As that ratio changes what worked in the past does not work in the present and gets worse in the future.

How much should two workers contribute of their income to fund one retiree?

madrchsod

(58,162 posts)but i`m afraid the new free trade agreement will be the final kiss of death for the future social security.

muriel_volestrangler

(106,891 posts)but you can't just pass laws to do that. Whereas you can pass laws to affect the tax rates, other government expenditure, or the benefits paid. Saying "I know how to avoid being poor - be rich instead!" is not that useful.

jeff47

(26,549 posts)For the last 40 years.

I don't think we should cut the program based on this prediction. Especially when it is based on GDP growing at 1% over the intervening 20 years, which is far less than the previous 100 years of growth.

Bluenorthwest

(45,319 posts)in 20 years before the law was passed, this was part of their argument against establishing Social Security. 'It will go broke' has been said since before Social Security existed.

stevenleser

(32,886 posts)Warren DeMontague

(80,708 posts)Not so subtle message being, "Fuck You, Gen X"

trumad

(41,692 posts)Anyone who calls for a cut in SS is a fucking douchebag.

Warren DeMontague

(80,708 posts)No one would notice.

I agree with your sentiment.

dsc

(53,458 posts)let's pay back the money that was stolen from the trust fund. We should increase taxes on the rich and cut defense to the tune of around 200 billion a year for 20 years.

jeff47

(26,549 posts)The trust fund is invested in US bonds. That's the point of having the fund - invest the money in something safe that pays interest. Storing the cash in a giant vault would be really dumb.

So there was no money "stolen" from the trust fund to pay back. All of the money was and is used to buy bonds.

Additionally, cutting defense would do nothing to help the trust fund. Defense and Social Security have separate revenue streams. Any cuts to Defense would do nothing for Social Security.

dsc

(53,458 posts)when the trust fund runs out. IE let SS run a deficit for the 20 years in question.

Social Security is a financially separate entity. Defense spending comes from the General fund. Social Security has it's own, separate financing.

For years we have been counting the surplus in SS to lower the deficit. So we can just do the other way around. Use a general budget surplus to erase or lessen the deficit of SS.

muriel_volestrangler

(106,891 posts)This would not be a constitutional problem - when there was the temporary FICA cut, the general fund was used to make up the shortfall. If you said "we'll make that yearly payment permanent, and cut defense spending to make up for it in the general fund", it would help.

madville

(7,858 posts)The SSDI trust fund will be depleted in 2016 at the current pace. No one is talking about what will happen when that occurs.

The scary part is that the law could allow SSDI to begin drawing from OASDI trust funds. The last projections I saw (from the SSA) if that occurs has ALL trust funds depleted by 2023 and the trend lately has these dates constantly being moved up as it snowballs.

Either some changes are made in the next ten years or we will see at least 25% cuts.

dkf

(37,305 posts)Why is it so hard for them to be straight with people and look for solutions.

ProSense

(116,464 posts)Yikes!

Marr

(20,317 posts)Well, well.

muriel_volestrangler

(106,891 posts)sustainability is the trust funds’ date of exhaustion,

which, under CBO’s extended baseline, would be in

calendar year 2031.13

13. The DI trust fund would be exhausted in fiscal year 2016, and

the OASI trust fund would be exhausted in calendar year 2033.

This document, however, focuses on the combined trust funds.

In 1994, the annual report of the Social Security trustees projected

that the DI trust fund would be exhausted in 1995. That outcome

was prevented by legislation that redirected revenues from the

OASI trust fund to the DI trust fund. Partly because of that experience,

it is a common analytical convention to consider the DI

and OASI trust funds as combined.

http://www.cbo.gov/sites/default/files/cbofiles/attachments/44521-LTBO2013.pdf

99Forever

(14,524 posts)Remove the cap, problem solved.

Why are you on this site? You sound exactly like a Republican.

Kolesar

(31,182 posts)The AARP says it is 0.3%/year. Compounded 18 years, it is only 5.5%

1.003^18 => 1.0055. That is what eighteen years of cuts from age 62 to age 70 would amount to .

http://www.aarp.org/politics-society/advocacy/info-02-2013/the-chained-consumer-price-index-explained.html?intcmp=AE-ENDART1-REL

I have read a lot about retirement planning. If you have any other questions, please ask.

dkf

(37,305 posts)Of benefits. Thus a 25% cut or they could increase payroll taxes significantly and keep growing them year by year.

Kolesar

(31,182 posts)I put up a url . It is not that long of an article. Enjoy

That's the trade off when you consider chained CPI.

http://www.aarp.org/politics-society/advocacy/info-02-2013/the-chained-consumer-price-index-explained.html?intcmp=AE-ENDART1-REL

dkf

(37,305 posts)I'm just reiterating the current projection

Kolesar

(31,182 posts)I thought that was what you were claiming. Hope you have a long life.

dkf

(37,305 posts)It's cold in Georgia right now.

LongTomH

(8,636 posts)That will make Social Security solvent for at least 75 years.

B Calm

(28,762 posts)money on military contractors it would be solvent forever!

Codeine

(25,586 posts)muriel_volestrangler

(106,891 posts)

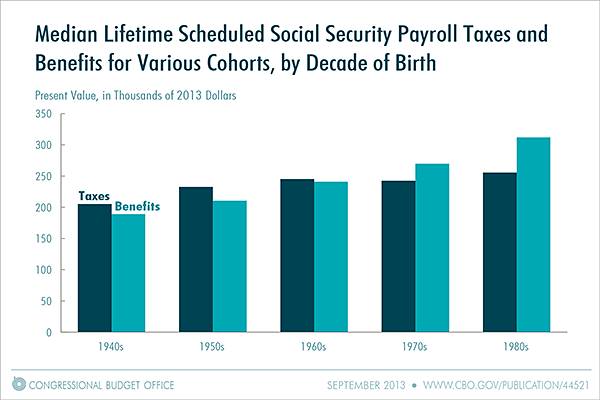

According to CBO’s projections, under the assumption that all scheduled benefits are paid, real median lifetime Social Security benefits and real median lifetime payroll taxes would be greater, in general, for each successive cohort (see the figure below). Over their lifetime, beneficiaries born in the 1940s would, on average, receive about $190,000 in benefits and pay about $205,000 in payroll taxes. Those born in the 1960s would, on average, receive $240,000 in benefits and pay $245,000 in payroll taxes; and those born in the 1980s would, on average, receive $310,000 in benefits and pay $260,000 in payroll taxes. For workers born from the 1940s through the 1980s, taken all together, lifetime payroll taxes would be roughly equal to lifetime benefits. But benefits for earlier generations were considerably larger than their payroll taxes, and that historical imbalance contributes to the system’s ongoing financial shortfall. (Because Social Security benefits are more predictable than Medicare benefits, CBO has extended its projections for Social Security further into the future.)

http://www.cbo.gov/publication/44597

An attempt at 'fairness' might say that the taxes paid by the 1940s cohort are pretty much done, now, and it would be unfair to reduce the benefits they are starting to receive - or the 1950s cohort. What might be better is to gradually decrease the benefits that the cohorts who are still a way from retirement will get, or increase the taxes they pay a bit.

MrsKirkley

(180 posts)

Capt. Obvious

(9,002 posts)Yo_Mama

(8,303 posts)It could defer the date when that occurred by only a few years.

You have to make other major tax changes in order to avoid steep benefit cuts.

Chained CPI also raises income taxes, most acutely on the lower income. There are a lot of things Chained CPI will do, but claiming that they will ensure that SS benefits will be there is just not credible.