I’ve been reading up on it today. The problem isn’t the fees which amounted to a few million dollars. This is what I’ve gleaned.

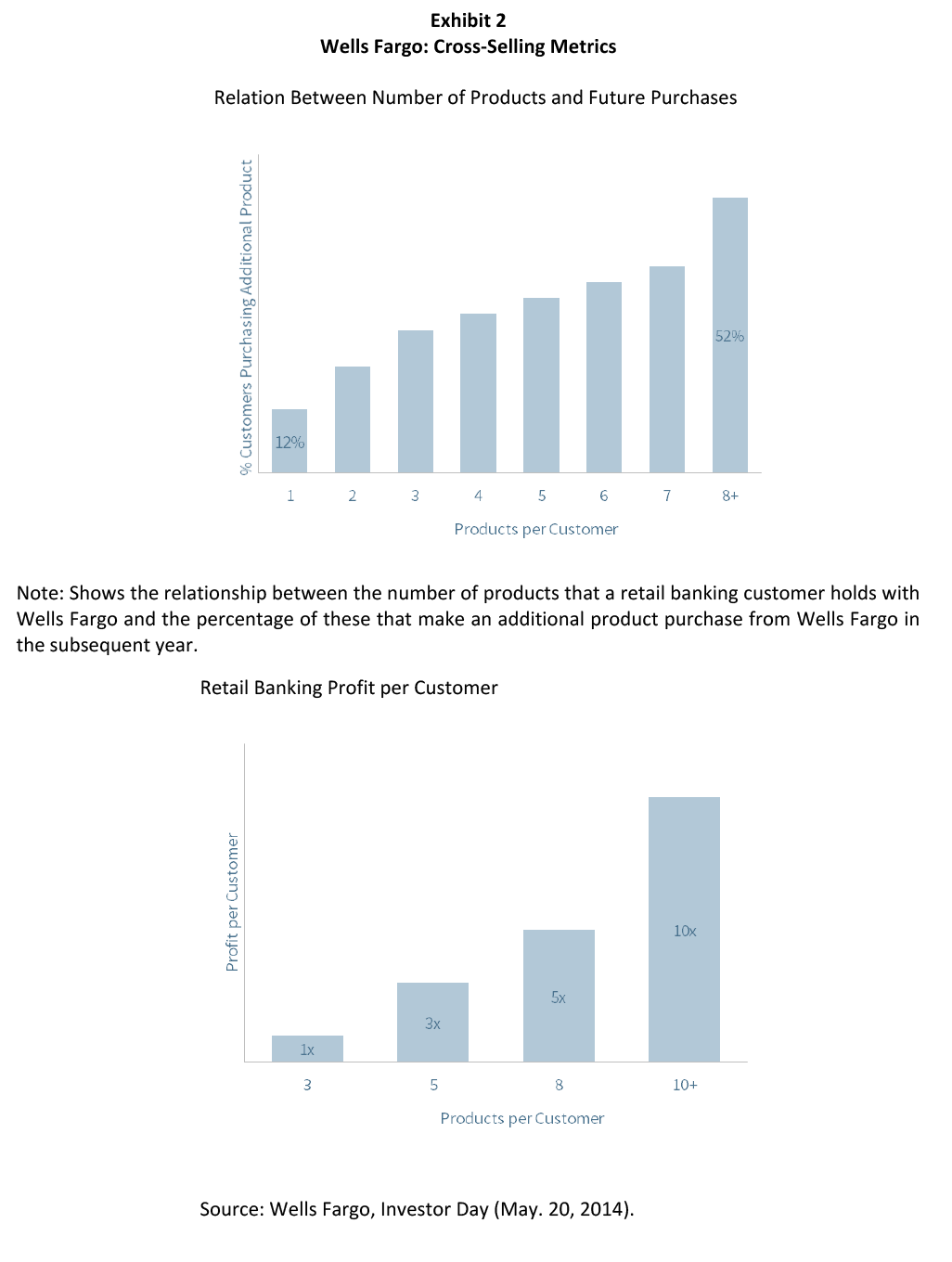

Apparently some accounting geniuses figured out that people with multiple accounts were more likely to do more business with the bank and generated more bank profit. See exhibit 2

]

]

So in a classic case of mistaking cause and effect they decided to incentivize that. (My opinion)

Based on the operating principle just mentioned, the Bank (and the other financial services operations that were held by WFC) was infused with a sales culture that vigorously promoted the cross-selling of services. Opening of new customer accounts was rigorously tracked by Wells Fargo’s operating systems; success was rewarded with bonuses; lack of success with “enhanced training” or termination.

At the same time as they demanded results they pushed authority down the management chain

The Bank’s decentralized structure gave the head of the Community Bank near unlimited discretion in establishing sales goals, and management at all levels were remorseless and relentless in pursuit of these goals

(duke)

https://sites.duke.edu/thefinregblog/2017/04/26/phony-accounts-scandal-a-case-study-for-bank-board-directors/]

Warning signs appeared but ignored. Then there was there was a story by the LA Times in 2013

To meet quotas, employees have opened unneeded accounts for customers, ordered credit cards without customers’ permission and forged client signatures on paperwork. Some employees begged family members to open ghost accounts.

https://www.google.com/amp/s/www.latimes.com/business/la-fi-wells-fargo-sale-pressure-20131222-story.html%3f_amp=true]

Then in 2015 they were sued

In May of 2015, the Los Angeles City Attorney filed a lawsuit against Wells Fargo based on the Bank’s alleged fraudulent and abusive sales practices.

(duke link)

(Snip)

But somehow the scope of the problem was never presented to the board.

An early draft of the presentation – which was never delivered to the Committee – disclosed that approximately 1% of employees in the Community Bank had been terminated for sales integrity violations in 2013 and 2014. After the Community Bank’s management questioned the validity of this number, it was removed from the final presentation that was delivered to the Risk Committee. Instead, during the May 2015 Risk Committee meeting, the head of the Community Bank informed the committee that in 2013 and 2014 combined, 230 employees had been terminated for sales abuses

(duke link)

Senior management wanted great sales figures. They set up a system where they demanded unobtainable results and didn’t care how that was achieved.

One might ask why that is so bad. 2008 wasn’t that long ago. Liar loans were a big part of that. Also triggered by unrealistic sales targets and free wheeling subordinates. The fact that in 2015 the board still didn’t demand and get an honest accounting says to me they didn’t want to know.

One might blow this off as a stupid scandal, but it wasn’t for the perpetrators. They all had millions in stock options and the fraudulent growth of retail banking drove up stock prices which made them filthier rich.

The perpetrators also got raises, promotions and more stock options on the back of those fraudulent accounts.

I posted a reply below. Even after clawbacks and fines the two people in the article made out fine.

Sorry for the ramble. Reading was interesting.

= new reply since forum marked as read

= new reply since forum marked as read