Welcome to DU!

The truly grassroots left-of-center political community where regular people, not algorithms, drive the discussions and set the standards.

Join the community:

Create a free account

Support DU (and get rid of ads!):

Become a Star Member

Latest Breaking News

Editorials & Other Articles

General Discussion

The DU Lounge

All Forums

Issue Forums

Culture Forums

Alliance Forums

Region Forums

Support Forums

Help & Search

Economy

In reply to the discussion: Weekend Economists Sit on a Wall August 23-25, 2013 [View all]Demeter

(85,373 posts)24. Austerity Claims Victory in Europe YVES SMITH NAKED CAPITALISM

http://www.nakedcapitalism.com/2013/08/austerity-claims-victory-in-europe.html?utm_source=feedburner&utm_medium=email&utm_campaign=Feed%3A+NakedCapitalism+%28naked+capitalism%29

Yves here. Even though Delusional Economics has moved into a guardedly positive stance on Europe, the “recovery” is halting enough in Europe that there are still quite a few analysts on the other side of the fence. Wolf Richter has an engagingly-written post on how unmitigatedly awful conditions are in hotels and restaurants are in France. And Ambrose Evans-Pritchard was kind enough to ping last week and express his considerable skepticism about the chattering about “recovery” in the periphery. Nominal GDPs are still falling, which means debt levels are still rising. And don’t get him started on the Draghi Put!

....................................................................................................................

By Delusional Economics, who is determined to cleanse the daily flow of vested interests propaganda to produce a balanced counterpoint. Cross posted from MacroBusiness

Another night of relatively strong data out of Eurozone with services and composite PMIs looking mostly stronger, the UK also screamed ahead.

Eurozone economy stabilises as German recovery accelerates and downturns ease in France, Italy and Spain

• Final Eurozone Composite Output Index: 50.5 (Flash 50.4, June 48.7)

• Final Eurozone Services Business Activity Index: 49.8. (Flash 49.6, June 48.3)

• German recovery gains momentum while downturns in France, Italy and Spain ease further

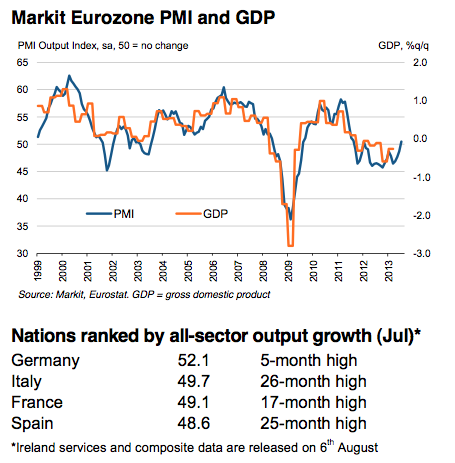

July marked a tentative return to expansion for the eurozone economy, as manufacturing output posted a solid expansion and the trend in services activity moved close to stabilisation. At 50.5 in July, the final Markit Eurozone PMI® Composite Output Index rose to a near two-year high and posted above the neutral 50.0 mark for the first time since January 2012. The headline index was marginally above its flash reading of 50.4.

Manufacturing production rose at the fastest pace since June 2011, as the sector registered output growth for the first time in 17 months. Meanwhile, the rate of contraction in services business activity was negligible and the weakest during the current one-and-a-half year downturn in the sector.

Among the big-four nations, growth was led by Germany, where rates of increase in manufacturing output and service sector activity hit 17- and five-month highs respectively. France, Italy and Spain meanwhile saw overall rates of contraction ease further.

France and Italy both moved close to stabilisation, Source: Markit, Eurostat. GDP gross domestic product as solid growth at manufacturers largely offset slower declines at service providers. Spain saw output decline in both sectors.

So as we’ve seen over the last month or two the news out of the Eurozone is slowly getting better and it’s definitely great to see that even the Italians have managed to slow the rate of decline, although contraction is still evident, as it is in Spain. It must be noted however, as I spoke about last week, this is all taking place in an environment in which periphery debt to GDP continues to grow. That is, the government sector is still providing an offsetting deficit that allows this private sector adjustment to take place in the absence of large enough external demand. Re-balancing is taking place, but there is still a very long way to go with this adjustment, as can be clearly seen from the rate of unemployment in many of these countries. There is a problem, however, and that is that many of these nations are reaching a point where debt to GDP once again becomes a concern. What is needed, and we are likely to see from in Greece in the near future, is a further write-down of debts before we can truly say there is a sustainable recovery taking place.

That reality, however, hasn’t stopped some “interesting” reporting on the matter:

Can a program of austerity and structural overhauls extricate an economy from a debt crisis? Is it really possible for a country to achieve a so-called internal devaluation—restoring its competitiveness by cutting wages and boosting productivity rather than lowering its external exchange rate? Are European democracies capable of confronting vested interests and coping with the resulting social upheaval?

Until now, the small group of believers—mostly to be found in Berlin—have been widely dismissed as freaks or sadists. The conventional wisdom argued that the only possible escape for countries like Spain was a large-scale mutualization of euro-zone sovereign debt or to quit the single currency.

The government of Mariano Rajoy has, however—through necessity as much as conviction—set out to prove them wrong.

…

What is certain is that the stakes couldn’t be higher—for Spain and the euro zone: A self-sustaining recovery would remove one of the biggest threats to the survival of the single currency.

No less importantly, it would vindicate Berlin’s approach to handling the crisis and send a powerful message to other governments tempted to look to debt mutualization as an easy alternative to the hard business of reform.

I genuinely hope that isn’t the actual position of the “small group of believers” and this is just journalistic silliness. I mean seriously, you don’t have to look very far to find evidence of the massive destructive social implications these programs had on the future of Spain. A recent story from the BBC for example:

And it’s not like those supposedly able to claim vindication weren’t complicit in exacerbating these long term issues, in fact they were running domestic programs to exploit these exact problems: MORE

Yves here. Even though Delusional Economics has moved into a guardedly positive stance on Europe, the “recovery” is halting enough in Europe that there are still quite a few analysts on the other side of the fence. Wolf Richter has an engagingly-written post on how unmitigatedly awful conditions are in hotels and restaurants are in France. And Ambrose Evans-Pritchard was kind enough to ping last week and express his considerable skepticism about the chattering about “recovery” in the periphery. Nominal GDPs are still falling, which means debt levels are still rising. And don’t get him started on the Draghi Put!

....................................................................................................................

By Delusional Economics, who is determined to cleanse the daily flow of vested interests propaganda to produce a balanced counterpoint. Cross posted from MacroBusiness

Another night of relatively strong data out of Eurozone with services and composite PMIs looking mostly stronger, the UK also screamed ahead.

Eurozone economy stabilises as German recovery accelerates and downturns ease in France, Italy and Spain

• Final Eurozone Composite Output Index: 50.5 (Flash 50.4, June 48.7)

• Final Eurozone Services Business Activity Index: 49.8. (Flash 49.6, June 48.3)

• German recovery gains momentum while downturns in France, Italy and Spain ease further

July marked a tentative return to expansion for the eurozone economy, as manufacturing output posted a solid expansion and the trend in services activity moved close to stabilisation. At 50.5 in July, the final Markit Eurozone PMI® Composite Output Index rose to a near two-year high and posted above the neutral 50.0 mark for the first time since January 2012. The headline index was marginally above its flash reading of 50.4.

Manufacturing production rose at the fastest pace since June 2011, as the sector registered output growth for the first time in 17 months. Meanwhile, the rate of contraction in services business activity was negligible and the weakest during the current one-and-a-half year downturn in the sector.

Among the big-four nations, growth was led by Germany, where rates of increase in manufacturing output and service sector activity hit 17- and five-month highs respectively. France, Italy and Spain meanwhile saw overall rates of contraction ease further.

France and Italy both moved close to stabilisation, Source: Markit, Eurostat. GDP gross domestic product as solid growth at manufacturers largely offset slower declines at service providers. Spain saw output decline in both sectors.

So as we’ve seen over the last month or two the news out of the Eurozone is slowly getting better and it’s definitely great to see that even the Italians have managed to slow the rate of decline, although contraction is still evident, as it is in Spain. It must be noted however, as I spoke about last week, this is all taking place in an environment in which periphery debt to GDP continues to grow. That is, the government sector is still providing an offsetting deficit that allows this private sector adjustment to take place in the absence of large enough external demand. Re-balancing is taking place, but there is still a very long way to go with this adjustment, as can be clearly seen from the rate of unemployment in many of these countries. There is a problem, however, and that is that many of these nations are reaching a point where debt to GDP once again becomes a concern. What is needed, and we are likely to see from in Greece in the near future, is a further write-down of debts before we can truly say there is a sustainable recovery taking place.

That reality, however, hasn’t stopped some “interesting” reporting on the matter:

Can a program of austerity and structural overhauls extricate an economy from a debt crisis? Is it really possible for a country to achieve a so-called internal devaluation—restoring its competitiveness by cutting wages and boosting productivity rather than lowering its external exchange rate? Are European democracies capable of confronting vested interests and coping with the resulting social upheaval?

Until now, the small group of believers—mostly to be found in Berlin—have been widely dismissed as freaks or sadists. The conventional wisdom argued that the only possible escape for countries like Spain was a large-scale mutualization of euro-zone sovereign debt or to quit the single currency.

The government of Mariano Rajoy has, however—through necessity as much as conviction—set out to prove them wrong.

…

What is certain is that the stakes couldn’t be higher—for Spain and the euro zone: A self-sustaining recovery would remove one of the biggest threats to the survival of the single currency.

No less importantly, it would vindicate Berlin’s approach to handling the crisis and send a powerful message to other governments tempted to look to debt mutualization as an easy alternative to the hard business of reform.

I genuinely hope that isn’t the actual position of the “small group of believers” and this is just journalistic silliness. I mean seriously, you don’t have to look very far to find evidence of the massive destructive social implications these programs had on the future of Spain. A recent story from the BBC for example:

Scientists in Spain claim the long-term future of the country is being sacrificed, because of what they call “short-sighted” austerity measures.

Research and development in Spain has been cut by around 40% in the past five years. The Spanish government says the private sector needs to do more, but many scientists are simply leaving Spain and taking their work abroad.

Research and development in Spain has been cut by around 40% in the past five years. The Spanish government says the private sector needs to do more, but many scientists are simply leaving Spain and taking their work abroad.

And it’s not like those supposedly able to claim vindication weren’t complicit in exacerbating these long term issues, in fact they were running domestic programs to exploit these exact problems: MORE

Edit history

Please sign in to view edit histories.

Recommendations

0 members have recommended this reply (displayed in chronological order):

70 replies

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

RecommendedHighlight replies with 5 or more recommendations

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

RecommendedHighlight replies with 5 or more recommendations

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

RecommendedHighlight replies with 5 or more recommendations

Cyprus Bank�s Bailout Hands Ownership to Russian Plutocrats THAT WORKED WELL, DIDN'T IT?

Demeter

Aug 2013

#2

Feds building detective squad to target consumers and companies that don't follow Obamacare's rules

Demeter

Aug 2013

#4

Detroit Institute of Art Collection--Available to Creditors? by Adam Levitin SUCKING EGGS

Demeter

Aug 2013

#13

Argentina Just Lost Huge To A Bunch Of Hedge Fund Creditors, And The Judge Was Brutal About It

xchrom

Aug 2013

#23

Room For Hope? Fourth Largest Industry In France: It�s �Never Been This Catastrophic�

Demeter

Aug 2013

#26

Official White House Response to We request that Obama be impeached for the following reasons.

Demeter

Aug 2013

#29

The Trans-Pacific Partnership is not about free trade. It's a corporate coup d'etat--against us!

Demeter

Aug 2013

#34

Peter Van Buren: Bradley Manning, Surveillance State Creep, Emergence of Post-Constitutional America

Demeter

Aug 2013

#37