Welcome to DU!

The truly grassroots left-of-center political community where regular people, not algorithms, drive the discussions and set the standards.

Join the community:

Create a free account

Support DU (and get rid of ads!):

Become a Star Member

Latest Breaking News

Editorials & Other Articles

General Discussion

The DU Lounge

All Forums

Issue Forums

Culture Forums

Alliance Forums

Region Forums

Support Forums

Help & Search

Environment & Energy

Related: About this forumNREL: The Four Phases of Storage Deployment: A Framework for the Expanding Role of Storage in the U.S. Power System

(Please note, this is a publication of a national research lab. Copyright concerns are nil.)

Storage Futures Study

The Four Phases of Storage Deployment: A Framework for the Expanding Role of Storage in the U.S. Power System (PDF)

…

Preface

This report is one in a series of NREL’s Storage Futures Study (SFS) publications. The SFS is a multiyear research project that explores the role and impact of energy storage in the evolution and operation of the U.S. power sector. The SFS is designed to examine the potential impact of energy storage technology advancement on the deployment of utility-scale storage and the adoption of distributed storage, and the implications for future power system infrastructure investment and operations. The research findings and supporting data will be published as a series of publications. The table on the next page lists the planned publications and specific research topics they will examine under the SFS.

This report, the first in the SFS series, explores the roles and opportunities for new, cost- competitive stationary energy storage with a conceptual framework based on four phases of current and potential future storage deployment, and presents a value proposition for energy storage that could result in substantial new cost-effective deployments. This conceptual framework provides a broader context for consideration of the later reports in the series, including the detailed results of the modeling and analysis of power system evolution scenarios and their operational implications.

The SFS series provides data and analysis in support of the U.S. Department of Energy’s Energy Storage Grand Challenge, a comprehensive program to accelerate the development, commercialization, and utilization of next-generation energy storage technologies and sustain American global leadership in energy storage. The Energy Storage Grand Challenge employs a use case framework to ensure storage technologies can cost-effectively meet specific needs, and it incorporates a broad range of technologies in several categories: electrochemical, electromechanical, thermal, flexible generation, flexible buildings, and power electronics.

More information, any supporting data associated with this report, links to other reports in the series, and other information about the broader study are available at https://www.nrel.gov/analysis/storage-futures.html.

…

Executive Summary

The U.S. electricity system currently has about 24 GW of stationary energy storage with the majority of it being in the form of pumped storage hydropower (PSH). Given changing technologies and market conditions, the deployment expected in the coming decades is likely to include a mix of technologies. Declining costs of energy storage are increasing the likelihood that storage will grow in importance in the U.S. power system. This work uses insights from recent deployment trends, projections, and analyses to develop a framework that characterizes the value proposition of storage as a way to help utilities, regulators, and developers be better prepared for the role storage might play and to understand the need for careful analysis to ensure cost-optimal storage deployment.

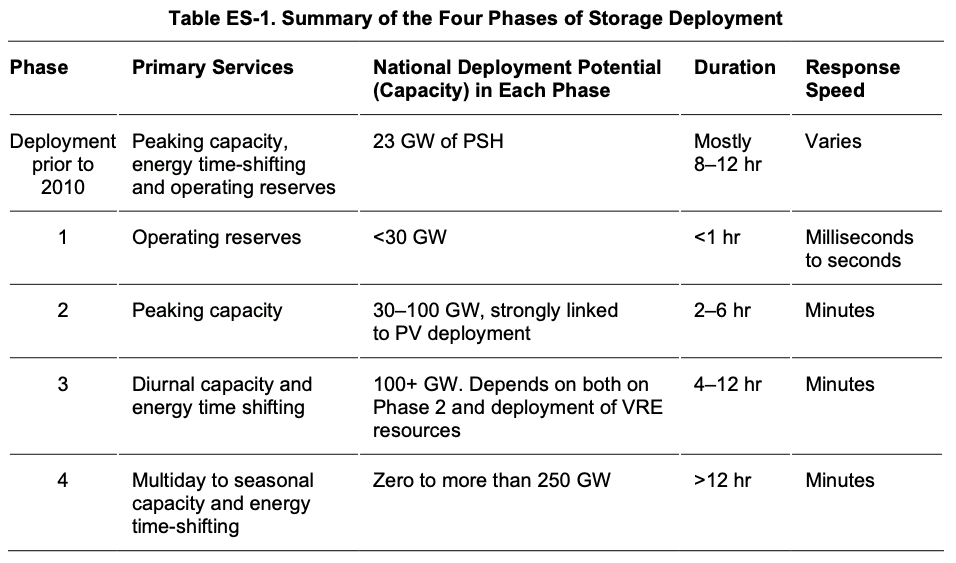

To explore the roles and opportunities for new cost-competitive stationary energy storage, we use a conceptual framework based on four phases of current and potential future storage deployment (see Table ES-1). The four phases, which progress from shorter to longer duration, link the key metric of storage duration to possible future deployment opportunities, considering how the cost and value vary as a function of duration.

The 23 GW of PSH in the United States was built mostly before 1990 to provide peaking capacity and energy time-shifting for large, less flexible capacity. The economics of PSH allowed for deployment with multiple hours of capacity that allowed it to provide multiple grid services. These plants continue to provide valuable grid services that span the four phases framework, and their use has evolved to respond to a changing grid. However, a variety of factors led to a multidecade pause in new development with little storage deployment occurring from about 1990 until 2011.¹

Changing market conditions, such as the introduction of wholesale electricity markets and new technologies suggest storage deployment since 2011 may follow a somewhat different path, diverging from the deployment of exclusively 8+hour PSH. Instead, more recent deployment of storage has largely begun with shorter-duration storage, and we anticipate that new storage deployment will follow a trend of increasing durations.

We characterize this trend in our four phases framework, which captures how both the cost and value of storage changes as a function of duration. Many storage technologies have a significant cost associated with increasing the duration, or actual energy stored per unit of power capacity. In contrast, the value of most grid services does not necessarily increase with increasing asset duration—it may have no increase in value beyond a certain duration, or its value may increase at a rapidly diminishing rate. As a result, the economic performance of most storage technologies will rapidly decline beyond a certain duration. In current U.S. electricity markets, the value of many grid services can be captured by discrete and relatively short-duration storage (such as less than 1 hour for most operating reserves or 4 hours for capacity).

Together, the increasing cost of storage with duration and the lack of incremental value with increasing storage duration will likely contribute to growth of storage in the U.S. power sector that is characterized by a progression of deployments that aligns duration with specific services and storage technologies.

The four phases conceptual framework introduced in this work is a simplification of a more complicated evolution of the stationary energy storage industry and the power system as a whole. While we present four distinct phases, the boundaries between each phase will be somewhat indistinct and transitions between phases will occur at different times in different regions as various markets for specific services are saturated, and phases can overlap within a region. These transitions and the total market sizes are strongly influenced by the regional deployment of variable renewable energy (VRE) as well as hybrid deployments. However, we believe it is a useful framework to consider the role of different storage technologies, and particularly the importance of duration in driving adoption in each phase.

Phase 1, which began around 2011, is characterized by the deployment of storage with 1-hour or shorter duration, and it resulted from the emergence of restructured markets and new technologies that allow for cost-competitive provision of operating reserves, including regulating reserves. Potential deployment of short-duration storage in Phase 1 is bounded by the overall requirements for operating reserves, which is less than 30 GW in the United States even when including regulating reserves, spinning contingency reserves, and frequency responsive reserves, some of which are not yet a widely compensated service.

Phase 2 is characterized by the deployment of storage with 2–6 hours of discharge duration to serve as peaking capacity. Phase 2 has begun in some regions, with lithium-ion batteries becoming cost-competitive where durations of 2–6 hours are sufficient to provide reliable peaking capacity. As prices continue to fall, batteries are expected to become cost-competitive in more locations. These storage assets derive much of their value from the replacement of traditional peaking resources, (primarily natural gas-fired combustion turbines), but they also take value from time-shifting/energy arbitrage of energy supply. The potential opportunities of Phase 2 are limited by the local or regional length of the peak demand period and have a lower bound of about 40 GW. However, the length of peak demand is highly affected by the deployment of VRE, specifically solar photovoltaics (PV), which narrows the peak demand period. Phase 2 is characterized in part by the positive feedback between PV increasing the value of storage (increasing its ability to provide capacity) and storage increasing the value of PV (increasing its energy value by shifting it output to periods of greater demand). Thus, greater deployment of solar PV could extend the storage potential of Phase 2 to more than 100 GW in the United States in scenarios where 25% of the nation’s electricity is derived from solar.

Phase 3 is less distinct, but is characterized by lower costs and technology improvements that enable storage to be cost-competitive while serving longer-duration (4–12 hour) peaks. These longer net load peaks can result from the addition of substantial 2–6 hour storage deployed in Phase 2. Deployment in Phase 3 could include a variety of new technologies and could also see a reemergence of pumped storage, taking advantage of new technologies that reduce costs and siting constraints while exploiting the 8+ hour durations typical of many pumped storage facilities. The technology options for Phase 3 include next-generation compressed air and various thermal or mechanical-based storage technologies. Also, storage in this phase might provide additional sources of value, such as transmission deferral and additional time-shifting of solar and wind generation to address diurnal mismatches of supply and demand. Our scenario analysis identified 100 GW or more of potential opportunities for Phase 3 in the United States, in addition to the existing PSH that provides valuable capacity in several regions. Of note for both Phase 2 and 3 is a likely mix of configurations, with some stand-alone storage, but also a potentially significant fraction of storage deployments associated with hybrid plants, where storage can take advantage of tax credits, or shared capital and operating expenses. As in Phase 2, additional VRE, especially solar PV, could extend the storage potential of Phase 3, enabling contributions of VRE exceeding 50% on an annual basis.

Phase 4 is the most uncertain of our phases. It characterizes a possible future in which storage with durations from days to months is used to achieve very high levels of renewable energy (RE) in the power sector, or as part of multisector decarbonization. Technologies options in this space include production of liquid and gas fuels, which can be stored in large underground formations that enable extremely long-duration storage with very low loss rates. This low loss rate allows for seasonal shifting of RE supply, and generation of a carbon-free fuel for industrial processes and feedstocks. Phase 4 technologies are generally characterized by high power-related costs associated with fuel production and use but with very low duration-related costs. Thus, traditional metrics such as cost per kilowatt-hour of storage capacity are less useful, and when combined with the potential use of fuels for non-electric sector applications, makes comparison of Phase 4 technologies with other storage technologies more difficult. The potential opportunities for Phase 4 technologies measure in the hundreds of gigawatts in the United States, and these technologies could potentially address the residual demand that is very difficult or expensive to meet with RE resources and storage deployed in Phases 1–3.

Our four phases framework is intended to describe a plausible evolution of cost-competitive storage technologies, but more importantly, it identifies key elements needed for stakeholders to evaluate alternative pathways for both storage and other sources of system flexibility. Specifically, an improved characterization of various grid services needed, including capacity and duration, could help provide a deeper understanding of the tradeoffs between various technologies, and non-storage resources such as responsive demand. Such a characterization would help ensure the mix of flexibility technologies deployed is robust to an evolving a grid, which will ultimately determine the amount of storage and flexibility the power system will need.

…

This is just the introduction. For more substantial information, follow the link. My goal here is to make clear the different “phases” of energy storage which will be required on a renewable grid.

Preface

This report is one in a series of NREL’s Storage Futures Study (SFS) publications. The SFS is a multiyear research project that explores the role and impact of energy storage in the evolution and operation of the U.S. power sector. The SFS is designed to examine the potential impact of energy storage technology advancement on the deployment of utility-scale storage and the adoption of distributed storage, and the implications for future power system infrastructure investment and operations. The research findings and supporting data will be published as a series of publications. The table on the next page lists the planned publications and specific research topics they will examine under the SFS.

This report, the first in the SFS series, explores the roles and opportunities for new, cost- competitive stationary energy storage with a conceptual framework based on four phases of current and potential future storage deployment, and presents a value proposition for energy storage that could result in substantial new cost-effective deployments. This conceptual framework provides a broader context for consideration of the later reports in the series, including the detailed results of the modeling and analysis of power system evolution scenarios and their operational implications.

The SFS series provides data and analysis in support of the U.S. Department of Energy’s Energy Storage Grand Challenge, a comprehensive program to accelerate the development, commercialization, and utilization of next-generation energy storage technologies and sustain American global leadership in energy storage. The Energy Storage Grand Challenge employs a use case framework to ensure storage technologies can cost-effectively meet specific needs, and it incorporates a broad range of technologies in several categories: electrochemical, electromechanical, thermal, flexible generation, flexible buildings, and power electronics.

More information, any supporting data associated with this report, links to other reports in the series, and other information about the broader study are available at https://www.nrel.gov/analysis/storage-futures.html.

…

Executive Summary

The U.S. electricity system currently has about 24 GW of stationary energy storage with the majority of it being in the form of pumped storage hydropower (PSH). Given changing technologies and market conditions, the deployment expected in the coming decades is likely to include a mix of technologies. Declining costs of energy storage are increasing the likelihood that storage will grow in importance in the U.S. power system. This work uses insights from recent deployment trends, projections, and analyses to develop a framework that characterizes the value proposition of storage as a way to help utilities, regulators, and developers be better prepared for the role storage might play and to understand the need for careful analysis to ensure cost-optimal storage deployment.

To explore the roles and opportunities for new cost-competitive stationary energy storage, we use a conceptual framework based on four phases of current and potential future storage deployment (see Table ES-1). The four phases, which progress from shorter to longer duration, link the key metric of storage duration to possible future deployment opportunities, considering how the cost and value vary as a function of duration.

The 23 GW of PSH in the United States was built mostly before 1990 to provide peaking capacity and energy time-shifting for large, less flexible capacity. The economics of PSH allowed for deployment with multiple hours of capacity that allowed it to provide multiple grid services. These plants continue to provide valuable grid services that span the four phases framework, and their use has evolved to respond to a changing grid. However, a variety of factors led to a multidecade pause in new development with little storage deployment occurring from about 1990 until 2011.¹

Changing market conditions, such as the introduction of wholesale electricity markets and new technologies suggest storage deployment since 2011 may follow a somewhat different path, diverging from the deployment of exclusively 8+hour PSH. Instead, more recent deployment of storage has largely begun with shorter-duration storage, and we anticipate that new storage deployment will follow a trend of increasing durations.

We characterize this trend in our four phases framework, which captures how both the cost and value of storage changes as a function of duration. Many storage technologies have a significant cost associated with increasing the duration, or actual energy stored per unit of power capacity. In contrast, the value of most grid services does not necessarily increase with increasing asset duration—it may have no increase in value beyond a certain duration, or its value may increase at a rapidly diminishing rate. As a result, the economic performance of most storage technologies will rapidly decline beyond a certain duration. In current U.S. electricity markets, the value of many grid services can be captured by discrete and relatively short-duration storage (such as less than 1 hour for most operating reserves or 4 hours for capacity).

Together, the increasing cost of storage with duration and the lack of incremental value with increasing storage duration will likely contribute to growth of storage in the U.S. power sector that is characterized by a progression of deployments that aligns duration with specific services and storage technologies.

The four phases conceptual framework introduced in this work is a simplification of a more complicated evolution of the stationary energy storage industry and the power system as a whole. While we present four distinct phases, the boundaries between each phase will be somewhat indistinct and transitions between phases will occur at different times in different regions as various markets for specific services are saturated, and phases can overlap within a region. These transitions and the total market sizes are strongly influenced by the regional deployment of variable renewable energy (VRE) as well as hybrid deployments. However, we believe it is a useful framework to consider the role of different storage technologies, and particularly the importance of duration in driving adoption in each phase.

Phase 1, which began around 2011, is characterized by the deployment of storage with 1-hour or shorter duration, and it resulted from the emergence of restructured markets and new technologies that allow for cost-competitive provision of operating reserves, including regulating reserves. Potential deployment of short-duration storage in Phase 1 is bounded by the overall requirements for operating reserves, which is less than 30 GW in the United States even when including regulating reserves, spinning contingency reserves, and frequency responsive reserves, some of which are not yet a widely compensated service.

Phase 2 is characterized by the deployment of storage with 2–6 hours of discharge duration to serve as peaking capacity. Phase 2 has begun in some regions, with lithium-ion batteries becoming cost-competitive where durations of 2–6 hours are sufficient to provide reliable peaking capacity. As prices continue to fall, batteries are expected to become cost-competitive in more locations. These storage assets derive much of their value from the replacement of traditional peaking resources, (primarily natural gas-fired combustion turbines), but they also take value from time-shifting/energy arbitrage of energy supply. The potential opportunities of Phase 2 are limited by the local or regional length of the peak demand period and have a lower bound of about 40 GW. However, the length of peak demand is highly affected by the deployment of VRE, specifically solar photovoltaics (PV), which narrows the peak demand period. Phase 2 is characterized in part by the positive feedback between PV increasing the value of storage (increasing its ability to provide capacity) and storage increasing the value of PV (increasing its energy value by shifting it output to periods of greater demand). Thus, greater deployment of solar PV could extend the storage potential of Phase 2 to more than 100 GW in the United States in scenarios where 25% of the nation’s electricity is derived from solar.

Phase 3 is less distinct, but is characterized by lower costs and technology improvements that enable storage to be cost-competitive while serving longer-duration (4–12 hour) peaks. These longer net load peaks can result from the addition of substantial 2–6 hour storage deployed in Phase 2. Deployment in Phase 3 could include a variety of new technologies and could also see a reemergence of pumped storage, taking advantage of new technologies that reduce costs and siting constraints while exploiting the 8+ hour durations typical of many pumped storage facilities. The technology options for Phase 3 include next-generation compressed air and various thermal or mechanical-based storage technologies. Also, storage in this phase might provide additional sources of value, such as transmission deferral and additional time-shifting of solar and wind generation to address diurnal mismatches of supply and demand. Our scenario analysis identified 100 GW or more of potential opportunities for Phase 3 in the United States, in addition to the existing PSH that provides valuable capacity in several regions. Of note for both Phase 2 and 3 is a likely mix of configurations, with some stand-alone storage, but also a potentially significant fraction of storage deployments associated with hybrid plants, where storage can take advantage of tax credits, or shared capital and operating expenses. As in Phase 2, additional VRE, especially solar PV, could extend the storage potential of Phase 3, enabling contributions of VRE exceeding 50% on an annual basis.

Phase 4 is the most uncertain of our phases. It characterizes a possible future in which storage with durations from days to months is used to achieve very high levels of renewable energy (RE) in the power sector, or as part of multisector decarbonization. Technologies options in this space include production of liquid and gas fuels, which can be stored in large underground formations that enable extremely long-duration storage with very low loss rates. This low loss rate allows for seasonal shifting of RE supply, and generation of a carbon-free fuel for industrial processes and feedstocks. Phase 4 technologies are generally characterized by high power-related costs associated with fuel production and use but with very low duration-related costs. Thus, traditional metrics such as cost per kilowatt-hour of storage capacity are less useful, and when combined with the potential use of fuels for non-electric sector applications, makes comparison of Phase 4 technologies with other storage technologies more difficult. The potential opportunities for Phase 4 technologies measure in the hundreds of gigawatts in the United States, and these technologies could potentially address the residual demand that is very difficult or expensive to meet with RE resources and storage deployed in Phases 1–3.

Our four phases framework is intended to describe a plausible evolution of cost-competitive storage technologies, but more importantly, it identifies key elements needed for stakeholders to evaluate alternative pathways for both storage and other sources of system flexibility. Specifically, an improved characterization of various grid services needed, including capacity and duration, could help provide a deeper understanding of the tradeoffs between various technologies, and non-storage resources such as responsive demand. Such a characterization would help ensure the mix of flexibility technologies deployed is robust to an evolving a grid, which will ultimately determine the amount of storage and flexibility the power system will need.

…