Welcome to DU!

The truly grassroots left-of-center political community where regular people, not algorithms, drive the discussions and set the standards.

Join the community:

Create a free account

Support DU (and get rid of ads!):

Become a Star Member

Latest Breaking News

Editorials & Other Articles

General Discussion

The DU Lounge

All Forums

Issue Forums

Culture Forums

Alliance Forums

Region Forums

Support Forums

Help & Search

Democratic Primaries

Showing Original Post only (View all)Americans' Health-Care Costs Are Too Damn High, Study Finds [View all]

...the primary obstacle to rebuilding our ramshackle health-care system is the immense power of the industries and interest groups that have monetized its rot. But historically, public opinion has posed its own discrete challenges. Voters often display a strong sense of loss aversion, valuing the preservation of what they have over the uncertain promise of something better. And in the domain of health care — where the stakes of losing what one has (if one is privileged enough to have coverage in the general vicinity of “affordable”) are potentially life and death — this tendency has been especially acute.

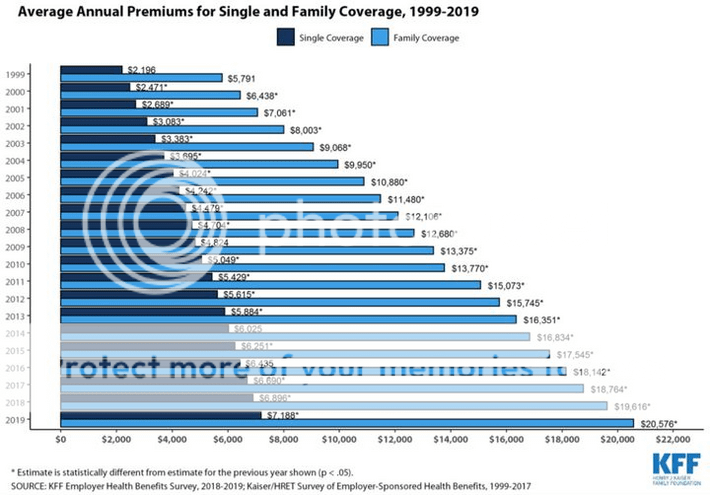

...For these reasons, a lot of health-care punditry presumes that the public’s appetite for Medicare for All — or even a Medicare buy-in — will swiftly decline once Democrats have the opportunity to actually implement it. And that scenario remains plausible. But there’s increasing reason to believe that “next time will be different” — because with each passing year, those loss-averse voters with employer-provided insurance have less and less to lose: According to KFF’s latest survey, the average annual premium for a job-based, family health-insurance plan is now $20,756 — 54 percent higher than it was just ten years ago. And the price of such plans is rising even faster for their actual beneficiaries, as employers offload rising health-care costs onto workers: Since 2009, the average premium paid by employees for a family plan has jumped by 71 percent to $6,015.

Among workers themselves, the distribution of the growing burden is deeply regressive. Since high-wage workers have more bargaining power than low-wage ones, firms force far more cost-sharing on the latter than the former. As a result, an increasing number of low-wage workers are forgoing employer-provided coverage. As Bloomberg notes:

In firms where more than 35% of employees earn less than $25,000 a year, workers would have to contribute more than $7,000 for a family health plan … Only one-third of employees at such firms are on their employer’s health plans, compared with 63% at higher-wage firms …

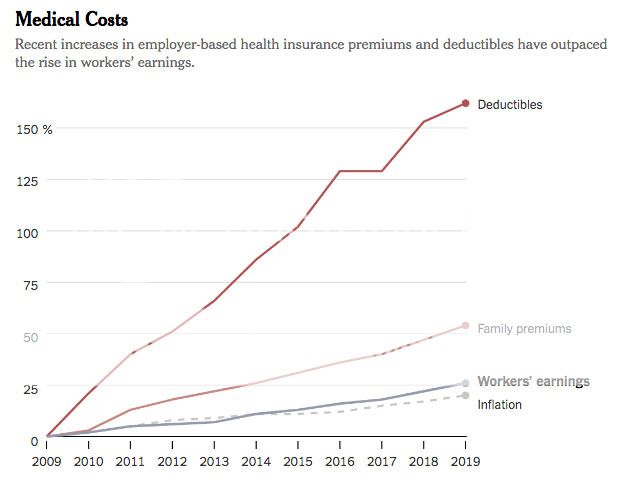

Some employers have opted to keep premiums affordable by diverting rising costs into higher deductibles, a policy that effectively takes from sick workers to give to healthy ones. Which goes over well with the median worker — right up until he or she moves from that second category to the first.

It is true that, for most of the decade documented here, American public opinion on health-care policy actually trended rightward. One could attribute that fact to the Affordable Care Act’s peculiar failures, or to thermostatic public opinion. Either way, it is an argument against the assumption that worsening objective conditions will necessarily build public support for radical reform.

Still, it’s hard not to think that there will eventually be a breaking point. Absent massive policy changes, things are going to get worse before they get better. As the boomer generation ages, it will consume more and more health-care services, thereby driving up their price. Meanwhile, the burgeoning demand for drugs that ease the burdens of senescence is leading Big Pharma to roll out exorbitantly expensive new medicines. These demographic-driven cost pressures aren’t unique to the U.S. But America’s uniquely weak cost controls make them harder to absorb. Under our existing system, the U.S. spends several times more than similar nations on health-care administration, pharmaceuticals, and physicians’ salaries. In return, Americans enjoy the 29th best health-care system in the world (just behind the Czech Republic’s), according to the Lancet.

More at:http://nymag.com/intelligencer/2019/09/kaiser-survey-premiums-america-health-care-costs-study.html

...For these reasons, a lot of health-care punditry presumes that the public’s appetite for Medicare for All — or even a Medicare buy-in — will swiftly decline once Democrats have the opportunity to actually implement it. And that scenario remains plausible. But there’s increasing reason to believe that “next time will be different” — because with each passing year, those loss-averse voters with employer-provided insurance have less and less to lose: According to KFF’s latest survey, the average annual premium for a job-based, family health-insurance plan is now $20,756 — 54 percent higher than it was just ten years ago. And the price of such plans is rising even faster for their actual beneficiaries, as employers offload rising health-care costs onto workers: Since 2009, the average premium paid by employees for a family plan has jumped by 71 percent to $6,015.

Among workers themselves, the distribution of the growing burden is deeply regressive. Since high-wage workers have more bargaining power than low-wage ones, firms force far more cost-sharing on the latter than the former. As a result, an increasing number of low-wage workers are forgoing employer-provided coverage. As Bloomberg notes:

In firms where more than 35% of employees earn less than $25,000 a year, workers would have to contribute more than $7,000 for a family health plan … Only one-third of employees at such firms are on their employer’s health plans, compared with 63% at higher-wage firms …

Some employers have opted to keep premiums affordable by diverting rising costs into higher deductibles, a policy that effectively takes from sick workers to give to healthy ones. Which goes over well with the median worker — right up until he or she moves from that second category to the first.

It is true that, for most of the decade documented here, American public opinion on health-care policy actually trended rightward. One could attribute that fact to the Affordable Care Act’s peculiar failures, or to thermostatic public opinion. Either way, it is an argument against the assumption that worsening objective conditions will necessarily build public support for radical reform.

Still, it’s hard not to think that there will eventually be a breaking point. Absent massive policy changes, things are going to get worse before they get better. As the boomer generation ages, it will consume more and more health-care services, thereby driving up their price. Meanwhile, the burgeoning demand for drugs that ease the burdens of senescence is leading Big Pharma to roll out exorbitantly expensive new medicines. These demographic-driven cost pressures aren’t unique to the U.S. But America’s uniquely weak cost controls make them harder to absorb. Under our existing system, the U.S. spends several times more than similar nations on health-care administration, pharmaceuticals, and physicians’ salaries. In return, Americans enjoy the 29th best health-care system in the world (just behind the Czech Republic’s), according to the Lancet.

More at:http://nymag.com/intelligencer/2019/09/kaiser-survey-premiums-america-health-care-costs-study.html

primary today, I would vote for: Undecided

10 replies

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

We definitely need universal coverage. But can't wait for Warren to tell folks their taxes are

Hoyt

Sep 2019

#1

First, malpractice insurance is not that expensive. Second, a doc can serve in a rural area for a

Hoyt

Sep 2019

#5

With some prescription drugs that may be true, if it is, I wouldn't be the least bit surprised

Uncle Joe

Sep 2019

#9

Any serious talk about any UHC plan has to tackle price controls and cutting costs...

Humanist_Activist

Sep 2019

#4