Welcome to DU!

The truly grassroots left-of-center political community where regular people, not algorithms, drive the discussions and set the standards.

Join the community:

Create a free account

Support DU (and get rid of ads!):

Become a Star Member

Latest Breaking News

Editorials & Other Articles

General Discussion

The DU Lounge

All Forums

Issue Forums

Culture Forums

Alliance Forums

Region Forums

Support Forums

Help & Search

General Discussion

Related: Editorials & Other Articles, Issue Forums, Alliance Forums, Region Forums"The Chart That Could Save Obamacare"

The Chart That Could Save ObamacareBy David Weigel at Slate

http://www.slate.com/blogs/weigel/2013/10/31/the_chart_that_could_save_obamacare.html

"SNIP...................................

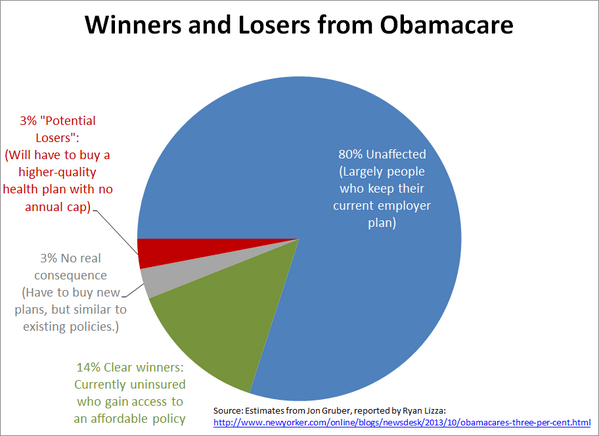

Brookings fellow and critic of snarky Twitter users Justin Wolfers has put together a chart of the people whose coverage under Obamacare will 1) stay the same, 2) get pricier, 3) get cheaper. It's making the rounds around the liberal blogosphere and Twittersphere today, as a sort of coping device for the negative turn against the health care law.

[URL=

.html][IMG]

.html][IMG] [/IMG][/URL]

[/IMG][/URL]

Seems right to me; it so happens that the 6 percent of humans likely to lose their plans and pay more constitute millions of Americans, and that even a small number of them can talk to the media about how horrid the experience is. What they need is a long trench warfare campaign of fact-checking and, occasionally, apologizing. Michael Hiltzik, for example, has reported out the tale of Deborah Cavallaro, a Los Angeles woman spiriting around conservative-leaning shows to explain how Obamacare killed her plan.

Her current plan, from Anthem Blue Cross, is a catastrophic coverage plan for which she pays $293 a month as an individual policyholder. It requires her to pay a deductible of $5,000 a year and limits her out-of-pocket costs to $8,500 a year. Her plan also limits her to two doctor visits a year, for which she shoulders a copay of $40 each. After that, she pays the whole cost of subsequent visits... at her age, she's eligible for a good "silver" plan for $333 a month after the subsidy -- $40 a month more than she's paying now. But the plan is much better than her current plan -- the deductible is $2,000, not $5,000. The maximum out-of-pocket expense is $6,350, not $8,500. Her co-pays would be $45 for a primary care visit and $65 for a specialty visit -- but all visits would be covered, not just two.

Is that better than her current plan? Yes, by a mile

...................................SNIP"

5 replies

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

"The Chart That Could Save Obamacare" (Original Post)

applegrove

Oct 2013

OP

K/R but it doesn't IMO need "saving" except from it's stupid ass critics and the MSM.

NYC_SKP

Oct 2013

#1

About half of the "current employer plans" are changing to comply with ACA regs.

FarCenter

Oct 2013

#2

NYC_SKP

(68,644 posts)1. K/R but it doesn't IMO need "saving" except from it's stupid ass critics and the MSM.

I think it's just fine, but it's getting a beating by the press.

FarCenter

(19,429 posts)2. About half of the "current employer plans" are changing to comply with ACA regs.

They will change coverages, deductibles, networks, prices, etc.

applegrove

(131,121 posts)3. Do you have a link?

doc03

(38,943 posts)4. I don't think it needs "saving" n/t

veganlush

(2,049 posts)5. 80% are winners too

As their policies get much better, for example my college age daughters are covered if necessary until they're 26. Also, limits and caps are gone. Chart drastically underreports winners