Welcome to DU!

The truly grassroots left-of-center political community where regular people, not algorithms, drive the discussions and set the standards.

Join the community:

Create a free account

Support DU (and get rid of ads!):

Become a Star Member

Latest Breaking News

Editorials & Other Articles

General Discussion

The DU Lounge

All Forums

Issue Forums

Culture Forums

Alliance Forums

Region Forums

Support Forums

Help & Search

Economy

In reply to the discussion: Weekend Economists Clean Out Davy Jones' Locker, March 2-4, 2012 [View all]Demeter

(85,373 posts)7. The global zombie shuffles on

http://www.macrobusiness.com.au/2012/03/the-global-zombie-shuffles-on/

My theory for global growth this year is that it will slow from last year and any acceleration will be difficult and halting. That’s because Europe has set course for perpetual recession via austerity and a credit crunch, the US looks headed for a slowdown on lousy income growth and China is going to have its version of a balance sheet shakeout as it suppresses house prices. As such I’ve been looking for signs of weak rebounds in the PMIs. And I’ve found them.

We know of China’s and Japan’s manufacturing zombies, as well as the slowdown in growth in last night’s US ISM. Now today we can add the export bell weathers of South Korea and Taiwan. First to the ROK:

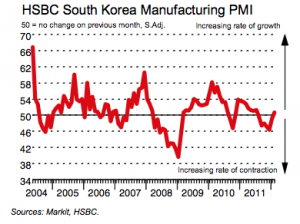

Business conditions in the South Korean manufacturing sector improved for the first time since July 2011 during February. This was highlighted by the HSBC South Korea Manufacturing PMI® posting 50.7, up from January’s reading of 49.2. Nonetheless, the latest figure pointed to only a marginal rate of growth.

South Korean manufacturers reported an increase in new business received during February, ending a six-month sequence of contraction. Nonetheless, the expansion was only marginal. Similarly, new export orders increased, but only slightly. Panellists commented that ongoing fragile economic conditions and strong competition for new business had limited the extent to which overall new work intakes increased.

So, a fairly subdued bounce. Meanwhile, in Taiwan the news was similar with a bit more upside:

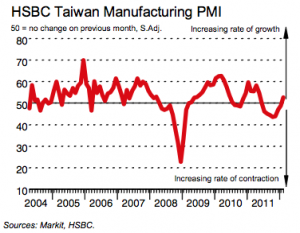

The HSBC Taiwan PMI™ – a composite indicator designed to provide a single-figure snap-shot of the health of the manufacturing sector – posted 52.7 in February, up from 48.9 in January, and signalled modest growth of the sector. Furthermore, the expansion ended an eight-month period of deteriorating operating conditions.

Manufacturers in Taiwan reported a rise in new business during February, the first such increase since May 2011. Increasing almost seven points, the seasonally adjusted New Orders Index pointed to solid growth of new work intakes. Similarly, an expansion of new export business was also registered. Panellists commented that increased demand, both at home and overseas, had contributed to the rise in overall new orders. Export markets particularly noted to have shown an improvement were China, Europe and the US.

Finally, now we’ve done the rounds of the global PMIs once more, we can look at the J.P.Morgan Global PMI:

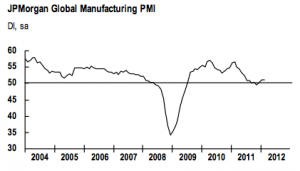

The JPMorgan Global Manufacturing PMI™ broadly held its ground at 51.1 in February, little-changed from 51.3 in January, to signal an improvement in operating conditions for the third straight month. Levels of output, new orders and employment all moved higher.

So, as you can see, not going anywhere fast and a glance at the internals is no more encouraging with forward pointing indicators weaker than headline:

We’ve averted a banking crisis in the US, more recently one in Europe, and probably one in China right now. My guess is we’ll now pay with slow growth. Everywhere.

My theory for global growth this year is that it will slow from last year and any acceleration will be difficult and halting. That’s because Europe has set course for perpetual recession via austerity and a credit crunch, the US looks headed for a slowdown on lousy income growth and China is going to have its version of a balance sheet shakeout as it suppresses house prices. As such I’ve been looking for signs of weak rebounds in the PMIs. And I’ve found them.

We know of China’s and Japan’s manufacturing zombies, as well as the slowdown in growth in last night’s US ISM. Now today we can add the export bell weathers of South Korea and Taiwan. First to the ROK:

Business conditions in the South Korean manufacturing sector improved for the first time since July 2011 during February. This was highlighted by the HSBC South Korea Manufacturing PMI® posting 50.7, up from January’s reading of 49.2. Nonetheless, the latest figure pointed to only a marginal rate of growth.

South Korean manufacturers reported an increase in new business received during February, ending a six-month sequence of contraction. Nonetheless, the expansion was only marginal. Similarly, new export orders increased, but only slightly. Panellists commented that ongoing fragile economic conditions and strong competition for new business had limited the extent to which overall new work intakes increased.

So, a fairly subdued bounce. Meanwhile, in Taiwan the news was similar with a bit more upside:

The HSBC Taiwan PMI™ – a composite indicator designed to provide a single-figure snap-shot of the health of the manufacturing sector – posted 52.7 in February, up from 48.9 in January, and signalled modest growth of the sector. Furthermore, the expansion ended an eight-month period of deteriorating operating conditions.

Manufacturers in Taiwan reported a rise in new business during February, the first such increase since May 2011. Increasing almost seven points, the seasonally adjusted New Orders Index pointed to solid growth of new work intakes. Similarly, an expansion of new export business was also registered. Panellists commented that increased demand, both at home and overseas, had contributed to the rise in overall new orders. Export markets particularly noted to have shown an improvement were China, Europe and the US.

Finally, now we’ve done the rounds of the global PMIs once more, we can look at the J.P.Morgan Global PMI:

The JPMorgan Global Manufacturing PMI™ broadly held its ground at 51.1 in February, little-changed from 51.3 in January, to signal an improvement in operating conditions for the third straight month. Levels of output, new orders and employment all moved higher.

So, as you can see, not going anywhere fast and a glance at the internals is no more encouraging with forward pointing indicators weaker than headline:

We’ve averted a banking crisis in the US, more recently one in Europe, and probably one in China right now. My guess is we’ll now pay with slow growth. Everywhere.

Edit history

Please sign in to view edit histories.

Recommendations

0 members have recommended this reply (displayed in chronological order):

66 replies

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

RecommendedHighlight replies with 5 or more recommendations

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

RecommendedHighlight replies with 5 or more recommendations

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

RecommendedHighlight replies with 5 or more recommendations

ART CASHIN: We May Have Just Witnessed The Presence Of Artificial Intelligence In The Stock Market

Demeter

Mar 2012

#14

Matt Stoller: Wall Street Fixer Rodge Cohen � Big Banks Key to American Global Dominance

Demeter

Mar 2012

#20

Michael Hudson: 2,181 Italians Pack a Sports Arena to Learn Modern Monetary Theory � The Economy

Demeter

Mar 2012

#21

that was a relly nice rain we had last night. how do i know? cause i've been awake since 2:15.

xchrom

Mar 2012

#30

Adrian Hamilton: Is there really no alternative? Let Irish voters be the judge of that

xchrom

Mar 2012

#31

And those who live together without benefit (?) of marriage have their reasons,

Tansy_Gold

Mar 2012

#54

Spain defies Brussels by granting itself the leeway it was denied on the deficit

xchrom

Mar 2012

#46

glad every one in your family is ok -- i'm sure it was scary for your daughter. nt

xchrom

Mar 2012

#41